Between rising healthcare costs, tariff-related price increases on various goods, and a housing market that drains most of the paycheck, we are reaching an affordability crisis in America.

The car market isn’t offering any relief with average transaction prices for new cars approaching $50,000. The solution for some buyers is to stretch a loan as long as possible, upwards to 100 months, to get payments in line with their budget. Here is why that can be a risky move.

There is still a lot of economic uncertainty, and for folks shopping for a new or used car, some tough decisions may have to be made regarding what they can actually afford. Many buyers will fall into the monthly payment trap and stretch a loan out for as long as possible so that their car note is reasonable. Some people may be tempted by a 100-month car loan, but they may not fully understand the math as to why an over-eight-year loan is financially dangerous, or what their alternatives should be.

Cheap Payments Now With Big Costs Later

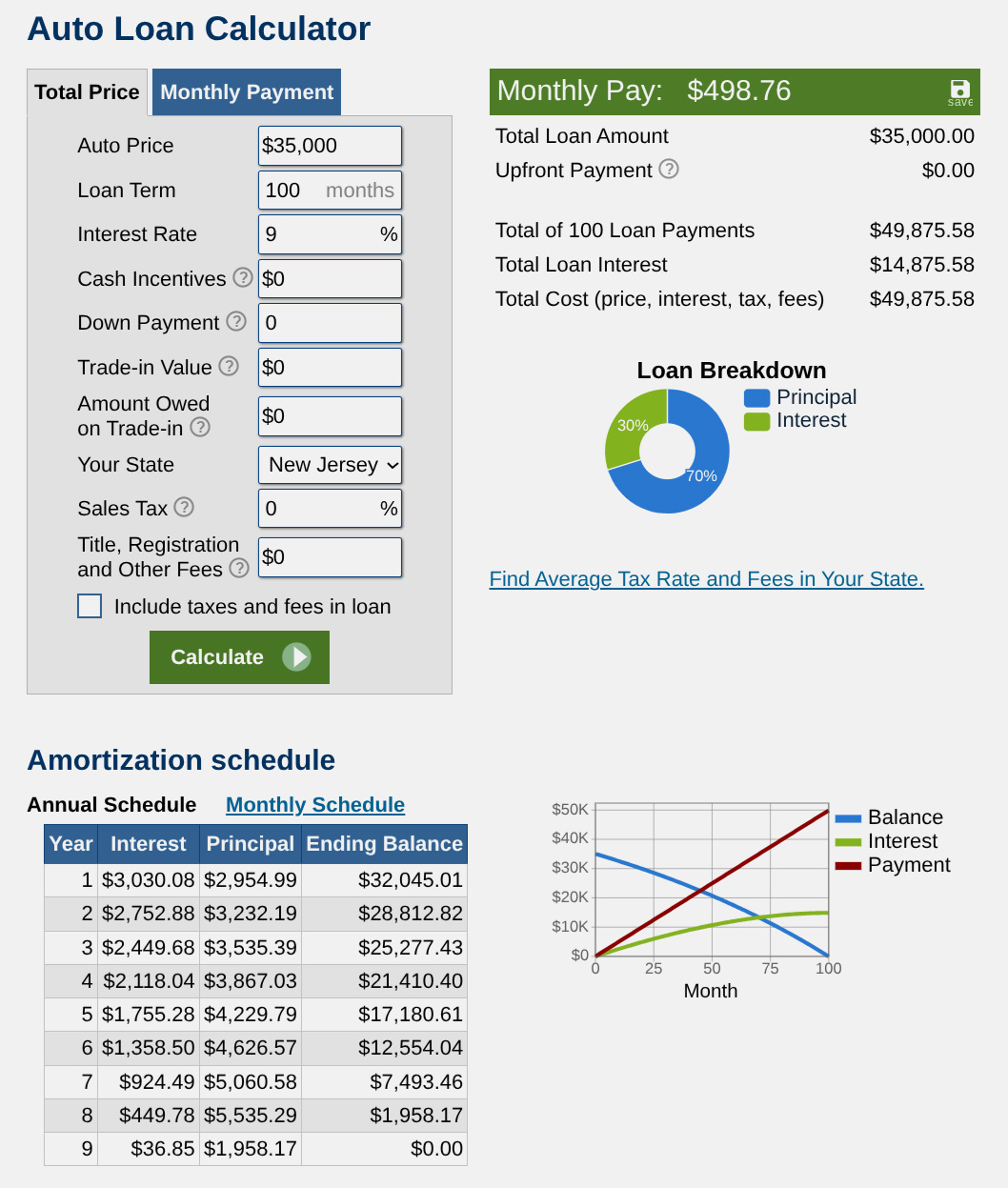

Let’s examine a hypothetical purchase of what most would consider a “reasonable” and high-quality car, the 2026 Honda CR-V Hybrid, with the goal of getting a payment under $500 per month. The base price of a Sport trim with AWD is $38,580. Perhaps with some good negotiation, you can wiggle that price down to an even $35,000.

Currently, Honda is running an APR special of 4.99% for 60 months. With no down payment, that works out to about $660 per month. That is pretty steep, now suppose we stretch that loan to 72 months. Naturally, the interest rate will be higher. Assuming a 7.0% APR for the six-year loan, the payments are $596 per month, a bit better but still not quite affordable. The dealer manages to find a bank willing to underwrite a 100-month loan at 9% APR with payments of $498.76 per month.

You got your very reasonable car under budget, but at what cost? Here is the breakdown:

At the conclusion of the loan, you will have paid almost $15,000 in interest on a $35,000 purchase, and about $8,200 of that interest will be paid in the first three years. If we compare that to the 60-month loan at 4.99% APR, that’s only about $4,600 in interest.

Not only does the 100-month loan cost over three times the interest compared to the five-year loan, it also puts the buyer in a potentially underwater situation if they decide to trade that CR-V after a few years. In fairness, a Honda should hold value pretty well, compared to some other brands, but the likelihood of having any equity if you decide to get rid of it after the first few years is low. There is also the chance that the person would have to roll over negative equity into the next loan.

What Could You Do Instead?

If you are trying to achieve a specific monthly payment, there are two solutions. The obvious solution, though not one that most buyers want to admit to, is to simply get a cheaper car. There is no shame in concluding that a brand-new ride is not the best move for your finances. In fact, a less expensive used car is often the smartest play.

If you were targeting a payment of $500 per month on a 60-month loan, assuming a 7.0% APR, your total spending limit comes to about $25,000 with tax and fees. Even though a new CR-V Hybrid is not in the cards, that doesn’t mean you can’t get a quality car. But you may need to be flexible when it comes to models, color, and equipment.

For example, here is a quick selection of 2020+ hybrid crossovers within 200 miles of the LA metro with under 50,000 miles. Granted, none of these are CR-Vs, but almost all of them will give you a practical car that will have respectable gas mileage for much less than a new Honda:

Alternatively, Leasing Can Get You The Same Car For A Similar Price

If a buyer insists on getting a brand new car, but needs to stay within that $500 per month threshold and doesn’t want to roll the dice on a 100-month loan, a potential solution is to lease. Honda’s current offer on a CR-V Sport Hybrid lease is $299 per month with $4,899 due at signing before tax and fees for a 10,000-mile/36-month program.

If we were to restructure that into a zero-down lease, it works out to around $436 per month before tax and fees. And most folks would likely fall under the $500 per month target even after those additional charges are added in.

The classic argument against leasing is that you don’t have any equity in a vehicle, as you are essentially “renting” it from the finance company, and you are always stuck in the cycle of payments. In that respect, if you look at a lease compared to a 100-month loan, we have already established that having equity after a few years is not likely. Also, instead of paying on a car where your loan far outlasts the warranty, you could have cycled through three leases in the same time with payments well under your target and maintain full warranty coverage. Most “finance experts” will say that leases aren’t a smart money move, but they are far less risky than taking out a loan for 100 months.

One of the common bits of car-buying advice is to never tell the salesperson how much you want your payment to be. Now with 100-month car loans available, this is just one more tool for unscrupulous dealers to convince buyers that some cars are more “affordable” than they really are.

Your best defense against a bad deal is to understand how the math works ahead of time and not get roped into paying way more interest than you should while being trapped in a car loan for over eight years.

Top graphic images: Honda; DepositPhotos.com

Great article, like all of Tom’s writing. Hope to see more from you here!

I would never want to be making payments on a car (though I can understand that other people have different priorities)

My current car “payment” is probably averaging about $50/mo for parts…

Twelve years ago, I was driving a 15 year old minivan, and its transmission broke, requiring a $2,200 replacement. I was telling this to a work acquaintance, who said, “You should just buy a brand new one. At 0% interest, they are practically giving them away.” This person has a PhD, but I think that my one-time large maintenance bill more than makes up for car payments. Note: Their PhD is NOT in finance.

I don’t want to hear if you can’t afford to pay cash, you can’t afford it. That’s a bit obnoxious, each person has different things going on.

With that said, yea please don’t do a 100 month loan, if you need to do a 100 month loan to afford it, that monthly payment will get old real quick and now you are most likely heavily upside down and haven’t paid off much of the principal, most of the payments in the beginning is going to interest.

Leasing is ok to get a lower payment, if you go into it knowing what you are doing. If you drive under 10k miles a year, you’ll be ok. You need to find an undesirable car where the manufacture is putting in cash incentives to move the car. And after all that, the manufacture is giving $10k incentives to buy the car at the end of the lease. That last part is not very common at all, but that’s what Nissan is doing with the Ariya and we end up with a very cheap car.

if you can’t afford to pay cash, you can’t afford it

if you can’t afford to pay cash, you can’t afford it

if you can’t afford to pay cash, you can’t afford it

if you can’t afford to pay cash, you can’t afford it

if you can’t afford to pay cash, you can’t afford it

if you can’t afford to pay cash, you can’t afford it

if you can’t afford to pay cash, you can’t afford it

if you can’t afford to pay cash, you can’t afford it

:-p

Shakes fist

Or just lease a Tacoma. Leasehackr constantly has deals being promoted in there; since they seemingly depreciate at the same rate as diamonds, you can get a very inexpensive lease based on the high residual value.

I don’t want one, but if I needed a new something, I’d certainly consider it. I’ll just stick to raggedy, used up Volvos, thank you.

Before manufacturers changed it, you were allowed to do 3rd party buy out too. I leased the gx460, fit, s2k, my trade in or private party value was more than the residual. I’d just sell the car, and pocket the extra. Worked out pretty well for a while.

100-month car loans. 50-year mortgages. The current advice on social security is not to draw upon it until 70. Did I miss something? Is everyone living to 125 these days?

No but who knows, debt soon may be inheritable.

It is already in some parts of the world.

The debt-inheritable loan products will be marketed as a way to “extend one’s legacy”.

And the government will be on board since it will encourage people to have more kids to prop up the inflationary economics they so love.

Of course. Plus, someone has to step in and make sure these things can’t be discharged in bankruptcy. Won’t someone think of the banks?

Better kids than shareholders amIrite?

In a way they are. It’s part of the estate, no?

I think that depends. If the mortgage is in an LLC for example the other assets of the estate may be untouchable. But I’m not a lawyer so it’d better someone else who knows more about such matters to weigh in.

Yes part of the estate, but if the value of the estate is less than the value of the debt, then the inheritance is zero and the banks get the shaft.

I wonder if banks would start lowering the limits of unsecured credit (e.g. credit cards) when people go beyond a certain age, just to limit their exposure.

A 50 year mortgage is at least on a moderately appreciating asset with tax deductible interest.

Do you want another housing crisis? Because this kind of reasoning is how 2008 happened. 😛

Yes, the correct alternative to a 100 month car loan is anything else. Literally any other option is better. Buy something cheaper. Steal a car. Stage a slip and fall at the dealership and tell them you’ll take a car instead of suing them. It’s hard to find a worse option than a 100 month loan.

I did a real life “LOL” when I read “stage a slip and fall at the dealership”

Thank you for the much-needed giggle amidst my hour long staff meeting this morning!

Happy to help. I’m glad that my current job rarely has meetings because we have too much chaos that can’t be left alone long enough for regular meetings.

I really wish we had fewer of them. Despite our chaos, the powers that be seem just as committed as ever to scheduling these (often) pointless meetings.

Oh nice Tom writes here now! I’ve used Tom’s car broker service twice and he got us exactly what we wanted both times. Welcome to Autopian Tom!

I am a regular reader and contriburtor on the personalfinance subreddit. There is a fairly predictable flow of people who either want to “Get out” of their underwater car loan, or their underwater vehicle has been totaled and they don’t have gap insurance. Those problems are only going to increase if people buy 100 months loans. That’s crazy. Many people never learned about the dark side of car loans and they’re easily pulled into these traps.

I too used to frequent that sub. Many people never learned about the dark side of interest is a more apt description.

Well, a loan is simply a rental of money. (Same as a mortgage that way.) So, you are either renting a car or renting the money via interest.

And paying it in full leaves one losing the opportunities to invest that money (or keeping a rainy-day fund), though it would be difficult to match a return to the interest rate on the car.

So, the first question should be: do I NEED a new car?

If so, do I NEED THIS car?

Etc.

I borrowed money from my mom at 0% interest for a used car, paid her back when she asked for a payment. That’s the best deal (IMO — she did not break my kneecaps once!).

Also, leasing is a good deal IF the math works out. I mean, suppose that CRV payment were $100 instead of $299 or $436? There is likely an indifference amount wherein one would choose either own or lease indifferently, so sayeth the math.

People who don’t do the math will learn the hard way about math.

“People who don’t do the math will learn the hard way about math.”

Not all people. Some people just spend and spend and then wonder why they’re “broke” even though “they make lots of money”

Long loans make sense only with cheap financing. Like 1% or 0%. And planning on keeping the car for a long time.

Don’t tell me what to do dad. /s

But cereally the prices I paid for any of the used cars I have owned I just find it hard to want to get a new car. All my recent (non-classic car) purchases so daily drivers are always within 5 or so years old and the price you can get a car in that range vs new is pretty ridiculous especially if you get a CPO.

Instructions unclear, are you telling me I should be buying Jeep Grand Royale with Cheese with 96month financing?

No, 100 month financing! Read the article! 🙂

Find one without Cheese and that’ll knock at least a month off the loan.

Instructions unclear, ended up with a Double Quarter Pounder from the Value Menu.

Still better than a jeep

Must be a French model.

As always, great advice Tom.

This is before you factor in the depreciation hit, biggest in the first couple of years, on that new car.

OMG! Haven’t had a car payment since 1987.

Recommending a used Jeep with a hybrid powertrain should not be in the same article saying 100 month term is a poor financial choice.

TBF – Stellantis is most famous for their 96month financing.

Why stop with just one bad life choice?

The Jeep would be a poor financial decision. That ’24 Hornet right below it is the smart move.

That Hornet seems a bit overpriced. There is a new hybrid Hornet R/T within 100 miles of me that is listed at $26,992.

I wasn’t recommending any of those specific cars, just providing a quick market sample of various used cars that would be possible at that price point.

This makes me wish for the heady days of zero-percent financing…

Until my last two or three cars, I bought cheap but interesting vehicles, and often sold them for more than I paid. My friends would give me a hard time about getting, something newer, but I would say “one year of your payments buys me this car and a lot of gas.”

I know the Joneses. Nice folks. But I don’t feel the need to keep up with them.

“I know the Joneses. Nice folks. But I don’t feel the need to keep up with them.”

Nice, I am using this and I will absolutely give you credit!

Use it with my blessing!

An 8 year 4 month auto loan. So much can happen in that amount of time. You could fall ill. You could lose your job. You might move somewhere that you don’t even need a car.

But, some people have no concept of anything beyond the short term so there will be plenty of people who fall for this.

In the five years since my wife and I bought our van, we’ve moved out of state, sold a house, sold our other car (2020 car prices were amazing for sellers), lived in three different places, and bought a new house after moving to a different area again. We’ve since bought another car in cash and I recently started a new job that gives me a car to be used for both work and personal use.

The only reason we’re still dragging that van along through all those life changes is that it’s literally irreplaceable (the specific model isn’t made anymore) and it’s a fun camper van that isn’t really applicable as a daily driver.

Then again, I’m not really one of those people who still expects to be living the same life for five years running. Different strokes, I guess.

I think a camper van that isn’t your daily is different. As you mentioned, it’s not made anymore. That’s special, whether you’ve paid it off yet or not.

That’s an entirely different scenario than a 100 month loan on a friggin CR-V. Imagine making the payments for 80 months and then something bad happens and it gets repossessed.

A vivid, plain language description of the situation and its real world dangers, understandable by anyone willing to take the time…which was exactly what I expected. Tom’s pieces were the last reason I stuck it out at the old site for as long as I did.

I hope to be here a bit more often now.

Finance companies grinning at someone paying twice the MSRP to finance a vehicle for 100 months, only for it to be worth half that MSRP by the time the loan is paid off.

With Tom’s arrival, the circle is complete. The Autopian global domination is now assured.

Ok. Now do this for trucks so haters can see that we are paying way more than cars

Sorry, your username requires you to phrase that in the form of an angry rant.

We will also accept a tirade.

Add “shaking a fist” for maximum effect.

Done!

Ok.

Dag nabbitt! I don’ wanna hear no bellyachin’ about yer tinny commieyooter curs! Y’all see them prices on dem dere trucks!?! Outright criminal I tell ya! Gonna write my congressman once I save up fer the stamp!

I don’t think my brain could even comprehend “100-month loan” in the title. I saw $100 / month instead. 100 months is just too insane to be a real option…

I DO WHAT I WANT!!!

Also, hey Tom! Glad you’re here!

until they run out of people willing to sign on the line for crazy loans for expensive vehicles we’ll never see any downward price pressure.

convincing people that they don’t ‘deserve’ a new car won’t work. consumers would rather be poor than look poor.

BHPH lots show they will not run out of people. You will never fix stupid. I worked in a shop and my colleague would always say “Never underestimate the power of an idiot.”

Hell yes! Love seeing Tom at the Autopian!