Between rising healthcare costs, tariff-related price increases on various goods, and a housing market that drains most of the paycheck, we are reaching an affordability crisis in America.

The car market isn’t offering any relief with average transaction prices for new cars approaching $50,000. The solution for some buyers is to stretch a loan as long as possible, upwards to 100 months, to get payments in line with their budget. Here is why that can be a risky move.

There is still a lot of economic uncertainty, and for folks shopping for a new or used car, some tough decisions may have to be made regarding what they can actually afford. Many buyers will fall into the monthly payment trap and stretch a loan out for as long as possible so that their car note is reasonable. Some people may be tempted by a 100-month car loan, but they may not fully understand the math as to why an over-eight-year loan is financially dangerous, or what their alternatives should be.

Cheap Payments Now With Big Costs Later

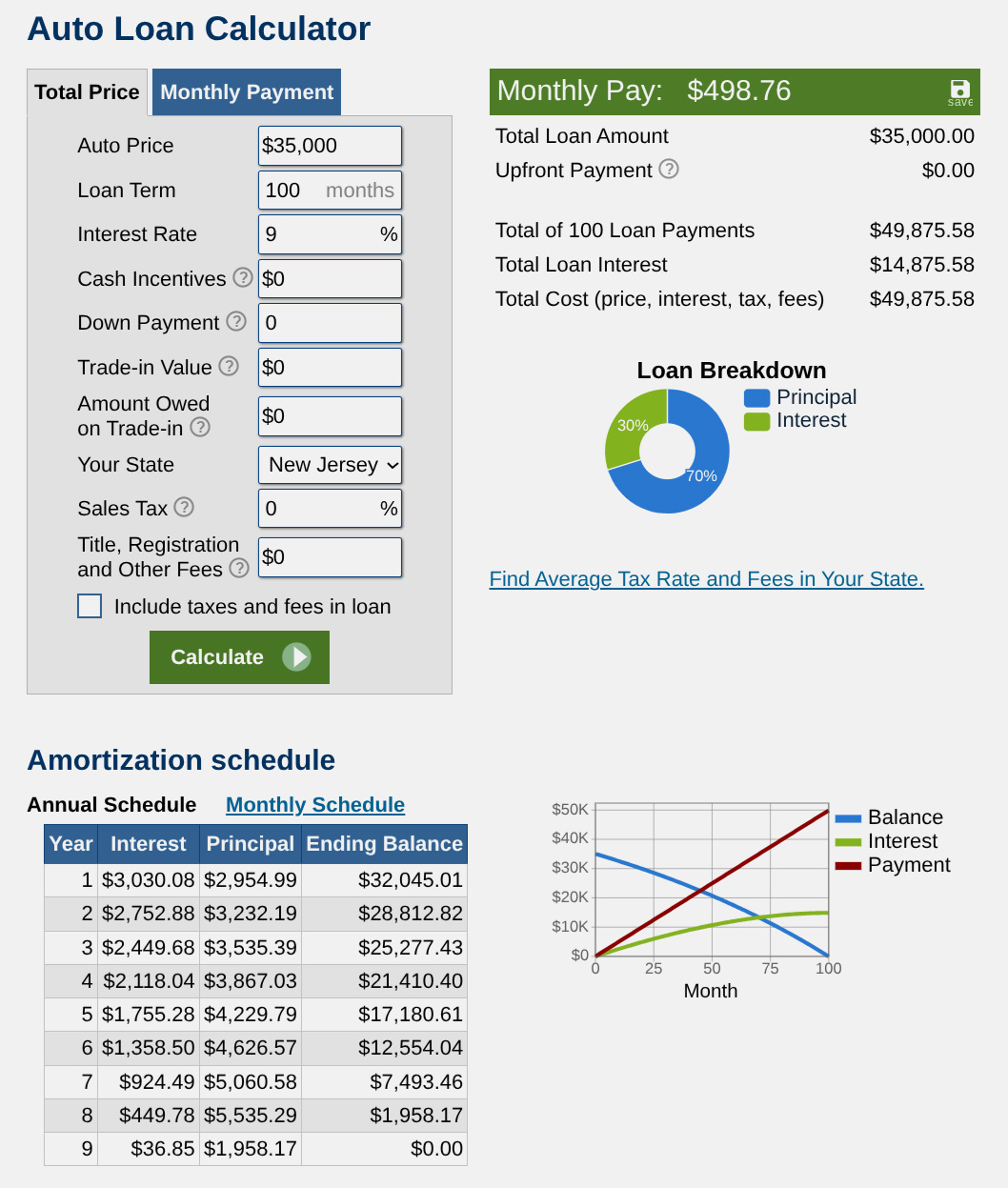

Let’s examine a hypothetical purchase of what most would consider a “reasonable” and high-quality car, the 2026 Honda CR-V Hybrid, with the goal of getting a payment under $500 per month. The base price of a Sport trim with AWD is $38,580. Perhaps with some good negotiation, you can wiggle that price down to an even $35,000.

Currently, Honda is running an APR special of 4.99% for 60 months. With no down payment, that works out to about $660 per month. That is pretty steep, now suppose we stretch that loan to 72 months. Naturally, the interest rate will be higher. Assuming a 7.0% APR for the six-year loan, the payments are $596 per month, a bit better but still not quite affordable. The dealer manages to find a bank willing to underwrite a 100-month loan at 9% APR with payments of $498.76 per month.

You got your very reasonable car under budget, but at what cost? Here is the breakdown:

At the conclusion of the loan, you will have paid almost $15,000 in interest on a $35,000 purchase, and about $8,200 of that interest will be paid in the first three years. If we compare that to the 60-month loan at 4.99% APR, that’s only about $4,600 in interest.

Not only does the 100-month loan cost over three times the interest compared to the five-year loan, it also puts the buyer in a potentially underwater situation if they decide to trade that CR-V after a few years. In fairness, a Honda should hold value pretty well, compared to some other brands, but the likelihood of having any equity if you decide to get rid of it after the first few years is low. There is also the chance that the person would have to roll over negative equity into the next loan.

What Could You Do Instead?

If you are trying to achieve a specific monthly payment, there are two solutions. The obvious solution, though not one that most buyers want to admit to, is to simply get a cheaper car. There is no shame in concluding that a brand-new ride is not the best move for your finances. In fact, a less expensive used car is often the smartest play.

If you were targeting a payment of $500 per month on a 60-month loan, assuming a 7.0% APR, your total spending limit comes to about $25,000 with tax and fees. Even though a new CR-V Hybrid is not in the cards, that doesn’t mean you can’t get a quality car. But you may need to be flexible when it comes to models, color, and equipment.

For example, here is a quick selection of 2020+ hybrid crossovers within 200 miles of the LA metro with under 50,000 miles. Granted, none of these are CR-Vs, but almost all of them will give you a practical car that will have respectable gas mileage for much less than a new Honda:

Alternatively, Leasing Can Get You The Same Car For A Similar Price

If a buyer insists on getting a brand new car, but needs to stay within that $500 per month threshold and doesn’t want to roll the dice on a 100-month loan, a potential solution is to lease. Honda’s current offer on a CR-V Sport Hybrid lease is $299 per month with $4,899 due at signing before tax and fees for a 10,000-mile/36-month program.

If we were to restructure that into a zero-down lease, it works out to around $436 per month before tax and fees. And most folks would likely fall under the $500 per month target even after those additional charges are added in.

The classic argument against leasing is that you don’t have any equity in a vehicle, as you are essentially “renting” it from the finance company, and you are always stuck in the cycle of payments. In that respect, if you look at a lease compared to a 100-month loan, we have already established that having equity after a few years is not likely. Also, instead of paying on a car where your loan far outlasts the warranty, you could have cycled through three leases in the same time with payments well under your target and maintain full warranty coverage. Most “finance experts” will say that leases aren’t a smart money move, but they are far less risky than taking out a loan for 100 months.

One of the common bits of car-buying advice is to never tell the salesperson how much you want your payment to be. Now with 100-month car loans available, this is just one more tool for unscrupulous dealers to convince buyers that some cars are more “affordable” than they really are.

Your best defense against a bad deal is to understand how the math works ahead of time and not get roped into paying way more interest than you should while being trapped in a car loan for over eight years.

Top graphic images: Honda; DepositPhotos.com

That CPO Kia Sportage looks like a decent deal.

Every single one of those loans is a brick pulled from the Jenga tower that is the US economy.

If they’re offering a really good interest rate, the longer the loan the better.

If you take that cash and invest it in anything that yields a higher APR (net of capital gains tax = 15% in the US), you’re winning.

I think you can get a 10-year CD at up to 4% APY these days. So any spread between the car loan rate and 3.4%, is all profit in your pocket.

No one is offering 1.9 APR on a 100 month loan….this term is a tool for desperate buyers and dealerships to get people into cars they really can’t afford

Why is it so hard to find used cars from private sellers nowadays? Our beater is collapsing and so I am looking to spend $5-7K for something my wife can take to work. It has to be a hatchback (maybe a small station wagon), she hates driving anything larger than a Civic. She wants a Fiat 500 – any real reason not to get one, aside from the Fix It Again, Tony stereotypes?

I don’t want a bunch of random people checking out my stuff anymore! Last used car we sold for a family member, we met at the Auto Club lot so that we could do the paperwork right there. Too many ways to get scammed now.

While I agree, the hassle ought to be worth the extra few thousand. The owner of the car I am looking to buy for $6K probably got $2,500; if I pay them $4K we’re both ahead.

I was going to add that the car you want to sell privately needs to be cheap. The dollar amount depends on the person. Sometimes you just want the extra car out of your driveway and off your insurance. We traded in our last car mainly for convenience as their offer was not worth the difference plus our time and effort and inconvenience.

We have friends who have four kids. They use Carmax a lot to sell cars just to keep things simple.

Seriously? Carmax, Carvana, and the general shittyness of online private sales.

Yeah, you could probably get a slightly better price selling private, but why bother with time-wasters and potential scammers when it’s easier to sell to either of the above?

In my area Facebook Marketplace has a lock on the private used car market. The interface is garbage but I sold my campervan in 4 days.

Same – except 90% of the sellers are dealers who are selling the cars that are not good enough to get a warranty.

That is not my experience. At least not shopping for older cars. Around here those are mostly private sellers (at least from the pictures taken in a driveway or street parked)

For cars that are 2-5 years old – yes those are dealers because the 2/3’rds of new car buyers that keep their vehicle for 5 years or less are trading that car to a dealer or leasing.

Very few people are going to go through the hassle to sell a 5 year old car private party and then go buy a new car from a dealer.

Yeah, here they do not always disclose for lower cost cars. I went to test drive something and an old lady across the street took me aside and told me the dude owned a small buy here/pay here lot – which checked out. Half of them give themselves away by asking which car you’re calling about, or having tags on the keys that describe the car.

Selling on FB has worked pretty well for me, though, the two times I tried.

Fools and money. If $150/mo strains your money, you should just be shopping for a much cheaper car to start with.

One of the problems is that people are trying to look like they have more than they actually do. They want to be seen as wealthy as they cruise by in their $86,000 luxmobile. They don’t need it, they just want it. And that’s the problem. Our current system tells people they can afford something they can’t and the system is set up for them to have to pay for it, even if they go bankrupt. High interest rates used to keep people from buying something they couldn’t afford, but the banks and manufacturers have colluded to create ridiculously long loan terms and our government just takes the money being given to them by these corporations to look the other way.

A $23,000 four passenger sedan fits almost everyone’s life. You don’t need a Yukon Denali to take your two kids to school, but hey, mom’s gotta look good, right. And dad needs his F350 to take his toolbelt to the job site.

The $63,000 difference on a car purchase can be banked and used to buy your next car for cash rather than stay in debt for life.

Underappreciated, this comment is.

If you have two kids or fewer, then you can get by with any cute-ute (CX-5, used CRV, used Rav4, etc.).

You don’t need a Jeep because you get 4 snowstorms a year, and you don’t need an F-150 because you go camping 4 times a year.

There is something to be said for luxury and ego, but it needs to be recognized that that is what they are. And anything above a 10k Yaris or Honda Fit is fueling ego and luxury.

I wish the author would dig into the data a bit more. What are the credit scores of new car purchasers? The answer: 1 in 6 used car purchasers is “subprime.”

https://www.kbb.com/car-news/study-84-of-new-car-borrowers-have-prime-or-better-credit/

So fully 15-20% of new car purchasers should be buying used. 15-20% of those loans will be delinquent within 4 years (see Figure 5):

https://www.federalreserve.gov/econres/notes/feds-notes/a-note-on-recent-dynamics-of-consumer-delinquency-rates-20251124.html

I am not really going to weep much for rich people taking out long-term loans; it’s their money to do with as they wish. Nor am I going to weep much for people with credit scores in the 500s trying to buy new – they should be buying used.

We have a consumption crisis, but frankly, as the author indicates, most people can simply buy used (which is what they’re doing, for the most part). This is a problem that gets discussed at a high level (“New car payments are really high”) without really mentioning the underlying assumption – that people are somehow entitled to affordable new cars.

Took delivery of a 2004 Colorado Crew cab Z71 in may of 2004. Sticker was $26,995. after trading in a truck and a down payment, i financed around 17k. had i financed for 48 months GMAC would have given me 0% financing but i was in college working at office depot so i opted 60mos and the APR was .8%. $311 a month and that was after an extended warranty. paying more than $400 a month makes me sick to my stomach. i usually keep vehicles for 10+ years so the length of the loan doesnt really bother me much as long as the out the door price is where i want it. looking back and comparing that to prices and APR’s today is staggering.

Absolutely not. At the same time, the used car market I depend on to feed me reasonable vehicles requires a certain amount of people to eat shit on their loans. So I’m torn.

I have dealt with a family-owned Chevrolet dealership for many years. They know I am financially secure. However, when buying a car, the first question the salesperson asks is “What do you want your monthly payment to be?” I always have to respond that I already know what the monthly payment will be, the duration of the loan, the interest rate I will be paying, and how much I will be putting down based on the out the door figure offered to me. They want to check my credit rating and become confused when they discover I have it locked.

I know I am an outlier, but I find it disturbing that most car purchasers base their purchase on monthly payment alone, which opens them up to longer loan durations, higher interest rates, worthless add-ons, and a complete acquiescence to any negotiating power.

And yes, I bought a Chevy model that is identical to the Cadillac model – for thousands less. I’m not out to impress anyone with a fucking badge on the grille.

I tell them the payment will be what the payment will be, what I’m concerned with this the out the door price, tax, license, document fees ect. I also go in knowing what interest rate I can get from both of my credit unions, and tell them that if they want my finance business they will have to beat that rate by a decent bit. Which is why I’ve got accounts at two credit unions and why I “spent” $5 more on my car than my out the door offer as it went into the savings account at the new to me credit union.

Going into a car dealership without a pre-approval is like going into shark-infested waters covered in bleeding sores. Don’t do it, ever.

Though that said, I have on a couple of occasions taken their exorbitant financing because it was tied to rebates or other pricing advantages. And then I literally went down the street and refinanced with my credit union before the ink was dry. Pre-payment penalties are illegal in both of my states, thankfully. I did pay three payments on a slightly higher dealer note so that my favorite BMW sales gal could get her spiff though. I really like her, and it was like $30 difference for that short of a time. Brought her a couple bottles of wine back from Italy the last Euro Delivery too. I got $12K+ off US msrp on that M235i so no big deal.

One time I went into the dealer, knowing of course the interest rate I could get through my credit union and my high credit worthiness. When I came back from the test drive they were waiting with some numbers. The interest rate was really high. I said as such and he came back with “Well that is what we find is the typical rate for someone with your credit score” I said BS, I guess I won’t be doing business with you and walked out the door.

Exactly the right move when dealing with idiots.

“I will make two payments: The deposit, and then the balance.”

Depends on the interest rate. If I can make more investing the money than making payments, I will make the payments. I don’t have $50K laying around collecting dust, and taking the money out of investments means not only losing the future gains, but recognizing current gains AND paying income tax on them at a pretty stiff marginal rate. Nope, I will pay a little interest and make it up in the long run.

But as I have said here before, at this point the automakers have done me the great favor of removing ALL temptation of buying any new more new cars. And I don’t see that changing. Even minty-fresh examples of the cars I like are basically couch cushion money at this point compared to what the new equivalents cost. The last car I bought for myself, my ’14 E350 wagon three years ago, was about 25% of the cost of a new one, and I like it far better than the ridiculous nonsense Mercedes was peddling new, then or now. But if I had been buying in ’14, I may well have bought a new one. I did buy a new BMW in ’15, my last new one of those. My last actually new car was in ’17 for a GTI Sport, then I bought my technically not new but might as well have been 28 miles on it Fiata in ’19.

Exactly. The amount I put down and the loan I assume is a function of opportunity costs (the amount of money I put down vs. investing it), and my personal cash flow. It’s all worked out before I step into the dealership.

I will also point out that consumer protections are something that the current administration is successfully reducing. Sign any loan with a careful read-through and hope that they aren’t changing the terms between what they show you and what they put your signature on.

I read EVERYTHING before I sign it. Usually the longest part of the process, though I am a very fast reader.

You are not an outlier, you are just smart. Which, yeah, OK, makes you an outlier.

Whenever a salesperson asks me about payments, I tell them I can buy the car with one payment or as many as the thing has months of warranty, and the interest rate will determine which. Then I invite them to beat my pre-approval, and no, I am not telling you what the rate is other than it is very commensurate with my (extremely high) credit rating. About 50% of the time they do indeed manage to beat my bank/CU – but I am going to make them work for that kickback. Any nonsense about the price changing if I don’t finance it with them would lead to them seeing my back walking out their door. I am actually very friendly and a hopefully a fun guy to sell a car to – but I also don’t put up with any bullshit. I have never once in my life needed to buy a new car, I just wanted to. Big difference.

I start the finance dude discussion with a blanket NO to any and all add-ons, and expressing my willingness to walk right out the door if they don’t get on with it. Saves all sorts of time and bullshit. I don’t think I have ever spent more than 10 minutes signing the papers.

I agree with you that a 100mo loan is a bad idea and the alternatives you’ve offered are better IMO, BUT that’s just our opinion.

I’m generally not one to embrace the “agree to disagree” philosophy (I believe we can and should hash it out, usually.), but in this situation I think making more allowances than I usually would is warranted.

The statements

and

come off like the buyer in the hypothetical is being unreasonable in wanting a new CR-V despite an obviously tough cash flow position. I don’t think that’s fair.

The hypothetical situation has problems that we deem unacceptable, but the alternatives come with their own set of problems. The hypothetical consumer has selected the problem package they’re willing to live with from a set of possible problem packages, and even though it’s not the package we would choose, ¯\_(ツ)_/¯ I can’t really tell them they’re wrong.

I read these statements understanding that Tom’s full time job is a business helping people to find and buy cars, assisting in all aspects of the buying process. (Read his bio)

So, if Tom makes a statement about what most buyers want, or think they want, or their rationality (or lack thereof), and how well they understand the implications, I’ll take him at his word. I’m sure he’s helped hundreds (thousands?) of different buyers of different cars at different price points.

True, but think about it this way: are Tom’s customers a representative sample of the overall car buying population?

I’m leaning towards “no”

People buying more car than they can actually afford, and therefore the rate of repos and defaults are well established, and uneducated financial decisions are not a surprise.

Here’s a starting point about the trend in buyers, but there are statistics and government data all over the place.

https://www.usatoday.com/story/money/2025/09/10/auto-loan-delinquencies-debt-report/85998815007/

Expert in the field talks about that field and says yes.

But, random guy on Internet is leaning towards no. Hmm… That’s a tough one.

If anything, Tom’s customers likely represent a more informed sample of the overall car buying population. They have to be aware that agents exist who can help them acquire a car at the best price, and they have likely done enough research to decide what car they want and (hopefully) what they are willing to pay for it.

So Tom, writing something like this for the people not using his services, is probably combining some personal experience and some researched data to offer something that could be very helpful to the general car-buying public.

Bingo…my clients are not taking out 100 month loans. But I often write articles to a wider audience that may not be as financially savvy. I try to avoid absolutes like the Dave Ramsey cult “Always pay cash, never ever lease!”

That Dave Ramsey financial advice is definitely hurting people who don’t realize that completely avoiding credit makes life more expensive.

I’ve read your stuff for many years over on the other site and here. You definitely have a much more realistic view and offer good advice to the general public while recognizing that circumstances differ.

I mostly agree with you, but Tom did provide an option that gives them a 3 year old or less car that’s always under warranty for 108 months for their $500/month.

Tom, I just wanted to let you know that reading your articles changed my mind about leasing. All my life, I bought cheap, used cars (usually German) and fixed them up. I had a lot of fun doing that, especially now that I have a garage, Quick Jacks, etc.

However, life changes and I’ve wanted to spend more time work friends and family and less time fixing oil leaks on BMWs.

I got a great lease deal on a 2025 Ioniq 5, installed an EVSE in my garage, and couldn’t be happier. With what I’m saving in parts costs and fuel, my monthly expenses have decreased slightly. Importantly, I have so much more free time on my hands.

I never would have considered this a few years ago, since so many people told me that leasing a car is just throwing away money.

I just want to say you have one of my favorite first names

Hey cool! Hi Micah!

Don’t get to say that every day 🙂

When one of my friends was widowed, she started leasing. Her husband used to maintain the cars and she just wanted things to be safe and simple.

If the important thing to someone is payment, leasing makes a lot of sense. You can stay in new cars with warranties and probably service contracts for a payment that’s not too bad. Sure, going from lease to lease means you never own the car, but the people making buying decisions on monthly payment are often going from loan to loan anyway.

And a nice thing about most leases is that you can buy them out if you decide you want to own the car (or just to sell it if the residual is lower than the value).

That said, 100 months is wild. My last car loan was a 36 month loan I paid off in a year, but I can understand a 60 month. 72 month makes me nervous, but I understand how people end up there. Any more and it’s just too long, too much interest, and just an obviously bad idea, I think.

Buy an older, RELIABLE car for cash. Learn to work on it yourself. With all of the youtube content out there there’s literally no reason you can’t learn to do at least minor things to a car yourself.

Assuming you have the space. And the time. And the tools. And it doesn’t break in winter when you don’t have a garage.

And older, reliable cars that are easy to work on are getting long in the tooth. What’s a reasonable model year for a car that you don’t need a computer to do repairs on now? 2010? Maybe 2015? Like, yeah, I can do routine maintenance on my 2013 (although I don’t do oil changes, that’s well worth paying someone) but if something electronic went I’d be fucked.

Ha ha. No. Older to me is the 90’s. Maybe early 2000’s. Kids, Lol. Electronics really have nothing to do with it in my book. There are cars out there that have reliable electronics. If I have to be more specific. Get a toyota or honda from the 90’s or early 2000’s. The average car payment is now over $700 a month. I can guarantee that you’ll spend less in maintenance costs per month on one of these cars. Or almost anything for that matter. Even if you have to pay someone else to do it.

This has been my approach since 2021, I currently own both a 2003 Civic and a 2013 Civic. I will say this, my 03 feels demonstrably less sturdy or safe than my 2013. I know we all like to complain about complexity weight, and unneeded features around here. I do as well, but my 13 is simply a nicer, and safer driving experience.

Yes, I paid more than 10x for the newer one than the older one; but also I have ABS, traction control, a backup camera, etc… While that adds complexity and cost to maintain and repair, it also makes daily use much better. Driving my 03 in a sleet storm is a puckering experience, I’ve grown up in this weather and can handle it, but the 13 just handles it more elegantly.

I would not want to drive anything from the 1990s as a daily commuter, especially with my children in it.

Any Toyota or Honda from the 90’s-00’s within 400 miles of here is either dust in the wind, or soon to be dust in the wind.

I totally recommend for those with the desire to do the work and the flexibility to do the work, yeah rock on with the old cars and the wrenching. But deep in the Northeast, it’s basically winter 5 months a year here. And any old cheap car is miserable to work on. It’s way more practical to take that sort of thing on as a passionate hobby, than it is to depend on something old and rusty to get you to work. The environment is simply awful to cars here.

Sunday’s forecast is a high of 9F, and a low of -16F. It’s times like these that I’m glad I’m not doing a brake job on a 20 year old Honda.

As evidenced by today’s Shitbox Showdown, if I lived in Oregon, I would exclusively drive 90’s-00’s cars. I can’t even believe what that RAV4 looks like.

THIS. Most cars approaching even approaching ten years old are going to suck to work on, and like you said, the weather. Last winter I was out in the driveway at 25 degrees because a brake caliper decided to seize on my 4Runner.

I’m over 40 now, I’ve been doing that shit since I was 16. I remember laying on my back in the snow in the driveway pulling the driveshaft out of my K10 to replace a worn u-joint because I wanted to go out and play in the snow with it.

I just bought my first brand new vehicle because I want to just drive.

I’ve done the old beater thing and having brake lines randomly blow out on you because of rust is no fun.

In my 20’s, I was totally willing to do fluids, brake jobs, various other improvements to my cars. Making a weekend out of such things was fun for me (well, until I had exhausted a full can of PB Blaster and was resorting to heat for damn near every nut and bolt for damn near every project).

I’m in my late 30’s with two kids. It may seem counter-intuitive, but I cannot afford to spend a weekend panicking about having my car operational for work and school dropoff by Monday. I have a totally different set of responsibilities now.

I have no problem with people taking these sorts of things into their own hands and putting their time, effort, and investment (tools and such aren’t free) into making their source of transportation as cheap as possible. Totally cool. But let’s not kid ourselves, there’s an opportunity cost to doing this.

Absolutely! I don’t have kids, but I’d rather be out on a Saturday mountain biking with friends or hiking with my GF and the dogs. Too many weekends this past summer were spend dealing with my rusty ass 4Runner, while the GF and dogs watched Law & Order.

And even taking it to a shop can be a hassle if you don’t have a trusted local guy, and an extra car to get to work while it’s in the shop.

Stuff piled up on my 4Runner before I traded it because I just did not have the time to get it to the specialist shop I wanted to use.

I’m 40.

And any car from before 2005 here in New England is going to be extremely rusted, extremely unreliable, or not a good deal.

I looked within 50 miles of my town – there are 7 cars from before 2006 available. 2 volvos and 2 BMWs which aren’t really likely to have low cost of ownership. A 2000 Sebring which I’ll admit I’m not sure of the reliability on those. Then an Infinity QX4 and a Honda Civic – assuming the Infinity shares most of its parts with whatever the Nissan equivalent was, these are the 2 that I’d consider potentially reliable and cheap. And you’d have to hope they aren’t rusted to shit.

Finding a low-cost, 20+ year old car that’s actually reliable in a place where they use a lot of salt in the winter is like finding a unicorn.

God, people who this shit are one of my least favorite types of people.

This is a country where *the majority of households* can not afford a $400 emergency, and your advice is to spend tens of thousands of dollars out of pocket?!

It’s not bad advice, but you’re right, so many people are paycheck to paycheck, it’s really hard to save for anything.

I still think it’s overall bad advice anyway. Think about loan interest as what economists call “opportunity cost”. How much are you willing to pay to do or have something.

In the case of a loan, the interest is the cost of being able to keep the money you would otherwise have paid upfront.

So let’s say you could pay $15,000 upfront for a used car, or get a loan. How much would you be willing to pay to have that money in your bank account?

That is entirely dependent on how the loan rate and what I can earn on the money. I started buying used cars with cash about 15 years ago. However, the my last used car I took the loan because the rate was 2.75% and I could earn 8% on the money in a ibond.

However, Jsloden wasn’t talking about paying tens of thousands of pocket to buy a car. Notice he said something like a 90’s Honda or Toyota. I personally wouldn’t go that old but even cars from the 00’s are cheap.

2004 Civic for $3,750

https://www.facebook.com/marketplace/item/1478092483435227/?ref=search&referral_code=null&referral_story_type=post&tracking=browse_serp%3Ac4b63951-a1fe-49e1-9fdb-69b8acffbfc8

Or maybe something like this 2002 Ford Ranger for $4,500

https://www.facebook.com/marketplace/item/3511194965702516/?ref=browse_tab&referral_code=marketplace_top_picks&referral_story_type=top_picks

No, mainly because most people don’t have tens of thousands of dollars in their pocket. The average car payment now is about about $750. All I’m saying is that if people just saved that money for a few months you could purchase completely reliable transportation. I’ve been doing this for decades. Sure, some of them need a few minor repairs but it sure beat spending $750 a month for 7-10 years. I haven’t had a car payment in over 20 years.

I’m going to reply to my own comment here. Didn’t realize I would get this many responses. I understand that not everyone has the skills, tools, or the weather to work on their own car. I still stand by the fact that you will still spend a lot less than the average car payment in maintenance every month on an older, reliable car. Even if you have to pay someone else to work on it. People will find any reason they can to justify a car payment I guess.

Some people do not have the tools, space, time, skill, to do all the necessary repairs to used beaters. It can be a gamble on a few year old car that still costs $20-25K, repairs can be very expensive. Some people do not have the knowledge or time to take months to used car shop. We need better public transportation and more cheap cars. Buying more than you need is not smart but buying low priced new and keeping the nice reliable warrantied car works for some people. All of our current cars we bought new and they are all paid off and in great shape and they are from 6-13 years old now.

Space is a big one. With fewer people being able to afford homes, even if one CAN do the work, having a spot to do it is tough, especially in areas that experience bad weather. I’ve always wrenched on my own stuff, but I don’t even have a driveway, I’ve done brake jobs, replaced radiators, and so on while street parked. It’s no fun and honestly, I’m getting too old for that shite. I’ve realized time is valuable and my weekends are better spent elsewhere.

This is a big one. I live in an apartment and have a space and I am lucky enough that I can handle some basic maintenance things here and not create a mess (tarp down for oil changes just in case, stuff like that). I have the tools and can replace things here and there, but for bigger jobs, there’s no choice but to go to a shop. I’m also lucky that my engine bay is not cramped with everything squished together so that helps.

I always did my oil changes in the street too. I actually kind of enjoyed that, but sometimes it WAS a PITA.

With my new truck under warranty, I’ll probably have the dealer do the oil changes just to have them be on the service records. Oil changes look like cake on this thing though, it sits up high enough that I don’t need ramps, and the drain plug and normal cannister style oil filter are easily accessed without removing any skid plates.

My old lifted ZJ Grand Cherokee was like this, SO easy to work on. I would totally daily one of those again if they weren’t all rotted into the ground here.

My 4runner needed ramps, I had to unbolt the skid, and I needed to clean and put new O-Rings on the plastic filter housing.

Yeah, I’ve got an ’07 FJ Cruiser on 33s so I can scoot underneath it without a problem. The aftermarket skid has a hole in it for where the oil drains, which makes that a one step part of the job. The oil filter is at the front of the engine and accessible just standing in front of the truck so that’s also easy. Because the bay is still kind of ‘old’ with the layout, I can get in and do plugs, I’ve replaced O2 sensors, etc. without much of a problem and no one is the wiser. Unfortunately for brakes and stuff, I gotta go to the mechanic. I can’t imagine trying to do that kind of thing on the streets lol

I did change the shocks on my JKU in the driveway and did not even need to lift it as I fit under just fine. BUT for most of the repairs my time and age and income means my time is worth something to me so I pay for anything that may make me not have the car the next day for work. My friends who always work on everything on their 25+ year old rusty rigs are so cheap that they do not value their time at all.

Back in the day I’d change shocks on my ZJ with it on the ground and the wheels on. Nice having a vehicle where the shock does not also hold up the weight of the vehicle.

Soon auto loans will require the equivalent of PMI on a mortgage.

GAP insurance is the PMI. I don’t know if these loans require you to carry it, but I suspect they will require it soon if they don’t already.

More commissions for the closer at the dealership.

Forgot about that. Thanks.

I bought my first new car in 1997. It was a 60 month loan. At the time, most loans were still 48, some only 36. 60 was a bit of a stretch. My how times have changed.

60 months makes me sweat a little. 72 – I get a little fidgety. 84 – and I’m nauseous.

Taking a 100 month loan on a car would have me actively vomiting. Probably as a defense mechanism to make it impossible to sign paperwork.

Hell of a story for the sales people tho!

Just a Team America style, 2 minute long scene of me filling up a finance office with every fluid ounce of stomach volume.

Fuck yeah!

(ahem)

I recently took out a 72. The thought of making payments that long gives me anxiety, I have plans to pay it off within 48.

My last vehicle I financed in 2019 for 60 months, I paid it off in about 24. Then I kept making the same payment to my bank account every month, so I had a nice chunk to put down on my new truck. Even though it was more than 2X what I paid for my last vehicle, the payment is about the same, adjusted for inflation.

My most recent purchase was a 3 year old minivan that I took a 4 year loan on. I do NOT like owing money on a vehicle that’s 7 years old. The intent was to pay it off in 3 years, and I did. It made more sense to take the 4 year loan just in case of life shenanigans.

My rule of thumb is to have whatever car I’m buying paid off by the end of whatever warranty it might be covered by. But this is why I find some of the used cars people tout here to be a bit unappealing. Let’s say there’s a used RAV4 out there for 18k that’s something like 8 years old. Even if that’s theoretically a decent deal relative to the market (seems pretty typical from listings), I either feel the need to buy that in cash, (I’m not struggling, but that would theoretically empty my cash savings) or put enough down and take a measly loan out. It’s sort of a no-mans land for car buying, and oddly a significant risk in that while it may be a car with a great reputation, it’s still an 8 year old car I’m taking a risk on.

Sort of an endless tangent but yeah, I think I’d rather be in the business of buying new or lightly used, or even a beater, than that weird in between space where the car seems to still be overvalued yet still represents a major cash outlay, combined with significant risk.

36 months and 10,000 miles?

That’s 64 miles a week. You could do that just with alternate side of the street parking in Brooklyn.

10k miles PER YEAR.

Ok, 192 miles a week is still not much. Not enough for commuting to a job 20 miles away and zero other use for example.

When my kids were tiny we did not go around much. I returned my 3-year lease (Ford Transit Connect, great car, but down on power) with only 9200 miles on the clock.

As the kids grow bigger and more annoying the odo readings got closer and closer to the full lease mileage allotment. Not that it mattered–one was totaled in 4 months (fuckin’ jabroni ran the red light), one was sold to Carmax (thanks to Covid shortage), and one was bought out at lease end.

Agreed, it’s not for “normal” people.

This only really comes up because car prices are out of this world and dealers try to entice customers with “low” (lol) monthly payments, and desperate people may actually consider this – and usually go way over the mileage allowance and still end up upside down by massive amount.

Woot, Tom here. Yay!

Good info but it seems like you are preaching to the choir at the church of Autopians. Lots of used car buyers here and I like to think as a group we understand how interest works better than the “average” person and isn’t likely to fall for 100 month financing.

That’s why you send the link to one of your friends or family members who is about to make a stupid purchase in the disparate hope that they may actually read it instead of just signing for a shiny new toy that they can’t actually afford.

Hope springs eternal.

One of my goals with my friends here at The Autopian, just like “the other site” was to present helpful, though clearly obvious to smart people, advice that gives this site reach beyond our core readers

I send your articles to people all the time. For some reason, it doesn’t stick when I explain it, but when it comes from an expert on a car website, it does. I love your articles and hope to see more of you around here!

This actually reminded me of the glovebox. Good place to put this article so that I can forward it to certain people who think their entry level office job should be rewarded with a brand new 4Runner (not a joke).

Sure, but I’m still happy to read it and happy to see this message get out to as many people as possible.

After all, I rely on new car lessees/buyers so that there are used cars for me later.

For some reason, my Facebook reel sewer pipe has been serving me up hot steaming rage bait from this Houston BHPH dealership (“got you rollin” ?) full of … uh … customers supposedly dropping 90 or 100K on a 6 year old hellcat with a 100+ month note.

We can math it all day, but even if this was real (and I believe it’s not far from the truth), I don’t think buyers in this position care. They’re going repo-to-repo, chasing shreds of their credit down a spiral. Ownership isn’t even the point.

I am appalled by this. I don’t drive much so I can get away with practicing bangernomics and some of my neighbors do too based on the number of 20-30 year old daily drivers I see.

I am fortunate to have the resources in space, tools and backup vehicles, so I can run cheap old cars, as long as I avoid German luxury cars.