The total amount of automotive debt in the United States is now at a level that exceeds the Gross Domestic Product of Turkey. That’s a lot of automotive debt, although it’s not necessarily a bad thing. Don’t let it scare you. It’s not the end of the world, yet.

Will that number rise next year? Yeah, probably. I have no crystal ball, nor does The Morning Dump ever achieve perfect foresight. Honestly, sometimes my hindsight is suspect. Here’s a prognostication: Incentives for gasoline-powered cars will likely increase, but not enough to offset the price increases next year.

Aston Martin isn’t waiting to find out and is therefore going to cut its workforce by about 20% as it tries to survive the downturn. Nissan, on the other hand, is going to double the number of Pathfinders. I wonder if that’ll work.

Debt Isn’t Bad Until It Is

I did not watch the State of the Union last night. It was clear it was going to be long, and I thought the time would be better spent sleeping rather than seeing if some White House staffer’s Kalshi prop bet pays off.

The full transcript is available over at the AP, and my general view is: I ain’t reading all that. I’m happy for you, though, or sorry that happened. Don’t tell Robert Caro, but I didn’t turn every page. I just did a Ctrl+F for the word “auto” and came up with this:

The cost of chicken, butter, fruit, hotels, automobiles, rent is lower today than when I took office by a lot. And even beef, which was very high, is starting to come down significantly. Just hold on a little while. We’ll get that down. And soon you will see numbers that few people would think were possible to achieve just a short time ago.

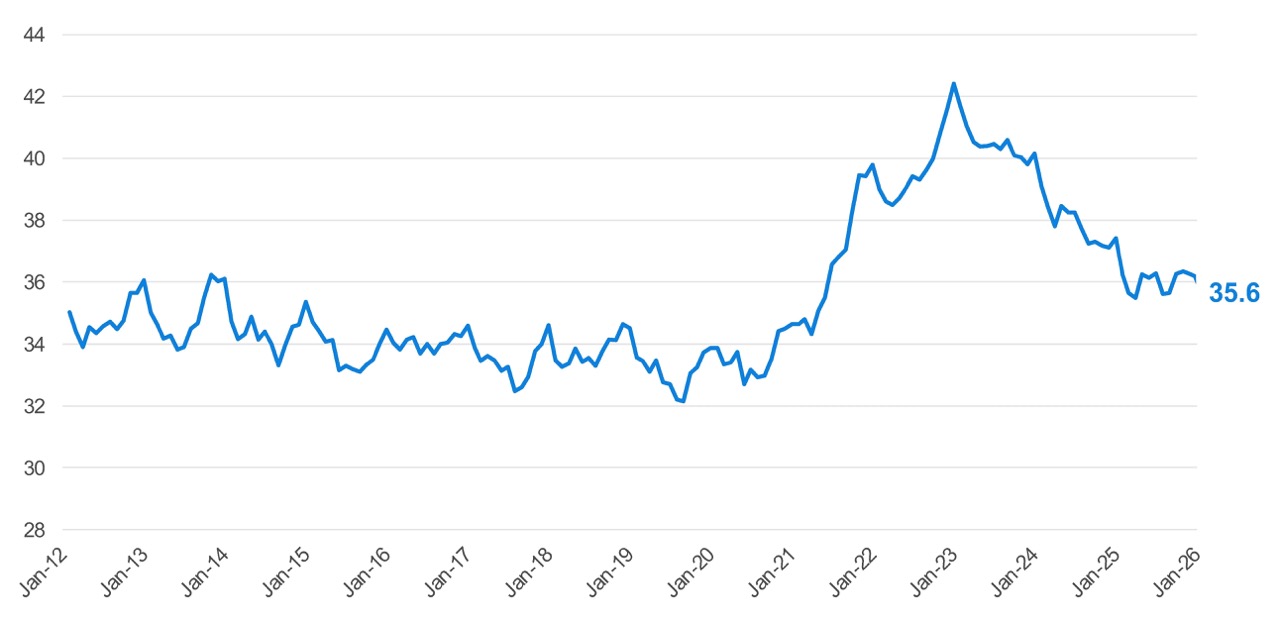

I will only speak to the automotive part of it; that’s maybe true if you compare January of this year to January of last year and look, specifically, at affordability. Here’s Cox Automotive on the costs:

New-vehicle affordability in January was better than a year ago, when prices were 1.9% lower but interest rates were higher. Incomes were also lower a year ago. January incentives were 6.4% lower than a year ago, yet affordability still improved – a sign that macro tailwinds from lower rates and higher incomes continue to outweigh reduced manufacturer support. The new-vehicle affordability index fell by 1.8% year over year, indicating affordability improved last month. A year earlier, it required 36.2 weeks of median income to purchase the average new vehicle.

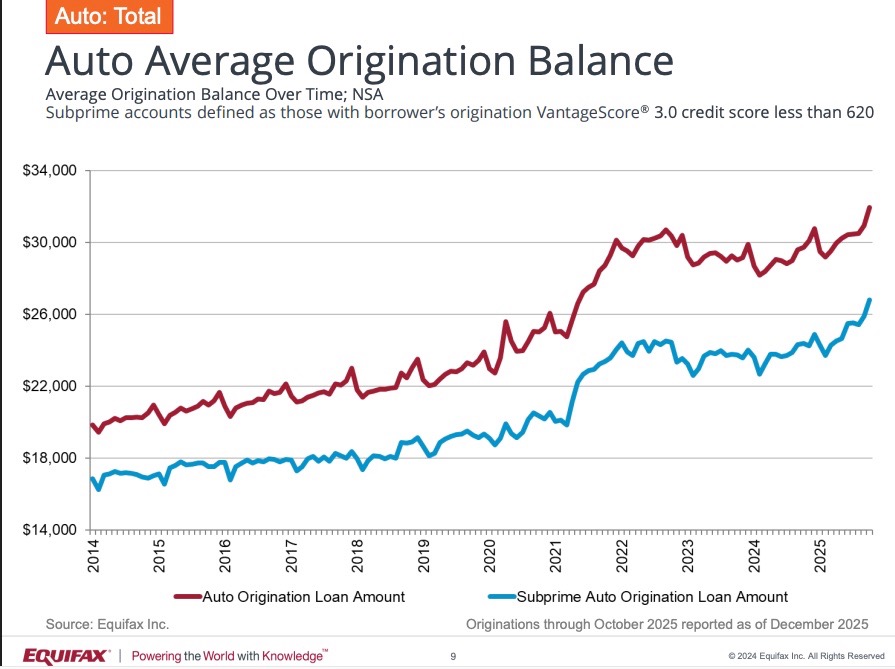

The cost of cars built outside of the U.S. (and thus the overall average) has gone up a lot, though, and terms have gotten longer, which means that the total amount people have spent financing cars has risen to new heights. According to Equifax, the total amount of automotive loan debt reached about $1.589 trillion in December of 2025, which is up by about 0.6% year-over-year. Add in leases, and that number grows to $1.685 trillion.

What you have to worry about with auto loans is not specifically the size, although it’s a fun number to put in the headline. It’s who is getting those loans and for what. Are subprime buyers taking a bunch of loans on wildly depreciating cars? Are delinquencies getting out of control? Equifax’s analysts don’t seem to think so:

Severe auto delinquency (share of balance 60+ DPD increased to 1.61%, up three basis points year-over-year, while auto write-offs decreased to 25.9 basis points. Delinquency trends have remained largely stable since late 2023, including within the subprime segment, where auto loans continue to rank as the top payment priority for borrowers.

There’s nothing about this that seems extreme. We’re now on year three of me writing about the bad loan vintages from the pandemic, and those haven’t all been paid off yet.

Here’s what stands out to me, though:

The average origination balance for all auto loans and leases issued in October 2025 was $31,962. This is a 7.6% increase from October 2024. The average subprime loan amount was $26,813. This is a 10.0% increase compared to October 2024.

This is the reality of today. Car prices have slightly improved, and the slow lowering of interest rates is, finally, starting to positively impact car buyers. To meet monthly payments, though, consumers are stretching further and further out into the future.

Again, it’s one of those situations where it’s not bad until it is. If unemployment stays low and the economy grows, then those loans are probably fine. President Trump said many times last night that the economy is strong and “roaring like never before.”

If the economy does stumble, though, and car values drop, then the underlying value of these cars will go down, and buyers will find themselves even more upside down as the loan term extends off into 60, 70, or even 80 months.

Cars Are Probably Not Going To Get Cheaper, Even If They Become More Affordable

Affordability is not that complex a metric, which is why it amuses me that it’s often misunderstood. When it comes to things you buy directly, affordability is a measure of the price of that object relative to your income. When it comes to things you finance, there’s the added dimension of the cost of borrowing.

The chart above is the Cox Automotive/Moody’s Analytics Vehicle Affordability Index referenced in the first story, which looks at how many weeks of income the average household needs in order to buy the average new car. This number spiked during the pandemic and has sort of flatlined this year as financing got easier, but cars really didn’t get cheaper.

With flat sales this year, it’s likely that some incentives will be out there in the market. Will this make cars cheaper? Probably not, as pointed out in this Detroit Free Press article on incentives and car sales:

“Our full year 2026 forecast is that incentives will increase $400 to $3,500, but given that last year had such a substantial electric vehicle incentive spend in the baseline, the true change is over $500 for (gasoline) powered cars,” Tyson Jominy, vice president of data and analytics at J.D. Power, told the Detroit Free Press.

How each automaker spends that extra $500 or more in incentive money will vary depending on their inventory and cost pressures, he said, and the competition for sales might not mean car buyers walk away paying less.

“Consumers will see higher transaction prices net of incentives on average, because automakers continue to increase (Manufacturer Suggested Retail Prices),” Jominy said. “Final transaction prices (for the full year) are expected to average $46,600, an increase of $800 versus 2025.”

With refunds coming, many buyers might have a slightly higher household income this year. If interest rates come down, then borrowing money gets cheaper. At the same time, if loans get longer, the total cost of a car then goes up.

Ultimately, it depends a lot on the car you want and the buyer you are. If you’ve got cash and you want something from a brand that’s trying to grow this year, then you might get a deal. If you’re financing a Tacoma, it might be a bit tougher.

Aston Martin Cuts 20% Of Staff

It’s been a while since I’ve driven an Aston Martin. I should fix that. Unfortunately for Aston Martin, the company sells many of its cars in the United States but does not build them here. Perhaps an Alabama Aston plant next year?

Blaming tariffs, the company is cutting.

Aston Martin, which has its headquarters in Gaydon, Warwickshire, employs about 3,000 people, meaning job losses will total around 600.

The firm said the job cuts should deliver annual savings of around £40m and did not specify when the job cuts would be implemented, but said most of the savings would be made this year.

A spokesperson for Aston Martin said US tariffs had been “extremely disruptive” and demand had also been “extremely subdued” in China, the world’s biggest auto market.

It has also trimmed its five-year capital spending plan to £1.7bn from £2bn by delaying investment in electric vehicle technology.

Clearly, the answer is to bring back the Cygnet.

Inside You, Are Two Nissan Pathfinders

The Nissan Pathfinder was once a stout body-on-frame SUV. Then it became a unibody blob. Now it’s a unibody car that looks like it could be a body-on-frame SUV.

Why can’t we have both?

According to Automotive News, that’s exactly what’s happening.

According to a person with knowledge of the plan, Nissan will continue selling an updated version of the unibody Pathfinder alongside a new body-on-frame model as soon as mid-2029.

This expanded Pathfinder lineup aims to target different buyer preferences: the unibody entry for those seeking affordability, car-like comfort and family practicality, and the truck-based variant for customers who demand a rugged aesthetic and greater capability.

The duration of the models overlapping in the market remains flexible and would depend on sales performance.

Will… will they both be called Pathfinder? That’s wild.

What I’m Listening To While Writing TMD

Have I really never done Paramore’s “Misery Business” for my TMD song? Hayley Williams remains undefeated in my book.

The Big Question

What’s the best example of a car or truck completely abandoning its customers from one generation to the next?

Top photo: Subaru/DepositPhotos.com

> higher incomes

Where are those, exactly?

I just want to say great topshot image creation today.

And great song.

Absolutely no one is forcing anyone to spend $60k, 70k or more on a car. There are plenty of options out there for 1/2 that be they some of the cheaper new cars available now or 1 or 2 year old models.

The automotive press never misses an opportunity to reiterate that “NeW CaR PrIcEs AvErAgE $50k”. Stop being a fucken lemming and buy what you can actually afford. And just because you qualify for financing, does not mean you can actually afford it.

When the Saturn S-series rolled into the L-series, the new cars lost most of the appeal that the S-series had cultivated. This problem repeated when the L-series was replaced.

The rebooted Ranger, Maverick, Blazer, Trailblazer, Cherokee, Gladiator, etc. are very different from their earlier generations, but the time gap helps dull the impact of those changes.

The new Outback has abandoned its wagon-focused customers. Time will tell, but I’m not convinced Subaru needs another crossover to wedge between the (enlarged) Forester and the Ascent.

The 4th gen Sienna no longer has removable rear seats, so 4×8 sheets don’t fit on the floor anymore. This doesn’t matter to every Sienna customer, but it does abandon the segment of customers that want to be able to do handyman or contractor work.

The Ford Probe also comes to mind…

That first graph and data is almost useless as it doesn’t account for inflation.

It illustrates inflation.

I love the camber of the wheels in the top shot. I laughed hard the second I saw the picture. Nice job, whoever came up with the concept and whoever executed it. Could be the same person.

TBQ: Like a lot of commenters, I read that as which car *company* abandoned a generation of fans. At first I thought Jaguar, but the dayglo objets d’art they last rolled out don’t really have customers, and a carmaker that doesn’t make cars has problems that surmount brand loyalty.

That leaves Saab. The last generations of their cars were either heavily diluted by their corporate master or outright rebadge jobs. Saab lovers wanted weird and got Opels.

Which car? Mitsubishi Eclipse leaps out, but there was a half-decade gap between the current SUV incarnation and the final two-door, and the last of those cars were already a sad shadow of what they’d been.

I’m going to say Land Cruiser, at least in the U.S. The current model is more like a 4Runner than what the brand has meant here in America: a full-size off-roader built more to a standard than a marketing strategy. I wish Toyota would let us have a 300 series cake without all the Lexus icing.

There were two major shifts in economic policy over the last 50-60 years – the first was a shift away from focusing on wages to focusing on consumption, in which cheap consumer imports effectively began being used to compensate for wage stagnation. The second was a significant expansion of consumer credit to compensate for the same for all the things that either couldn’t be manufactured abroad or weren’t actually cheaper that way. The two big effects of this were a massive widening of wealth inequality and an enormous increase in consumer debt, which meant that a substantial portion of what remained of consumers’ income was increasingly going to debt service on, eg, house, car, education, and medical payments.

If that all sounds unsustainable to you, well, I guess you don’t work at the fed.

Makes sense, but what policies can be used to go back to focusing on wages and reducing consumption?

Regarding wages, unions are the big ones, and federal purchasing policy & standards are also an enormous lever here – even just through the DoD, the fed is an enormous purchaser, and putting rules in place and adjusting bid scoring around labor standards for suppliers, contractors, and subcontractors would be huge. Trade agreements have been used to do similar in the past – we use them to strong arm our partners into enforcing a bunch of other policies we want (hello intellectual property), we can use them to influence labor policies as well. The chicken and egg problem right now is that wages are so far below where they need to be – we’re talking integer multiples – that policies which may raise prices need to be very carefully designed or they’re going to sink the average family. You need the wages immediately.

Regarding reducing consumption – this is an interesting phrase, because it implies people getting by with less. That’s not actually a requirement here – a bunch of the stuff we buy right now is, frankly, garbage – cheap electronics designed to break after a year, cheap clothing that wears out quickly, etc. To the consumer, getting, say, one pair of good shoes which lasts a decade is probably better than having to buy new shoes every year, but that shows up as “less consumption” in the numbers. This is the whole “Degrowth” argument – a huge amount of our consumption is wasteful, not in a “why did you buy that luxury” sense, but a “why did that break so quickly” sense.

There’s always a question of “where’s the money come from” for this, and a huge part of that is reducing wealth inequality. Jeff Bezos bought a yacht so big he needed to negotiate with the Netherlands to get it out to sea, and it had no material impact on his wealth (ditto the WaPo, which he’s now gutting), and meanwhile we’re arguing that we don’t have money to pay for schools or health care for veterans. I’m not sure people quite recognize both the scale and the impact of the kind of economic inequality we’ve got right now, but a big part of this is going to have to be less money in Bezos’ pocket and more in yours.

So, so many recession signs out there. Amazed by our economy’s resilience in 2025. We’ll see how long it can last.

It’s because we’re having an AI bubble at the same time we’re having a recession. When people catch on that AI is nothing more than glorified autofill, we’re in for some serious financial pain.

Cars are expensive, gotta get the money somewhere.

We need a economic professional to actually answer whether it is good or bad that our car loan balance matches Turkey. In addition come Thanksgiving when Turkey is substantially cheaper is that better or worse for the GNP?

NSX. The way Honda understood the car as a technology demonstrator was largely at odds to the way people saw them as reliable, semi-exotic driver’s cars. The technology of the past made the NSX a driver’s car and making a driver’s car was a way to showcase tech back then, hence the Senna development help, but when the new one was developed, tech had become antithetical to being a driver’s car, so the tech was geared more toward increasing efficiency and performance along with electronic driver’s “aid”, which ended up disappointing people who saw the car differently than its creator. Being ugly-bland didn’t help, either.

Careful with that lead image, you’ll have some stanceboi wanting to do unspeakable things to a Crosstrek…

This is my main takeaway from TMD today. I think the giant pile-o-cash is giving full length roof-top box vibes to go with the stance. Nice.

A bit of a non-sequitur, but I saw an example just before I saw your reply. My “favorite” use of roof top boxes is seeing a full-sized pickup with a hard tonneau cover with crossbars over the bed and at least one roof top box (I’ve seen two) mounted to the crossbars.

WOW, if only you had a vehicle with a large, secure, weatherproof storage area…

Around here that seems really popular with Rivians. I could maybe understand it if the bars were at the height of the cab so you could still put something big in the bed. But of course it is all about the “lifestyle”.

Aerodynamics wants to have a word with you here…

I get the not putting them on the roof, it’s the idea of securing and weatherproofing the large cargo area only to add the cost of putting a much smaller weatherproofed cargo area on top when you also have a quadcab (as the majority of trucks sold are).

It kind of feels like a “Yo Dawg, I hear you like weatherproof cargo areas…” scenario.

Eh… Maybe they need the extra lockable storage of the “roof top” box?

As we know, aerodynamics plays a much larger role with the BEV Rivian truck another commenter references, and in BEVs in general.

Curious how Ford’s new BEV truck (Universal Electric Vehicle Platform) that makes so much hoopla about aerodynamics and efficiency really pans out.

“Severe auto delinquency”

I wonder what class of vehicle has the most delinquencies. I’m gonna guess high trim pickup trucks?

And according to this video:

https://www.youtube.com/watch?v=I9TxJXm2m9s

I guessed right… with the Ford F150 being at the top of the list.

“What’s the best example of a car or truck completely abandoning its customers from one generation to the next?”

Off the top of my head… the 2nd Gen Honda Civic CRX that was replaced with the Civic Del Sol. The Del Sol is NOT what 2nd gen CRX owners wanted.

And the 3rd gen North American Ford Ranger to the 4th gen Ranger. The 3rd gen was still a small, affordable pickup truck. The 4th Gen wasn’t small nor affordable compared to the 3rd gen.

The Chevy Trailblazer… went from an actual truck on the GMT360 truck platform to a weaksauce CUV on the FWD-based VSS-F platform.

And the Trailblazer used to be bigger than the Blazer. But now we live in an upside down world where the Blazer is bigger than the Trailblazer.

Well the F-150 and Silverado are the two best selling vehicles in the US so it isn’t surprising that they are at the top when you talk total numbers. The real repo kings are the Altima and Charger/Challenger as they are near the top of the list of cars the repo man comes for yet are way way down on the sales charts.

President PDFile Protector says a lot of things that aren’t true and you shouldn’t repeat them (especially unremarked-upon) on a site with this much reach. Shame on you.

Exactly this!

Agreed. “Don’t print lies in the paper” is the saying I keep leaning on.

The fact checkers are still standing around waiting to do their job, as soon as a real fact is voiced.

He did actually say that, but there were so many…..untruths that if you were playing a drinking game you would have been out at the 1hr15 min mark. I lasted until 10:25. It was like being at a rally speech. Drug costs down 500-600%? Yeah, wow what a numbers-oriented businessman. BTW, how is the USFL and Atlantic City doing?

Yeah, especially since this is one of those things that’s objectively untrue by basically any metric.

It’s not the first time the Pathfinder has changed form unibody to BOF:

It’s been all over the place.

So assuming sales are satisfactory, I assume the unibody Pathfinder will just be in production until some regulation makes it not worthwhile to update. Less like an “Acadia Limited” where they overlap the two generations, more like the late Grand Caravan. The QX60 is reportedly going BoF, so will the old also continue on? Can it get the VQ back if so?

Or – it’s a Bronco & Bronco Sport line situation.

S-Series -> ION

VUE 1st gen -> 2nd gen

Olds Cutlibu comes to mind but that was just a stopgap anyway.

Pontiac Bonneville G?

KL Cherokee going away with no direct replacement in any CDJR brand. Move down to a Compass, or gamble on a Hornet?

Not having a car payment has been absolutely huge for me. I would have very little left for saving now that everything else is ridiculously expensive.

As much as I’d love to get a second sporty car for weekend trips, I can’t see myself taking on a car payment again anytime soon. It just doesn’t make sense to take that on when I don’t have to, considering how expensive life’s necessities have gotten.

I really feel for people stuck with loans for their primary vehicle. If you’re not filthy, unethically rich, life’s rough these days.

I will vs be looking to buy something for cash before long. Driving a 6mt vw sportwagen I bought for $5k right now. Bought it hi mi and a bit rusty, but Ill have gotten 3 years and 50000 mi out of it when I am done with it

“The Nissan Pathfinder was once a stout body-on-frame SUV. Then it became a unibody blob. Now it’s a unibody car that looks like it could be a body-on-frame SUV.

Why can’t we have both?

According to Automotive News, that’s exactly what’s happening”

That’s essentially what Toyota did with the 4Runner and Highlander: provide both a road-going and traditional BOF model in the midsize SUV segment. Twenty years ago. It was questioned at the time, but it looks pretty smart now. Way to stay ahead of the curve, Nissan!

Jeep and Ford did similar I suppose, with the Wrangler and Bronco, though as open-roof vehicles those are a little more niche.

QuesOTD:

There are a lot of models that abandoned customers with a redesign. Pathfinder is a good one. I’ll just expand on that and say Nissan/Infiniti as a brand abandoned its customers in fairly short order back in the aughts. I think you’d be hard pressed to find an entire major automaker who did this so thoroughly. Maybe Cadillac when they dropped land yachts for Arts and Science BMW clones.

Not a car specifically, but I feel like between 2015 and 2020 VW completely alienated the sort of people who historically bought their cars.

Agreed, and surprised I didn’t think of this. Had a 2010 Sportwagen I loved. There’s nothing for me there now.

I’ve got a 2014 Sportwagen that I will be holding onto for as long as possible. There’s not a thing VW sells in the US today that I’d buy. I had a CC and a GTI before the Sportwagen, but if I got a new car today it wouldn’t be a VW.

I am driving a 2010 $5k example 6mt 3 years ago, kinda rusty, but i will go down that road again after next year I think. The MT makes them more affordable, but yes, a new vw or not any new car is in the cards

I would say, on some level, they are continuing to doing so today.

Literally zero of the people I knew to be VW cultists in the 00’s and 10’s own a VW now. None. That seems pretty alarming to me.

Roughly half of them “won’t be screwed again”. The other half contend that the brand offers them nothing they would buy anymore, which is true. Soooooo, yeah I would have to agree with you.

The whole “VW is a luxury brand” that started in the 2000s was stupid and alienated the truly traditional VW customer.

I recall they were targeting Mercedes with VW and BMW with Audi.

Yeah I don’t think they succeeded in getting Merc buyers to cross-shop against VW products.

Not that any part of that plan was a particularly good idea, but I’d say VAG got their potential matchups backwards…

I agree. We had one or two VW cars in the garage over nearly 30 years. Now both bays are filled with Chevrolets: a Volt and a Colorado. Couldn’t be happier.

Yknow if we take all of these extra-long car payment loans, bundle em into securities and sell em to investors there could be a lotta money to be made! I’m sure this could only go well.

Genius! And activities like that clearly add value to the economy, and is not just a giant inflation generator…

Hey you just gotta remember, it will likely cause a lot of people a lot of pain in the future but in the meantime a lotta cool companies will be made so its all good

That’s such a great idea I bet you could make mint betting AGAINST it somehow…

Yeah but that assumes people would default on their extremely bad loans which as we know has never happened ever in the history of the economy ever and will definitely never happen in the future at all.

That was a movie, without the car payments. The Big Short.

It’ll go even better if large pension funds get in on the action.

I wonder if the pathfinder will be like the bronco and bronco II/sport

That’s exactly what I was thinking.

I’m sure anyone who bought a Pontiac Lemans in the late 60s/early 70s was not prepared for what they’d see in the late 80s.

I’m doing my part! I still have an outstanding balance of $153 on a car loan that I took out in December 2024.