Mark Twain once said that a lie can travel halfway around the world while the truth is still pulling on its boots. That was back when social media was what you heard in a tavern. It’s only gotten worse since, and recently, there’s been a freakout over the 15-year car loan. This doesn’t seem to be real, but it’s also not far from reality, which makes the response interesting.

The Morning Dump is wading into affordability, because that seems to be the most pressing issue for the automotive industry. This, and the potential for a 50-year home loan, has created the rumor of a car loan that could stretch to 180 months.

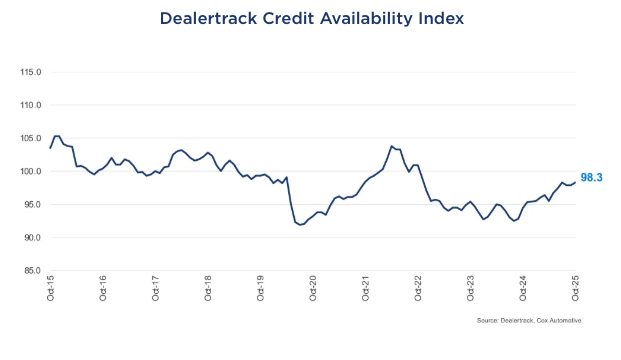

Taking a look at the overall credit market for cars, things are loosening up a little, and car loans themselves are already getting much longer. This isn’t to say all is well in the world of auto financing, as a deep dive into the failure of Tricolor shows how much fraud there potentially is in the system.

As the First Brands (they make all sorts of car parts) bankruptcy demonstrates, getting $10,000 for a car loan might be hard, but getting $100,000,000 for your company on the back of allegedly double-counted invoices is easier than you might guess.

The 15-Year Car Loan Isn’t Real

I woke up this morning and saw that the Autopian Discord (open to everyone) was excited about something. That something had been deleted, but I was able to infer and confirm that it was a rumor about the White House proposing a 15-year car loan. Specifically, there was an image going around in the White House Comms-style saying one was coming, and that Secretaries Lutnick and Duffy were working on it.

This sounded wrong for many reasons, and the post was deleted from Discord after everyone realized it was probably just some social media nonsense. I won’t link to the original because that merely reinforces the problem, but it went viral on both X and BlueSky. There’s a good fact check over on Yahoo! News, and it points out that there’s no version of the fake release on any White House-related accounts.

What tipped me off that it was probably fake was the mention of Secretary of Transportation Sean Duffy. As the old saying goes, the most dangerous place in the world is between Secretary Duffy and a camera, and he hasn’t been out there promoting this.

I think what really made this believable was that President Trump is attempting to address the housing crisis by promoting the 50-year mortgage. The idea there is to potentially lower monthly payments by stretching out the loans. Realtor.com points out one of the reasons why this might not be ideal for homebuyers, and the logic is similar to why it’s not great for people trying to finance a car:

Assuming for the sake of argument that mortgage rates were equal across both products, a 50-year mortgage would lower mortgage payments by about $250 per month on a $400,000 home, assuming 10% down and a 6.25% mortgage rate.

Total interest payments over the life of the 50-year loan would amount to $816,396, compared to $438,156 on the 30-year loan, a difference of $378,240. That amounts to 86% more interest over the life of the loan.

“Buyers do benefit from spreading out the high cost of a home purchase over a longer period, but lenders certainly benefit, too, by having a longer period to charge higher interest rates,” says Berner.

A key difference here is that the main cause of housing costs is a shortage of supply, which this doesn’t address. There’s a way to look at it where the most obvious outcome is that the addition of more buyers without more supply means higher prices. Cars don’t quite have this issue. While there’s some shortage of affordable models, carmakers can more easily turn up production of cars than homebuilders can turn up the supply of affordable housing.

However, homes tend to appreciate in value, whereas cars do exactly the opposite. The bit about interest rates is essentially the same as homes, and that’s worse because cars depreciate so quickly. Doing the math: if someone bought the average car (about $50,000) with the average down payment (about $7,500) at a better-than-average interest rate (7.00%), that person would only have a monthly payment of $382. However, that person would pay $26,261 in interest, making the total payment for the car $76,261 over 15 years. Additionally, the buyer would likely be underwater on the loan for a long period of time.

For all these reasons, a 15-year car loan probably isn’t going to be a White House priority, although there are times when it seems impossible to know these days.

The 15-Year Car Loan Isn’t As Crazy As It Sounds

Car loans are getting longer, with or without White House intervention, and buyers are increasingly underwater. The 84-month loan isn’t that unusual, and, with a slowdown in car buying, lenders are doing more to give access to buyers with lower credit scores.

According to Cox Automotive, the approval rate for auto loans in October hit 72.6%, which is down from September but up from last October. The one area of the market that expanded was subprime lending, with way longer terms being offered to buyers. The latest analysis shows that the share of loans over 72 months is 27.5%, up 300 basis points from last October.

Buyers tend to think in terms of car payments and not the overall market picture, but with rates dropping, these borrowers are not getting the best deal, as Cox points out:

The improvement was driven primarily by lenders’ increased willingness to extend credit to subprime borrowers through longer terms and lower down payments, even as overall approval rates declined. However, this expanded access came with higher yield spreads, meaning consumers paid more for financing compared to prevailing market rates.

Once again, money isn’t everything, but not having it is, especially for subprime borrowers. The longer the loan term, the higher the interest that a lender is going to provide, meaning that as rates go down, borrowers are paying even more for their money.

Tricolor Disaster Shows The Difficulties Facing Subprime Borrowers

The saga of subprime used car retailer Tricolor has revealed a lot about the underwriting practices of large institutional lenders like JPMorgan Chase, but it’s also shown how hard it is to be a subprime borrower.

There’s a great piece from Bloomberg that gets into the chain of events that led to the collapse of Tricolor, which allegedly borrowed money by using the same loans as collateral with multiple lenders. The company’s history is interesting to say the least, but what really got me is how much harder the company was on its borrowers than its lenders seem to have been on Tricolor:

Customers described aggressive sales tactics, confusion over loan documents and long delays in receiving car titles. Some said Tricolor called repeatedly when payments were late, often numerous times a day and deep into the night. Many vehicles were worn out, poorly maintained and had high mileage, according to car buyers and former employees.

Raquel Ramirez says her used GMC Yukon SUV has done nothing but give her trouble since she bought it in 2023 — it constantly jerks when she drives even after repeated repairs — and yet Tricolor staff would hound her when she fell behind on the $35,000 loan she took out. “If I missed a day of a payment, they would call until 10 at night asking for the payment,” Ramirez says.

The lack of scrutiny for massive companies isn’t just an issue with Tricolor. It’s also a key issue in the failure of First Brands.

First Brands Group’s New CEO Admits Company Faked Invoices To Get Loans

First Brands Group, the parent company of brands like Fram and Trico, declared bankruptcy in September after it was discovered that the company had massive debts it wasn’t likely to be able to pay. It was later revealed that the company’s founder, Patrick James, allegedly funneled hundreds of millions of dollars to his own personal accounts.

The company’s new interim CEO, Charles Moore, told the judge handling the bankruptcy that he discovered massive fraud at the company as soon as he arrived.

First Brands lawyers showed a 2022 message from one member of the company’s finance department to another, in which an employee suggests they may have to make “dummy invoices” to secure additional financing. In a subsequent message, a top member of the finance department doesn’t express any concerns about falsifying invoices, Moore testified. That surprised Moore, he said.

“I would think that if the notion of creating a dummy invoice was new or not happening, there would be some reaction to that,” Moore said on the witness stand.

Did you catch that? The new CEO was surprised to find out that the company’s finance department was not surprised to be asked to allegedly commit fraud in order to borrow money.

What I’m Listening To While Writing TMD

Brian kindly took over TMD yesterday, meaning that I missed the opportunity to mark the 50th anniversary of the wreck of the SS Edmund Fitzgerald by playing the eponymous song from Gordon Lightfoot. Today, I fix that.

The Big Question

What car would you take a 180-month loan to buy?

Top photo: Stellantis

“The 15-Year Car Loan Isn’t Real”

Well the fact is that 8 year loans are already terrible. In my view, the loan length should never be longer than the powertrain warranty.

“The 15-Year Car Loan Isn’t As Crazy As It Sounds”

Yes it is. If someone can’t afford a payment term that is no longer than the powertrain warranty, then they need to go for something cheaper or forego getting a new ride and hang on to their current ride (if possible).

“Buyers tend to think in terms of car payments ”

And those buyers are idiots.

And not all buyers think that way. Some buyers (like me) think in terms of Total Cost of Ownership… where ALL costs (including insurance, maintenance, repair costs of common repairs, fuel/operating costs, taxation, reliability and durability) are factored in, compared and considered.

“Raquel Ramirez says her used GMC Yukon SUV has done nothing but give her trouble since she bought it in 2023 — it constantly jerks when she drives even after repeated repairs”

Hey Raquel… did you inspect the vehicle yourself or have an independent mechanic do that BEFORE you bought it? Did you do a thorough test drive?

Or did you buy that stupid Yukon thinking “I get so much vehicle for my money” without doing any real homework?

And have you put any effort into diagnosing/fixing the issue yourself?

Some may call this “blame the victim”. But when people make stupid decisions, don’t do their homework and cause the bad situations they are in and then complain in a way that suggest they want someone else to fix their problem, I have trouble feeling any sympathy.

A Yukon is not a vehicle for anyone on a tight budget.

I have observed first hand more than a few times that a lot of people are ‘poor’ because they make fucking stupid life choices.

“What car would you take a 180-month loan to buy?”

None. Zero. Nichts. Nada.

Unless there was some sort of crazy economic circumstance (like a hyperinflation situation where it makes sense to hold assets instead of money), there is NO vehicle out there that I would buy with a 180 month loan because I am too smart to do something so stupid.

I don’t disagree with the meat here, but

In my experience, they are just not well educated. They come from financial ignorance and were never taught any better. And ignorance does not equal stupidity. I’d like to think they could be taught.

“In my experience, they are just not well educated.”

I would argue that someone who doesn’t think to take the time to educate themselves or ask for advice from someone more educated regarding a major purchase ARE idiots.

Whether someone has the intelligence but simply refuses to use it or whether they are truly dumb… the end result is the same… they are idiots.

Does it really matter why?

I recently helped a friend get a car. By “get a car”, I mean “gave advice I figured would go unheeded but didn’t mind because this person helped save me from heart disease and I was gratified to be asked”. What unfolded was less a matter of someone with one set of skills (her, an MD who oversees one floor of an award-winning hospital) ignoring those of another (me, a semi-retired guy who “knows about cars”) than a study in different perspectives and lifestyles.

She wanted a new mid-size SUV. I’ve never bought a new car and struggled to find anything commendable in that sector… the closest I could do was to express some enthusiasm for the then-new Lexus GX, tempered by wariness of its turbo V6. Eventually she ended up with a loaded Genesis GV70. Why? It struck her fancy and, most importantly, the monthly payments were a better fit for her budget than the competitors’.

“Bbbut the overall cost…” I said. That didn’t matter to her. It was the right number for her budget over the term she plans to own the car. I don’t think of the costs of car ownership in that way but it works for her. She’s not an idiot for viewing things in terms of monthly payments. She’s certainly not uneducated or bad with money. She’s not even negligent in ignoring the advice of someone who “knows more” about cars: I strongly advised against tricky-to-clean matte paint but she ordered it anyway. She has a detailer and happily gave him the gift basket of paint care products that came with the car and asked him to let her know when he needs more. She got exactly what she wanted and knew how to deal with it.

What might seem foolish from one perspective can be perfectly sound from another. Anchoring on a monthly number helps my friend focus on her job and enjoy her life. I think a lot of people with way less income are doing something similar: playing today’s losing game while they work for a better tomorrow.

To me, given she’s an MD, it sounds like a situation where she makes good money and has the money to burn.

And hey… if she can afford it, why not?

But not everyone has the money to burn… and that’s where people get into trouble.

Funny thing but if we believe “The Millionaire Next Door” people like MD’s are less likely to actually accumulate wealth because they spend their large paycheck on lifestyle creep.

I’d love to see some updated numbers as that book is rather dated.

If she was payment shopping she probably is an under-accumulator of wealth, to borrow a term from that (dated, but excellent) book.

We spend entirely too much time on ‘English’ in schools, and not enough on other subjects which will have greater effects on people’s lives than reading yet another Shakespeare play (or worse yet, the same one you read before).

What would I take a 15 year loan on? A home…. Oh you said a car hahaha yeah no.

Hit your local Walmart parking lot early in the morning and you’ll find it can be both.

Matt, thanks for including the “Wreck of the Edmund Fitzgerald”. As a lifelong Michigander, I still get the shivers and feels every time I listen to the ballad, just like this morning. I’ve had the privilege over the years to swim, fish, and kayak 4 of the 5 Great Lakes that border our state.

180 month car loan? Nope.

I attended a Gordon Lightfoot concert in Chicago’s beautiful Auditorium Theatre, not long after this song came out.

What car would you take a 180-month loan to buy?

Can i take Doc’s delorean and go do some time travel?

Need to pick up some stock from a weird guy and the Woz in a garage.

If you take a 15 year car note, that’s not a loan, that’s indentured servitude. And when that car costs more to fix than it’s worth, you’re going to stop making payments and let it get repossessed.

At that point, it’s the lender who is under water, sitting on a $10k note for a car that’s worth $2000 at auction. Sounds pretty unsustainable.

Meanwhile, the buyer has no car and is on the hook for $10,000 plus. And that’s unsustainable as well.

If such a loan product were to ever come into existence, I’d assume it would be because lenders did the math and figured they’d have already extracted enough profit via interest payments to write off the back-end losses by the time their collateral has depreciated to the point that borrowers are willing to walk away en masse.

The worrying thing to me is that this situation creates a world in which you never stop paying for a car loan. And I get it, some people WANT to make payments forever and will trade in as soon as their lease ends/car just gets a few years old. When I buy a car expensive enough to justify a loan, I’m thinking I’ll have 3-4 years of payments and then enjoy 5-6 years of paying nothing but insurance and maintenance. Is my 2018 sedan the newest, flashiest model? No, but I paid it off 2 years ago and have no foreseeable plans to get rid of it…

The 15, 20 or even 30 year vehicle loan already exists, it just has to have a kitchen, bathroom, and bedroom in the back of the vehicle. And there are many people who finance their RV’s for that long too.

When people make financial decisions based on monthly payment only, there will always be people out there to take advantage of that.

Boats, too. 20 year loans aren’t uncommon.

Just wondering if you could reference them as Nutlick and Doofus? If it fits, it fits.

I initially read Duffy as Daffy and then begin imagining Daffy Duck setting US transportation policy. It’s rabbit season!

Would you like to shoot him now or wait ’til you get home?

Daffy Duck is equally as qualified for the position as Sean Duffy, to be fair.

50-year home loans and 15-year auto loans (if they were a real thing) are both probably bad ideas. If the money was magically cheap, then sure, I guess nbd, but people are bad at budgeting and a lot of salespeople are predators; they aren’t going to take the monthly savings and save that money for retirement or future expenses they are going to use 15 or 50yr loans to buy more expensive shit. Over the last few years I heard multiple realtors use the phrase, “Marry the house, but date the rate” realtors have to eat too, and they aren’t all bad, but damn that is some bad advice. Similarly, I once asked what kind of financing terms I could get on a Winnebago converted Sprinter, and the rep said as long as I had 5% down they could usually provide 20-yr financing but he wouldn’t quote a range of rates.

I have yet to take out a car loan. As Sam Snead said, “aside from houses,if you have to buy it on time, you can’t afford it.”

I know I am lucky enough to be able to afford to do it so far, but that will probably end with my next car. The prices are nuts.

As for “The Wreck of the Edmund Fitzgerald,” a buddy used to go up to solo aciustic acts at bars and request that song because “I’m here with my buddy Edmund Fitzgerald, and he’s getting wrecked.”

In hindsight, this was in poor taste.

I lived by that mantra for a long time. However, I’ve started to buy nicer cars and finance them. The reasoning – the supply of cheap cars I used to buy evaporated – right after Cash for Clunkers. Next, finding a good beater started taking up too much time. Gone is the local rag that everyone listed their car on. Now you have to go to CL and FB marketplace, and it’s too easy for people to put up fake ads, ignore you, leave up ads for sold cars, etc. Also, you have to sort through the multitude of cars not worth $500 but people want $2500-5000 for.

Furthermore, I’m getting tired of working on cars just to keep them running so I can go to work. I’m a delivery driver, I need my car to work so I can work. Now I don’t mind working on a couple of project cars I have, but not having to do something to the car every month just to keep it running has been nice for the past 10 years. This last point has become even more relevant since parts prices have shot up.

Lastly – it’s actually cheaper. Hybrids have decreased my fuel expenses so much, it’s cheaper to operate my PHEV Escape, including it’s payment, than it is to drive one of my older cars. I had this experience about this time last year when my C-Max was totaled and I had to drive one of my other car to work for a month until I got my Escape. 50 mpg is a lot cheaper then 20 mpg when you’re driving 30k miles a year ($2800 in fuel costs alone,) and the minimal maintenance on a hybrid is really nice.

I truly cannot fathom loving any one car enough to devote 1/5 of my probable lifespan to paying for it.

yeah i keep a car about 2-4 years tops. and i never really spend more than about 7k on a car. I love the low end of the market, there is such good stuff there, and if it isnt working out.. well i can still just move on

Both my dad’s parents died right at about 50 so that is almost near 1/3 my possible life

I keep cars for 15 years, but I don’t want to pay for them that long. I keep them because they don’t have a monthly cost anymore (other than maintenance).

A 15-year car loan sounds plausible because the cost of goods and services keeps going up while the federal minimum wage has remained stagnant since 2009. That $7.25 minimum wage from ’09 is only worth $4.91 now, under the most charitable of estimates.

A house is the most expensive purchase most Americans will make, with a car being the second. If you remove home value from a household’s net value (what am I gonna do, sell my home and not buy a new one?) it will become crystal clear that most Americans are POOR. We’ve just allowed ourselves to become propagandized into thinking that because we “own” our homes that we are paying 15-30yr mortgages on, that means we are secure. We aren’t.

Cars are mandatory for most aspects of American life. Unless you live and work in one of about 30 major American cities, you need a car. Which, again, is the most expensive single purchase that a lot of people are ever going to make in their lives.

It is absolutely an affordability issue. It is a wage issue. We are more productive than we have ever been in history and if you remove an artificially inflated asset class from the equation, it is clear that our work is not commensurately rewarded.

Not quite. Very few people make minimum wage, and fewer make it now than they did in 2019. Legislated minimum wage has little to do with vehicle affordability, because most people make vastly more than the minimum wage. Which is to say, about 1% of workers make the minimum wage (it’s actually less than this, as individuals doing tipped work that don’t declare their tips, seasonal summer camp workers – yes, there’s a federal exemption for that – and the like have compensation that doesn’t show up in the income tax statements). 8 in 10, roughly, have compensation that is tipped or in-kind (see table 5 at the below link).

The percent of workers making minimum wage has gone down since 2019, indicating that the market continues to adjust for inflation even though legislation hasn’t.

https://www.bls.gov/opub/reports/minimum-wage/2023/

The point here is that legislated federal minimum wage is statistically irrelevant – about 0.2% of the working American populace make minimum wage after accounting for tips and in-kind contributions, most of whom work part time. What legislation requires and what people earn are two separate things; the median wage today is, inflation-adjusted, the same (IE, has the same purchasing power) as it was in 2019. Cite here: https://fred.stlouisfed.org/series/MEHOINUSA672N , though you can explore the Fed page for a lot more info.

IOW, wages have gone up. Minimum wage has nothing to do with vehicle affordability. We do have systemic issues with labor markets in the US, I’m not going to disagree with that, but fundamentally, the median 12-year-old car (which is, let’s say, 12k, or 2x the cost of a 2012 Toyota Corolla) could be purchased with two month’s wages of a median household.

We have a spending problem, not an affordability problem.

The only spending problem is that we don’t have enough money to spend. If very few people make minimum wage, there should be no problem raising it. $25/hr seems like a good spot to me.

How is it that (depending on your age) 2-4 generations ago a man used to be able to afford a house, a cabin next to a lake, a new car every 3-5 years, a college education, and 2.5 kids all on a single income? Plus he had a guaranteed pension.

Now 2 people working 40 hours a week can barely afford a used car without wondering if the next stock market “correction” will mean that they’ll be homeless, despite the fact that the only stock they own is in a modest 401k (if they’re even lucky enough to have that).

The cost of some things (houses, college, health care) have certainly exceeded inflation over the last few decades, but let’s not act like the typical middle class wage earner owned two houses and bought a new car every 3 years at any point in American history.

The past is sold to us and remembered through media, not the actual experience. The life you’re describing was that of an upper middle class salaried professional, one who can afford much of that same life today.

I lived in the past, you are incorrect.

My white trash Okie father dropped out of school in 8th grade and never went back. He dug ditches for a living. Zero investments. Zero stock market.

Yet we had nice new ranch style homes in California (the 1968 one had AC!) and the cabin at the lake for fishing complete with a little boat. Two Fords always in the driveway, dad’s pickup and moms full sizers. (66′ Galaxie 7 litre was my fav, but the 57′ Fairlane was runner up)

Everyone in my parents social circle was the same story. Only dad worked, no one has much edumacayshun, blue collar, all were doing fine financially.

Even my crazy “poor” aunt and uncle, he had never gone to school, had a damned house at Morro Bay in sight of the ocean in addition to their place in the central valley.

And he drove a sweet sweet brown Caddy he paid cash for.

Things have gone wrong in the last 60 years for ordinary people. Lots of things. But don’t say that there once wasn’t a golden era for the common folk. From 1945 to about 1975 was amazing.

All I will say to this is that every statistical measurement we have tells us that your family’s experience was an outlier. That doesn’t mean it didn’t happen, but most blue collar families in the 50s and 60s did not have multiple new cars and multiple homes.

Was it CA who most recently raised minimum wage in the food industry? What has been the fallout of that action? I mean that honestly, I haven’t paid attention, but it seems like a useful case study for impacts of wage control at the government level.

I think the trouble with raising the minimum wage like that is that those few people currently making minimum wage would instead become unemployed…

In my opinion, minimum wage laws remove a powerful way for lower skill (and maybe also lower responsibility, for whatever reason) workers to find jobs. If I can only do low-quality, low-skill work, and I struggle with personal issues that make me miss work 20% of the time, nobody will hire me for $25/hr. However, if I could give a low bid of $5/hr, I’d probably have no problem getting a job! It wouldn’t be much of a living wage, but it beats unemployment all day, and gives me opportunities to build skills and develop responsibility.

I have met a lot of people with very low abilities and intellect and they do not have the ability to “build skills”. They are employed at the best job they can actually do and they deserve to earn enough to not be on government assistance.

The trouble is that the corollary to that is that someone is then obligated to pay them enough to not be on government assistance. If the work they provide my business doesn’t provide me more value than what I’m paying them, it’s going to be a hard sell for me to continue employing them. The options are either 1. I’m a nice guy, and have a profitable enough business that I can afford taking the loss on them, or 2. I fire them. Option 2 is going to be what happens 99% of the time.

The only real way out of that is for the government to come to my specific business and legally require me to hire this specific individual at the higher minimum wage, but I really, really don’t think the government has the right to force me to do that, there’d be all kinds of unintended consequences, and the logistics of it would be nightmarish.

I know what you’re saying, and I agree that it’s a problem, but I just can’t think of any possible solution that doesn’t make even bigger problems of its own.

Yes. I think it is what kind of business. Giant super profitable for shareholder corporations and small mom and pop businesses can and should be thought of differently. Walmart and McDonalds should not have employees of government assistance.

Walmart is not super profitable. They have averaged less than a 3% net profit margin for the last decade. Today a basically guaranteed 1 month Treasury will pay you 4%

And the worst part is that while they predatory price all of their competition out of business and don’t pay their employees enough to live on, we get to pick up the tab with government assistance. We’re subsidizing Walmart’s race to the bottom with our tax dollars.

Huh, that’s something I hadn’t thought about. So the idea is that government assistance to low earners artificially drives down wages, because it relieves the pressure on businesses to pay their workers enough to live on unassisted? Or alternately the pressure on workers to demand high enough wages to live on unassisted?

The other issue is, if you put additional pressure on those businesses to raise wages, then you are incentivizing them to find alternatives. Paying $15/hr may be a decent way for people at the bottom of the pay scale to make some money. Raise that to $25/hr then there is a reason to invest in automation, robotics etc.

Of course this is already happening. You saw that with the most recent push to raise everyone to $15/hr and McDonald’s installed self-serve kiosks to experiment with removing cashiers.

I honestly don’t know what the answer is (I mean, I could come up with some great ideas that have zero chance of becoming reality, but why waste our time?) but we are getting to a point where it will be harder and harder for those that have no marketable skills to earn a living unless something changes. And I think it has to change culturally from the ground up.

Amazon is a good example. Back in 2018 they set a minimum wage of $15 per hour. Today they pay up to about $25 per hour and provide health insurance.

A few weeks ago internal memos leaked that say Amazon will replace 75% of their employees with automation by 2033 and the have already started rolling out highly automated warehouses with very few unskilled jobs. That is with 2025 technology

Amazon is the 2nd largest largest employer in the USA with 1.2 million workers – most of which are blue collar jobs.

The problem is you cannot think of them differently, because they are competing for the same workers. If Walmart is offering $18/hr then the mom & pop store has to offer the same or more, or risk not being able to get staffed sufficiently. Lots of people think big corporations are the safe bet and will go there first.

There are already federal and some state regulations that differentiate wages based on company size. Fair Labor Standards Act (FLSA): Sets federal minimum wage, overtime pay, and child labor standards. It generally applies to businesses with at least $500,000 in annual sales.

How does that help?

If you were at teenager looking for a job, would you take the job for $18 an hour at the Walmart in town or $15 an hour at Dave’s Corner Store? If Dave wants any decent employees he’s going to have to offer $18.

Welcome to complicated. Maybe walmart is too far out of town for some or not hiring. Maybe dave will need to treat his employees with respect or dave’s place sucks less than working at walmart. Government regulations are complicated and need to draw lines somewhere and there are always situations where that line is not great. a decent employee is not always the one who will jump jobs for a dollar. Life is messy. It is better than everyone gets paid 1 cent/hour and can’t complain.

Quite honestly Dave probably treats his employees exponentially better than Walmart does but that doesn’t pay the bills. Welcome to complicated, I deal in it every day.

The flaw in this argument is that there is someone better who will take the job at the same wage. Which often cases is not true in this lower sectors. Look at the current state of the RV industry. They deal with low quality work, because they pay low quality wages to a low quality labor pool.

Yeah, I guess as a business owner the challenge is to figure out what the best point on the price-quality curve is for the people you want to hire. Are you better off hiring lots of low-wage workers who don’t work very efficiently, or fewer high-wage workers who are more productive?

I think what I was trying to say was that if we artificially increase the price of the less efficient workers, there will be no financial reason to hire them over the more efficient workers.

Are you saying that even in that situation, you wouldn’t be able to hire the (normally) higher-paid, higher-productivity workers (because the labor pool is too small), and so you would instead keep the lower-productivity workers and just pay them more to keep up with the increased minimum wage? I can see how that could be the reality in certain situations, but I also imagine your business would have to be seriously profitable to be able to survive eating the large wage increase without any increased productivity

That might have been true for a small subset, but certainly not the norm. Both sets of my grandparents were squarely middle class, with one grandpa being a mechanic, and the other being an accountant. Both my grandmas also had jobs at various points to help make ends meet.

Yes, each was able to provide for their family with a typical middle-class American house from the 1960s, two cars, and they helped pay some towards college, but certainly couldn’t afford to pay for everything. They kept their cars for a very long time, often working on them themselves to save money. Airfare was still far too expensive for an average family vacation, so they took road trips.

Were they comfortable? Absolutely. They would both say they lived the American dream, but they still had to work really hard and make sacrifices to achieve that, same as today. I’d say the big exception would be housing costs being a much lower overall percentage of income than today, but don’t forget interest rates today are still pretty low compared to about 7.3% in 1970, spiking to 11.20% in 1979. My parents had a 9% mortgage on their first house in the ’80s.

Also, don’t forget the increasingly large list of things we pay for without thinking about it, that wasn’t even a thing 2 generations ago:

Mobile phones and data plans, especially for the kids (I do note that home telephone and especially long distance calls were a lot more expensive though).Internet connectivity at homeAir Conditioning (I grew up in a house in the suburbs of Atlanta without it)Multiple cars; many many families made do with one car and it wasn’t until both parents worked that two cars became the norm, though it was not uncommon for two car families.Various app subscriptions, food delivery etcNetflix et al; I didn’t even have cable TV in my house until about 6th grade.Dining out: This was extremely rare a few generations back and only happened on special occasions, including fast food.There should be a lot of things on the list we could remove if we’re strapped for cash. I get it, we don’t have a lot of resistance to advertising/marketing in our culture and everyone is trying to keep up with that one family that is doing better than everyone else (or are they?).

We’ve surpassed the expectation of comfort and now everyone has to have everything for fear of missing out. I think we need a reset on some of these things but I don’t think I know how to put the toothpaste back in the tube.

Yep, all good points as well. Even as a Millennial, I remember when we first got dial-up internet, and we didn’t have cable for most of my childhood, and even then, just the bare minimum local channels once we moved to a house that had terrible over the air reception. We had AC that came with the house, but my parents refused to use it (still don’t very much).

“That might have been true for a small subset, but certainly not the norm. Both sets of my grandparents were squarely middle class, with one grandpa being a mechanic, and the other being an accountant. Both my grandmas also had jobs at various points to help make ends meet.”

+1

It seems when many talk about past generations, they seem to have selective amnesia.

When I was growing up, my parents did it mostly on my Dad’s income. But like your grandma, my mother also took the odd side job.

Also the way my parents did it was that while we had a house, we didn’t have things like expensive electronics, fancy cars (just one used sedan for the whole family every few years after the old one wore out), central AC and a lot of other amenities people these days can’t seem to live without.

And to save more money, we rarely ate out, my mother would make some of our clothes and our vacations were mostly family camping trips.

Hell, my family didn’t have things like a VCR until I bought one with the money I made at my part time job.

“Were they comfortable? Absolutely. “

In my case, I recall there being times where my mother would say that she wasn’t sure how they were going to pay all the bills.

There were definitely times where my parents were NOT financially comfortable.

If you raise the minimum wage to $25 then anybody currently making $25 will obviously want $30. Do you really think that people who’ve been at a job for a while will be okay with suddenly making the same wage as someone hired that day?

Illinois’ minimum went from $10 to $15 in the space of five years. You increase a business’ single biggest expense by 50% over 60 months and you don’t know why prices have gone up?

That’s my point. Practically everyone is underpaid, even the people making $25/hr right now. The people that think they are secure because their house is “worth” 500k+ will be in the same breadlines as everyone else if/when the market collapses. 40% of the gdp growth and 80% of the stock market gains this year are due to AI, a product nobody asked for with an incestuous supply and manufacturing chain.

We all know that infinite growth is unsustainable and that true opportunity is exceedingly rare, so we are inclined to focus on next quarter, or make big bets on meme stocks and meme coins, all on the hopes that some greater fool will be left holding the bag. It is a naked grift.

Tl;dr – If labor was actually fairly compensated, businesses would have more consumers that they can produce for.

If a person working at Burger King is worth $25 an hour, not only will your value meal be $30 but then a barber is worth $50, a skilled welder is worth $100 and a doctor is worth $500. Keep doing that and the prices go up because there is not obscene markup baked into everything you buy. If there were, then that’s an opportunity for a competitor to move into that space.

Raise the cost of wages and people’s buying power will increase for a short time until prices adjust, and then there will be another call for wages to increase. This has been true since the history of ever, or at least as I’ve observed in my lifetime.

My local plumbing company already charges $125/hr for labor. I don’t even think you could get a backyard, shadetree welder with a harbor freight flux core to stitch together two pieces of scrap steel for under $100/hr. And the last time I got a haircut it was $40. And I’m fine with that, because these people deserve a living wage.

CEOs don’t need to earn 285x the typical worker. Boo hoo, they might have to go down to 100x, or even 50x. Odds are, almost everyone here is working class. Let’s try to have a little solidarity here.

I’m using out-of-thin-air numbers. If your plumbing company is charging you $125 an hour I assure you there’s not zero markup in that.

I’m working class too my friend, and I employ around 40 people at my business. I want my people to be financially comfortable and feel satisfied at their job. But my labor costs skyrocketed at almost the worst possible time.

I’m feeling the crunch just like anyone else, with everything we’re responsible for, our margins are being squeezed every single day, often by national-level competitors that have much deeper pockets than us.

I’m all about solidarity but let’s take your example to an extreme. Let’s make minimum wage $200 an hour. What do you think is going to happen? Will everyone be suddenly wealthy or is the market going to adjust?

Far to much time is focused on executive pay. Yes, I get it, their pay is ridiculous which justifies the moral outrage. However, from an accounting standpoint their pay is a rounding error on the company’s expenses.

You can cut the entire GM C-suite’s pay to $0 and you would not save enough money to give even just the UAW workers a $1 per hour raise.

So while cutting CEO pay might make the typical worker feel better – it won’t actually raise the rank and file’s pay.

What actually could effect pay is talking societal issues like US health care costs. My employer pays $22,000 a year for my high deductible insurance plan. That is $11 per hour for insurance that doesn’t really pay for anything until I pay $5,000 out of pocket.

Healthcare, like housing, food, and water, should be basic rights afforded to all humans. The focus of industry should not be on juicing the earnings report for next quarter so the stock price goes up. It is a toxic mindset that only benefits a minuscule percentage of people and is fundamentally unsustainable.

$1/hr might not sound like a lot, but I’d prefer that every worker get an extra buck over funneling all of those dollars to one dude.

Industry’s focus is making money – it has been since the beginning of time and will be until the end of time.

If you want to lay out a minimum standard of living for every person that is the role of society through government not industry.*

GM’s C-Suite is 14 executives not just Mary Barra.

(* I agree that healthcare, housing, food, and water are basic human rights.)

So, this is true in a vacuum. But, IRL the effects on inflation via labor cost are pretty minor. Take Denmark for example. A McDonalds employee is paid well into the 20’s per hour with benefits. However their meal cost is slightly lower than the US. Because the lowest wages have stagnated far below inflation you’d be bringing those lower class back to where they were then propelling them forward.

That was never a thing. Like… ever.

You want to wind the clock back 2-4 generations? Then let’s go ahead and remove air conditioning from the equation. Cut the size of your house in half, because the average house size back then was 1500sf. Want to share a bathroom with your kids? That’ll be a thing, as the median home had 1.5 baths back then. My grandmother (and I’m 40!) tells stories of when her home in Wyoming got electricity. Outdoor plumbing was still a thing. You’d call people on a party line, so if somebody else in town was on the phone, you couldn’t use it. You’d get your news on the radio until Philo Farnsworth brings the TV into commercial capacity.

International travel? Vastly more expensive. Your vacation will likely involve a road trip somewhere, once a year. You will likely never see another country unless you are in the armed forces.

I am not sure where you get your news from, but it has done you an awful disservice about what reality was like.

Meanwhile, $25 minimum wage is merely going to put some people out of work. The minimum wage – and I’ll engage in a trope here – is always $0. You will make it far more expensive for teenagers to get work experience.

California mandated its own minimum wage for fast food. The net result was a reduction in employment.

https://www.nrn.com/quick-service/california-lost-16-000-restaurant-jobs-since-20-minimum-wage-was-signed-into-law

(I’ve avoided any of the libertarian think tanks, which have an even more aggressive assessment, because hours were often cut from employees that did remain).

Not sure making people unemployed is a desirable outcome here, but if you want to argue that you wish to put an additional 3-5% of people in a particular industry out of work to hike the minimum wage, you are… welcome to it.

My dad could afford a decent house in a newer neighborhood and a 4 kids and a new car in the 1960-70 on just a tile and carpet installers income. yes houses, cars were also cheaper.

This. My family, 5 kids, managed to build a really nice 3 bath, 5 bedroom home in 1970 for about 40K on a wooded 1 acre beautiful lot. I just looked this home up, and it’s over 3,500 sq feet. Cost in 1970 was about 50K all in. Last time the home sold it was near 700K…

We were far from wealthy also. And my Mom did not work.

Thankfully my Dad made enough as a stock broker to allow that we could join a very nice country club so we had a safe place to hang out and swim each summer. I recall the fees and cost for meals there averaged about 4-5 hundred a month.

It was a different world then for sure.

Stock broker and blue collar worker aren’t exactly the same income level.

you may be surprised.

a lot of brokers then worked on commission only.

if a client did not call, that day you made nothing. really.

but in all honesty there were years he made over a million, and years he barely clear 20K…so it does actually sort of compare.

So he averaged between 3x and 166x the average wage in 1970. Somehow I don’t think that really compares to a blue collar worker back then, as evidenced by the country club membership.

My grandparents (born in the 1920s and 30s) both raised families of 6 in small (~1500 ft^2) homes. My mom’s dad was a minister and later a church administrator. My dad’s parents owned a dry cleaning business they took over from my great grandfather when his alcoholism no longer allowed him to operate it. They had one car at a time, which was certainly not replaced every three years. My grandmothers both worked once the kids were old enough to watch themselves. They never went out to eat, they travelled very rarely, they lived a modest midcentury life. They would never have considered themselves poor, because they saw real poverty in the Depression. But by today’s standards, they were indisputably working class.

Your nostalgia glasses are so rose tinted they’ve gone dark and you can’t see history for what it really was. People live better, more comfortable lives now than at any point in human history. Average homes are larger with more amenities, we live longer, spend less time on sustaining life/chores and more on entertainment/hobbies, cars are more reliable, etc. It’s this “golden age” fallacy that leads to people like Trump getting elected and policies that attempt to take us back to a worse time in human (and USA) history.

Average homes are larger because it costs fractionally more to build them that way, with the return on investment being significantly more so. Couple that with homeowners not wanting their houses to be worth less because it is literally the only asset that gives them a positive net worth, and you have two obvious incentives for inflating home sizes and artificially restricting the market.

The orange guy taps into legitimate grievances and capitalizes on the fact that Americans are too overworked, overstressed, propagandized, and disengaged. People are insecure and living hand to mouth. They don’t have the resources or the community to think beyond the easiest, most reactionary response. It is a crisis that is deliberately manufactured because stressed out people are easier to manipulate.

There are certainly legitimate grievances but buying into the narrative that life was better 2-4 generations ago is exactly the propaganda they want you to believe. My great-grandpa’s first wife died in a house fire in 1923 because she mistakenly put gasoline in a kerosene lamp. Living in 2025 is undeniably better than living in 1925 or 1950 or 1975.

People are dying today because they can’t pay their electric bill so they use propane heaters indoors. I don’t quite get your point here.

Obviously that’s unfortunate and we should strive to eliminate all preventable deaths. My point is that more people used to die 2-4 generations ago from things like lack of heat, clean water, healthcare, etc and looking back fondly on those days and believing false narratives about how life was prevents meaningful discussions about how to address present day issues.

I don’t see where I advocated for a lower standard of living or how anything I said could be interpreted that way. I am arguing for an increased standard based on higher wages, increased availability of social services for the people who rely on them, and an economy structured around the needs of the many rather than the whims of the few. 70,000 homeless people in LA alone indicate that there are still massive problems with access to everything you pointed out. You lift people out of poverty when you stop paying poverty wages.

What I am saying is that our purchasing power has not scaled with our productivity, and just because grandpappy didn’t have an iPhone 17 and you do doesn’t mean that we are better off in every regard. Homes being bigger and more expensive than ever isn’t making the point you think it is to the growing numbers of people who are increasingly feeling like the American dream is just that, a dream.

Sorry but that myth really needs to die.

The average household in the USA has never lived like that. Sure a highly paid auto worker or steel worker with a union contract might – but the typical worker never made that kind of money.

Even way back in 1950 65% of prime age adults were working.

“How is it that (depending on your age) 2-4 generations ago a man used to be able to afford a house, a cabin next to a lake, a new car every 3-5 years, a college education, and 2.5 kids all on a single income? Plus he had a guaranteed pension.”

The devil is in the details.

My dad was that man. He was a machinist and was a member of the steelworkers union.

He was able to afford a house. But that house was much smaller and didn’t have the amenities most home buyers expect these days.

For example, the house I grew up in didn’t have central AC, I shared a bedroom with one of my siblings until my oldest sibling moved out and we only had one car for the whole family. And we didn’t have things like dishwashers, nice stereos, VCRs and microwave ovens. We had a washer and dryer… but to save money on electricity, my mom would dry our clothes on the clothes line most of the time.

He also had a car… one car for the whole family of 6. And it was a car that was much more basic than the cars of today. Typically he had Fords… but also had the odd air-cooled VW.

And my dad did have a ‘cottage’. But it wasn’t like the cottages you see today. My dad bought an unserviced lot cheap that was next to a lake.

Weekends were spent ‘working on the cottage’.

He built the ‘cottage’ himself… a cottage most people today would call a ‘shack’.

And there was no running water. You went to an outhouse to go to the bathroom and when you wanted to ‘bathe’, you went for a swim.

And electricity at the cottage-shack? LOL… yeah right.

As for other things… we rarely at out at restaurants and vacations were mostly family camping trips.

The standards of people today are MUCH HIGHER than people of my parent’s generation and earlier.

And that accounts for a lot of the difference.

“Now 2 people working 40 hours a week can barely afford a used car “

The problem is the used “car” people go for these days are overpriced luxury SUVs and oversized trucks… expensive things that only the wealthiest from past generations would have bought.

well said but I would say the number of cities with decent transportation to not need a car is <10.

“What car would you take a 180-month loan to buy?”

ALL of them assuming the negative signs I slyly ink in front of the interest rates while the finance guy isn’t looking become legally binding.

I’m convinced all this sub prime car business was happening before from the buy here pay here most just never got picked up. Now people have less excuse then ever to make bad decisions because research is free and easy. But they try to get sympathy and even money from making their bad decisions public. I’m sure it will be “chat gbt” told me it was a good deal soon if it hasn’t already happened.

What car would you take a 180-month loan to buy?

A car with the winning $900 million Mega Million ticket wedged in the rear seat cushion.

IMHO the issue with cars is not an affordability issue, it’s a consumption issue. Consumers consistently pass up affordable options so manufacturers focus on whatbthey are buying. And that’s their choice as Consumers. Housing is mostly a supply issue (similar to autos during covid).

And a longer loan is not the answer to the housing issue. Just a lazy way for boomers to feel ok not addressing the issue.

The Wreck Of The Edmund Fitzgerald is such a great song, and the fact that the Edmund Fitzgerald has taken on new life as a meme is hilarious and awesome. I love history and I love shitposting, so when they intersect it tickles me in all the right ways. It reminds me of the boys in Rome vs girls in Rome stuff that went viral a couple of years ago after the “ask your boyfriend/husband how often he thinks about the fall of the Roman Empire” meme before it.

It’s also a testament to how much a great song can carry a meme to stardom. Rick Rolling isn’t all that all that unique or funny but Never Gonna Give You Up? An absolute banger. 10/10 song. The Shooting Stars memes? Pretty funny on their own, but the song? Excellent. It just adds another layer to the whole experience.

Anyway 15 year car loans or 50 year mortgages? Of course the Trump admin is into these ideas, it’s just another way to destroy the working class and implement trickle up economics. The 1% will profit and regular people will suffer, which is always the endgame. The goal is techno feudalism and in their ideal world none of us would own anything and would have to rent every single aspect of our lives from tech oligarchs.

It’s a naked scam. But so much of our country is so hopelessly financially illiterate that it just may work, and people dying in debt is great for the billionaire class because they’ve been collecting interest the whole time, and they’ll get to continue collecting it when they go after the person’s family for what’s still owed. They want all of us dumb, unhealthy, totally controlled, and constantly giving them more and more of our finite resources because they’re antisocial freaks who can literally never have enough to be satisfied.

Wait what are we on about again? Don’t fucking shop by monthly payment ever. That’s what they want you to do, and they very, very openly despise you and wouldn’t piss on you if you were on fire. They’d certainly try to grab your wallet out of your back pocket as you’re ablaze though, because it would increase their $10,000,000,000 net worth to $10,000,000,020.

I guess people never learn the easy lesson: DO NOT PUT CRIMES IN WRITING. You’d think that would be easy.

Okay, I’ll do a damn lot count! I’m workin’ with ya on this thing here!

I still need to get my wife to watch that movie.

The only way I could do a long term for a car, having GAP and a reliable vehicle. But I hate the idea of having a car payment that long. I would rather have a short loan and start putting money aside (same monthly “payment”) for the next purchase.

Arthur Guinness leased his first brewery at £45 per year for 9,000 years.

https://en.wikipedia.org/wiki/Guinness_Brewery

So can I get a 108,000 month loan on my new King Ranch?

So In 10759 that space will be available for lease? Can I rezone if for residential?

I’d find the smell of 9000 years of Guinness brewing to be a major selling point.

As always, when money is cheaper to borrow than the rate of return, it’s at least worth considering making the loan as long as possible to preserve flexibility (obviously there are other considerations involved, I am not a CPA or financial advisor).

I don’t expect automakers to be handing out 15 year 1.9% loans any time soon, but the point is broadly applicable to 4 vs 7 year loans or similar for example.

All the “bootstraps” mockery aside, the right answer here is to avoid taking out subprime loans for late-model cars.

The average car on the road is 12 years old. Tricolor’s average loan balance (which is not the same as the sum of payments, which would be higher) was $21,000. A 2012 Corolla near me? $6,000.

I’d have a lot more sympathy for anyone involved with the subprime market if anyone was sympathetic, but I’m not about to feel bad for a borrower who’s purchasing more car than I have and I’m not going to feel bad for a lender who extends a loan knowing it’s a bad idea for the borrower.

I’ve found repeatedly in my life that there is a “normie” consensus that a car under $10-$15K is a garbage heap. I find SO MANY people who are convinced they HAVE to spend those amounts absolute minimum to get a decent car. I’m not advocating eveyone be willing to buy that nonsense garbage I choose, though I have gotten good at choosing decent ones. But with a little extra effort, solid cars are plenty available at much more reasonable costs.

“I’ve found repeatedly in my life that there is a “normie” consensus that a car under $10-$15K is a garbage heap.”

What that tells me is a lot of ‘normies’ are stupid, don’t do their homework and make poor life decisions that keep them poor.

” But with a little extra effort, solid cars are plenty available at much more reasonable costs.”

+1

But that’s the problem… a lot of ‘normies’ don’t want to put in ‘a little extra effort’.

I think “a little extra effort” is hard if you don’t know who to trust. It will seem obvious here, but go into a math dept and finding the normal subgroup of a general linear group will be obvious. We tend to think the things we know are both more important, and more obvious than they actually are. Couple that with marketing pressures and businesses that depend on people not knowing things and I at least have empathy for those who get had.

When in doubt, or when in debt, the beige Corolla is your best bet!

As in, most people just need reliable A to B transportation. Investing your ego in a car is a luxury purchase – which is fine, because we live in a world where people want to invest their egos in their music, their headphones, their Insta profiles, and a whole heap of other things – but it is an outright luxury.

If you’re drowning in debt or have a sub-600 credit score, the $6-8000 Toyota Corolla or Yaris or Echo is the answer. The automotive equivalent of plain oatmeal? Yes. Reliable enough for everybody (including my doctor/exgf, who can definitely afford better)? Also, yes!

One that comes with a 180-month warranty.

I still have the lifetime bumper to bumper on my jeep and I have had it for 160 months.

I hope you’re milking that warranty to the max. I know I would…

it is a jeep wrangler I am using the hell out of the warranty

Of the few new cars I have owned I have driven for over 12+ years and driven them into the ground. I do not tend to sell any car wile there is much equity in the thing. I am getting close to the point where I may get one more new car and it had better last 20+ years so a 15 year loan on something I may keep 20-25 years and potentially die before it is paid off, maybe?

Extending loan terms does nothing but slap a bandaid on a war wound. And the banks are more than happy to provide a steady supply of Bandaids at a price…

If there is actual effort at the gov level to fix things, we’d be talking more seriously about how to teach folks good financial principles, and bring cost of living and wages under control (which I acknowledge is NOT an easy thing to do) vs encouraging a nice fat handout to banks that are keen to take advantage of financial illiteracy. Very few people in DC seem to actually care unless it’s a campaign item, because none of what I mentioned above is financially incentivized.

I thought the 15-year loan already existed, at least for exotic and collector cars, so the clear answer is a certain Pontiac on Cars And Bids.