Mark Twain once said that a lie can travel halfway around the world while the truth is still pulling on its boots. That was back when social media was what you heard in a tavern. It’s only gotten worse since, and recently, there’s been a freakout over the 15-year car loan. This doesn’t seem to be real, but it’s also not far from reality, which makes the response interesting.

The Morning Dump is wading into affordability, because that seems to be the most pressing issue for the automotive industry. This, and the potential for a 50-year home loan, has created the rumor of a car loan that could stretch to 180 months.

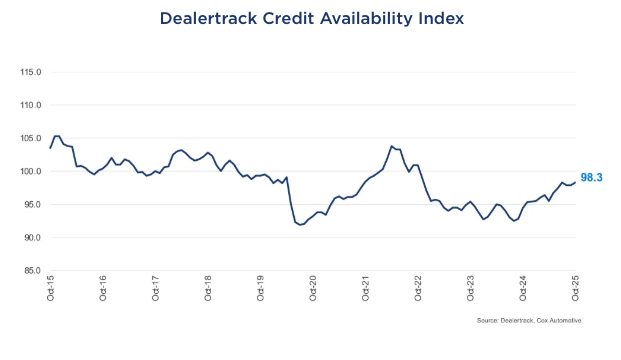

Taking a look at the overall credit market for cars, things are loosening up a little, and car loans themselves are already getting much longer. This isn’t to say all is well in the world of auto financing, as a deep dive into the failure of Tricolor shows how much fraud there potentially is in the system.

As the First Brands (they make all sorts of car parts) bankruptcy demonstrates, getting $10,000 for a car loan might be hard, but getting $100,000,000 for your company on the back of allegedly double-counted invoices is easier than you might guess.

The 15-Year Car Loan Isn’t Real

I woke up this morning and saw that the Autopian Discord (open to everyone) was excited about something. That something had been deleted, but I was able to infer and confirm that it was a rumor about the White House proposing a 15-year car loan. Specifically, there was an image going around in the White House Comms-style saying one was coming, and that Secretaries Lutnick and Duffy were working on it.

This sounded wrong for many reasons, and the post was deleted from Discord after everyone realized it was probably just some social media nonsense. I won’t link to the original because that merely reinforces the problem, but it went viral on both X and BlueSky. There’s a good fact check over on Yahoo! News, and it points out that there’s no version of the fake release on any White House-related accounts.

What tipped me off that it was probably fake was the mention of Secretary of Transportation Sean Duffy. As the old saying goes, the most dangerous place in the world is between Secretary Duffy and a camera, and he hasn’t been out there promoting this.

I think what really made this believable was that President Trump is attempting to address the housing crisis by promoting the 50-year mortgage. The idea there is to potentially lower monthly payments by stretching out the loans. Realtor.com points out one of the reasons why this might not be ideal for homebuyers, and the logic is similar to why it’s not great for people trying to finance a car:

Assuming for the sake of argument that mortgage rates were equal across both products, a 50-year mortgage would lower mortgage payments by about $250 per month on a $400,000 home, assuming 10% down and a 6.25% mortgage rate.

Total interest payments over the life of the 50-year loan would amount to $816,396, compared to $438,156 on the 30-year loan, a difference of $378,240. That amounts to 86% more interest over the life of the loan.

“Buyers do benefit from spreading out the high cost of a home purchase over a longer period, but lenders certainly benefit, too, by having a longer period to charge higher interest rates,” says Berner.

A key difference here is that the main cause of housing costs is a shortage of supply, which this doesn’t address. There’s a way to look at it where the most obvious outcome is that the addition of more buyers without more supply means higher prices. Cars don’t quite have this issue. While there’s some shortage of affordable models, carmakers can more easily turn up production of cars than homebuilders can turn up the supply of affordable housing.

However, homes tend to appreciate in value, whereas cars do exactly the opposite. The bit about interest rates is essentially the same as homes, and that’s worse because cars depreciate so quickly. Doing the math: if someone bought the average car (about $50,000) with the average down payment (about $7,500) at a better-than-average interest rate (7.00%), that person would only have a monthly payment of $382. However, that person would pay $26,261 in interest, making the total payment for the car $76,261 over 15 years. Additionally, the buyer would likely be underwater on the loan for a long period of time.

For all these reasons, a 15-year car loan probably isn’t going to be a White House priority, although there are times when it seems impossible to know these days.

The 15-Year Car Loan Isn’t As Crazy As It Sounds

Car loans are getting longer, with or without White House intervention, and buyers are increasingly underwater. The 84-month loan isn’t that unusual, and, with a slowdown in car buying, lenders are doing more to give access to buyers with lower credit scores.

According to Cox Automotive, the approval rate for auto loans in October hit 72.6%, which is down from September but up from last October. The one area of the market that expanded was subprime lending, with way longer terms being offered to buyers. The latest analysis shows that the share of loans over 72 months is 27.5%, up 300 basis points from last October.

Buyers tend to think in terms of car payments and not the overall market picture, but with rates dropping, these borrowers are not getting the best deal, as Cox points out:

The improvement was driven primarily by lenders’ increased willingness to extend credit to subprime borrowers through longer terms and lower down payments, even as overall approval rates declined. However, this expanded access came with higher yield spreads, meaning consumers paid more for financing compared to prevailing market rates.

Once again, money isn’t everything, but not having it is, especially for subprime borrowers. The longer the loan term, the higher the interest that a lender is going to provide, meaning that as rates go down, borrowers are paying even more for their money.

Tricolor Disaster Shows The Difficulties Facing Subprime Borrowers

The saga of subprime used car retailer Tricolor has revealed a lot about the underwriting practices of large institutional lenders like JPMorgan Chase, but it’s also shown how hard it is to be a subprime borrower.

There’s a great piece from Bloomberg that gets into the chain of events that led to the collapse of Tricolor, which allegedly borrowed money by using the same loans as collateral with multiple lenders. The company’s history is interesting to say the least, but what really got me is how much harder the company was on its borrowers than its lenders seem to have been on Tricolor:

Customers described aggressive sales tactics, confusion over loan documents and long delays in receiving car titles. Some said Tricolor called repeatedly when payments were late, often numerous times a day and deep into the night. Many vehicles were worn out, poorly maintained and had high mileage, according to car buyers and former employees.

Raquel Ramirez says her used GMC Yukon SUV has done nothing but give her trouble since she bought it in 2023 — it constantly jerks when she drives even after repeated repairs — and yet Tricolor staff would hound her when she fell behind on the $35,000 loan she took out. “If I missed a day of a payment, they would call until 10 at night asking for the payment,” Ramirez says.

The lack of scrutiny for massive companies isn’t just an issue with Tricolor. It’s also a key issue in the failure of First Brands.

First Brands Group’s New CEO Admits Company Faked Invoices To Get Loans

First Brands Group, the parent company of brands like Fram and Trico, declared bankruptcy in September after it was discovered that the company had massive debts it wasn’t likely to be able to pay. It was later revealed that the company’s founder, Patrick James, allegedly funneled hundreds of millions of dollars to his own personal accounts.

The company’s new interim CEO, Charles Moore, told the judge handling the bankruptcy that he discovered massive fraud at the company as soon as he arrived.

First Brands lawyers showed a 2022 message from one member of the company’s finance department to another, in which an employee suggests they may have to make “dummy invoices” to secure additional financing. In a subsequent message, a top member of the finance department doesn’t express any concerns about falsifying invoices, Moore testified. That surprised Moore, he said.

“I would think that if the notion of creating a dummy invoice was new or not happening, there would be some reaction to that,” Moore said on the witness stand.

Did you catch that? The new CEO was surprised to find out that the company’s finance department was not surprised to be asked to allegedly commit fraud in order to borrow money.

What I’m Listening To While Writing TMD

Brian kindly took over TMD yesterday, meaning that I missed the opportunity to mark the 50th anniversary of the wreck of the SS Edmund Fitzgerald by playing the eponymous song from Gordon Lightfoot. Today, I fix that.

The Big Question

What car would you take a 180-month loan to buy?

Top photo: Stellantis

The 84-month car loan may not be unusual these days, but it is absolutely insane and wrong on so many levels. If you need 84 months to pay off that ride, it’s a ride you should not be buying, you can’t afford it. But cars are so much more expensive now. True. Doesn’t change the fact that if you cannot afford one, you should not be getting it, period. 48-month loan is what I’d consider absolutely maximum reasonable time to keep up with its depreciation. If that means getting a Sentra instead of a Suburban, that’s your reality. Stop posing for the Joneses.

I’m afraid we’re no where near the point where reality eclipses FOMO.

Car are cheaper today comparing like to like after adjusting for inflation or wages. It takes the median household quite a few less weeks of pay to buy a Camry or Corolla today than 30 years ago.

The problem with the auto market is people are steadily moving up market to more expensive cars enabled by longer payment terms. People buy a RAV4 instead of that Corolla.

Yes, cars are cheaper dollar for inflation adjusted dollar. Back in 2000 I bought a fully loaded JGC for 38k which works out to ~72k in todays money, which is actually a bit more more than a fully loaded one today Problem is that I am not (nor are most) making anywhere near twice as much money as I did 25 years ago. So while cars’ prices may be OK inflation-wise, affordability is down in the toilet.

The median US household is making more today than in 2000 – even after adjusting for inflation. In 2000 the median household was making $72K in 2024 dollars. In 2024 the median household was making $84K.

SOME households don’t have wages keeping up with inflation but most have.

We can also look at affordability based on median household income vs MRSP

Base MSRP

1995 Camry Coupe: $ 16,128

2007 Camry Sedan: $ 19,900

2024 Camry Sedan: $ 26,420

1995 median income $34,080 (Camry = 25 weeks of income)

2007 median income $50,230 (Camry = 21 weeks of income)

2024 median income $83,730 (Camry = 16 weeks of income)

Then I guess the median household income does not tell a proper story because of how many people are underwater on their car loans today, and why the 84 month loan is the new normal. Fact remains, we have apparently a much lower spending power. Lifestyle creep probably plays a part, but still. Numbers are one thing, reality may be quite another.

Facts are facts. Feelings are feelings. It takes 9 weeks less income for the median household to buy a Camry today than 3 decades ago. This is a fact.

Auto loans are increasing in term because buyers are choosing to buy more expensive types of vehicle than they did in the past not because the same model vehicles are getting more expensive.

The first 10 years the RAV4 was available in the USA it sold less than 100K per year. Then people decided they had to have a crossover instead of a sedan and sales took off. Last year they sold 475K. Just one example of a steady trend.

Most people should only every NEED one car loan and that is the first one. Buy a modest car, pay off the loan, keep saving those payments and the next time around you have options. At that point someone can either pay cash or – if the loan rate is low and less than can reasonably be earned holding onto that money – take out a loan.

Cars last longer today than ever. Cars are much cheaper, like for like, than they were 10, 20, 30 years ago. There is no reason to indenture oneself to drive more than basic transportation.

There are a lot of people near the bottom that need a car to get to where they can find work from where they can afford to live (not always within public transportation and shift dependent) who cannot afford to save enough to pay with cash for a super cheap used car. the car repairs and the cost of living may mean that they can afford to get a loan for a cheap used car that may be better and more reliable than what they have now but not save enough to pay cash in the time they need reliable transportation to work. Being poor sucks and it costs a lot to be poor.

You just described the reason for the first car loan. Then there is a decision to make – whether or not to continue the cycle of debt.

Yes, being poor sucks. Been there / done that / decided to stop making dumb decisions. At one time I was 3x my income in debt with no money in the bank. Then my employer started laying off people and I calculated how long I could go without a paycheck. That was an eye opening experience and we decided to make a change and get of of debt. Took us 8 years to dig out living on a razor thin budget.

Nicely done! We spent four years clawing out of the doldrums after the 2008 downturn and it felt like an eternity. Still have some debt, but it’s all real-estate related these days.

Luckily for us our wake-up call came in 2002. At the end of 2008 the company I worked for shut down and I was unemployed for 10 months. The good thing is that my wife had just finished university and had started working. So my unemployment set back our debt repayments but we stayed afloat.

Had we come into 2008 with our old mindset and spending habits I have no doubt we would have ended up bankrupt and lost our house. (Which dropped in value 50% and we sold in 2014 for less than we paid in 2007)

It is wild to me that people did not learn from 2008 – 2010. I see people with good paychecks doing the same stupid things and massively overextending themselves with the idea that housing prices always go up.

This may be of interest to some of you… it’s not unusual at all for boat loans to be up to 15 years. I have owned several pontoon boats for us on a lake near me and I financed the last one (which was dumb) and they offered me 5, 10 or 15 year terms on the loan. If you need 15 years to pay off a vehicle (esp a toy)….you can’t afford it.

At the last few boat and outdoor shows that I’ve been to 12 years seemed to be the sweet spot that I saw at most of the dealer booths. Not only was it shocking to my wife and I, but it actually made her mad. When we bought our used boat I couldn’t get my CU to give me a shorter term than 5 years. I guess that flexibility is nice, but we paid it off in less than 2 years.

“What car would you take a 180-month loan to buy?”

Sounds like the perfect way to get a brand-new 2023 Toyota Mirai! If I’m going to roll the dice on hydrogen becoming a widely available fuel, I want financing on a timescale with at least a slim chance of being commensurate.

House of cards.

Also, the whole 50 year mortgage thing to save $250 a month on the payment is insane to me. Just proves that people can’t math.

Matt, did you drink 30 beers last night to commemorate the Fitz?

Once took a four year rent to buy deal — luckily we moved house on the four years so had cash to buy — still got the car and it works fine 21 years later.

The financing added around €1,000 to the cost of the new car.

But I remember when I signed, four years seemed a very long time to be stuck with it.

If the car keeps going, and if I do a bit of work on bumps and scratches, it will now start to appreciate in value — a bit, as a young-timer classic. So they say.

Sadly, I know a lot of people that take 15 year car loans already.

Money is tight, we have too many bills!

Crap, my car is worn out we need a new one!

We can’t afford a new car payment, what do we do?

Ahh, refinance the house with money out, pay off the bills and get a new car.

Problem solved.

So, bingo bango, with a house, you can get a 15 or even 30 year car payment today.

And if you don’t have a house, just keep kicking the can down the road with balance transfers, debt consolidations, and rolling negative equity from one car into another. That’s a future you problem.

Yeah – also I do think we are nearing (how near? I don’t know) a point where it is a future-all-of-us problem when these finance bubbles and AI bubbles and stock market bubbles all start popping

What car would you take a 180-month loan to buy?

2026 Ford Ranger Super Duty 4×4 extended cab with a six foot bed. Set up for American roads. ie: driving on the right side.

Just think, within a few years of graduating college you could have you entire life plan laid out for you:

The American Dream

Those are all bad life choices that don’t need to be made.

yeap. Take student loans.

Now if you are looking at a degree with a very high earning potential (such as the classic STEM degrees), spending a bit more might be worth it, but in general, you can get a BA or BS degree with a lot less than $400k in debt. My daughter has less than $10k of debt with her BA.

The biggest place you can screw up #1 is not getting a degree but still going to college. There’s nothing wrong with not getting a college education, or getting one later in life.

For a lot of kids, I would recommend a “gap year”. Fly to Europe in coach, get a cheap youth Eurail pass for the summer and go around Europe staying in cheap youth hostels. For a LOT cheaper than a semester in a larger University, you can experience a ton of cool things, get to see a lot of a different of new perspectives and seriously damage your liver (drinking age in Europe is lower).

I had a coworker that took a gap year, after he had an expensive degree in Engineering. He came back and became a Chef. He could have saved a ton of money if he did his gap year before university instead of after.

My niece is starting college next year looking at nursing. Full cost for tuition + room and board at a state school is $33,000. Most people pay 1/2 that after direct financial aid (not loans)

She could go to the community college for free but we have advised her against that because there is a 2 year wait to get into clinicals – which means two extra years not using that degree and making money.

It is a shame that the gap year isn’t more popular in the USA. Of course that time would have to be used wisely. A year at home playing video games isn’t going to do much good.

It is good to learn what you don’t want to do. Spending the summer after I graduated working in a Tier 1 auto supplier running a rubber injection press provided a HUGE incentive to go to college. I was hating life after 3 months and looked around and saw people that had been doing it for 30 years – making a few dollars more an hour than me.

An old co-worker got out of high school and saw college as a waste, even though he had the grades and study habit to succeed. He had a friend that made insane money as a specialist roofer that did tin and slate roofs.

He spent a summer carrying tar to the top of old historic buildings, sometimes in period correct wool clothing. Made more in that one summer than he did for his first 2 years of engineering combined. But he decided that the money wasn’t worth the sweat.

He was an excellent student in college, he had the focus and motivation to get good grades to avoid roofing.

I did college wrong. I went to a high end out of state university. I knew what I wanted to be when I graduated going in. As I matured, I changed majors after ruining my GPA. Came out of college having spend (today’s dollars) about $150k of my parents money and being about $100k in debt.

In college, the first thing you did in class was to look for grey hair or wrinkles. Anyone over 30 was automatically going to ruin the curve. It wasn’t until into my second junior year that I had the study habits and motivation to work as hard as a 30 year old ex-marine or whatever who had gotten to the point where they realized they needed/wanted a degree.

My wife did college wrong the first time. Not that she didn’t get good grades but in that she didn’t investigate the career options of her degree before committing 4 years and $$$. The old “If you love your job your will never work a day in your life” BS that our generation was taught. Turns out there where very few actual jobs in her chosen field. So she ended up with a 4 year degree but working at vet clinics just like she did in high school.

A few years later she decided to go back to school. This time she looked at pay and job prospects and picked a field that sounded tolerable if not a dream job. At 25 there was definitely a group of adult students with a very different mindset vs many kids straight out of high school.

School is a full time job – a job you pay to work instead of getting paid – so you absolutely better make it worthwhile.

What generation? I am Gen X and had a someone from Gen Y yelling at me about how they were the hardest working generation because they were always told to give 110%.

Is that a common / known thing? I feel like I was always told to work hard (and always did / do). I also feel like Gen Z could have looked at hard-working Gen Xers and realized that dream was over before committing to it.

I believe Gen X is the first generation to do less well than their parents by several measures. Also the first generation to have to worry about retirement and switching employers / jobs / fields.

The Oregon Trail generation. We are right on the border between X and Y with traits of both.

My parents are boomers. They absolutely had to worry about retirement as my dad never worked a job with a pension. Quite common situation as only 24% of boomers had jobs with pensions.

By the time I entered the workforce pensions were no longer a thing – which was actually liberating. I didn’t have to worry about getting screwed out of a pension – I start out knowing straight away that my retirement was completely up to me.

I’m not saying these are the best choices. People are paying $50k for the average new car now.

People make life decisions because they have to, not because they have all the information.

I would have benefited from a gap year. Financially, it was not even remotely an option. The loans from that wasted year at college cost much more than a gap year would have, but there are grants, scholarships and loans for college. There are no gap year grants easily available without strings attached, or at least I didn’t know of any at the time.

Everyone has a different situation. Just from observation in college and then after college when I did a week vacation on Eurorail like a “gap week”, I think that a lot of kids that dropped out of college after building up huge debt would have been a lot better off to build up $10-15k of debt learning themselves in a gap year rather than $100-150k in debt flunking out of college.

People need shelter. It is a basic human need. Can’t really live on a park bench until prices or rates come down. Renting is an option, but landlords know what homes / mortgages in the area cost and adjust their rents appropriately.

College is what people do in order to get a job to afford to shelter and feed themselves. Sure, there are degrees that don’t pay but often you won’t know that until it’s too late. People were making six figures in the early 00s just for being competent in photoshop or website design in static HTML. A kid graduating with a degree in those skills in ’07 probably wouldn’t get past entry level before those jobs dried up entirely. It’s a similar situation for coding right now. Computers have so much memory and processing these days that we can just accept sloppy inefficient AI generated code… so good luck on that path.

Cars are almost universally a bad financial decision. They cost too much to buy even if you get a good deal. They depreciate. They require expensive maintenance and repairs.

Starting to save for retirement at 50 is a bad decision. But I’ve never faced the economic reality that young people today are facing. At one point, I owned two homes in the Boston area and just left one empty for a year because I was too busy to fix it up to rent or sell.

To your original points:

However if someone makes stupid decisions on items 1, 2, and 3 then it is entirely possible that they will be so loaded down with debt they have nothing left to save for retirement.

If someone lives in an expensive area that they can’t afford – move. I’m tired of hearing my younger colleges complain they will never own a house here on the west coast when they refuse to move. There are openings in our company in low cost parts of the country where they could easily afford to buy a home. However, they have to be willing to make the move to better their lives.

Don’t wait to start saving for retirement.

Also, when you first get a retirement option, be aggressive in investing. I started off with a “balanced approach” and was way off track from retirement in my early 30s, even though I was doing the right thing with saving. Then I changed everything to mega aggressive. I always picked what funds had the highest rates of return over 12-15 years regardless of short term performance.

I’m now mid-50s. I have caught up and am on track for retirement. I just switched to being balanced in investing and stopped getting the “are you insane?!” messages about how aggressive my investments were.

If I had been mega aggressive at 25, I would be ready to retire at 60 instead of 65+. If I hadn’t been mega aggressive in my 30s and 40s, I would not have a chance of being comfortable in retirement.

Ferrari 550 Maranello. Bound to appreciate, in fact already beyond my ability to afford one without ruining the rest of my retirement.

OMG, my favorite front-engined V12 of all time. I love everything about that car.

At current prices, a 15-year loan on a collectible Ferrari might work…

They look 100x better in person than in photos, where they can look too understated. It’s this and a 330 GTC (the first Ferrari I ever saw in print and in person) if I win the lottery.

My all-time dream car is a Verde Silverstone over Cuoio 575 SuperAmerica. I wouldn’t care if it was F1 or gated.

And yes, I know the clear flip roofs have a nearly 100% chance of delaminating, and are 401k-draining to repair. I guess I’d flip the roof closed only whilst washing it on Sunday mornings.

I’m not exactly one of the anti-financing people on here, but GODDAMN. Just the premise of a 15 year car loan makes my skin crawl. And the reality is, there’s no car on sale today that I could possibly want enough to be chained to for that long.

But it’s the 50 year mortgage premise that really freaks me out. Wow. What a nightmare that would be.

Ditto. I’m willing to accept that 7/8 years will become common, but doubling that feels insane.

Even the 7-8 makes me a little nauseous. My rule of thumb, is that I want the vehicle paid off before the powertrain warranty* is up. So in 5 years, maybe stretch to 6. Once I’m looking at 7-8, even if I’m not dealing with a catastrophe, I’m probably looking at significant maintenance costs. I just don’t want those two things overlapping each other. However, in a situation where someone is really committed to their basic transportation (Corolla for instance) and just badly needs the flexibility a low payment provides, I understand it.

*I do not condone 10 year loans on Hyundai products. That’s just suicide.

I mean I’d never use one myself. But something going a couple years longer than I’m comfortable with isn’t a hill to die on. If someone is really buying it and keeping it for a long time, fine. Anyone trying to flip out of an 8 year loan every 2-3 years is gonna get buried fast.

Yeah, I don’t want to be patching rust holes on a car I’m making payments on. One or the other’s tolerable – I’ve done both at different times – neither is best though.

Yeah here in the Northeast, a 15 year car loan is a great way to be making payments on a vehicle that’s threatening to disassemble itself.

So it was a fake meme but still spent most of the morning dump on it…ok

Let’s take a moment to reflect on those that sacrificed so much to protect the freedom of people to be so stupid with their money.

interesting that things you do not negotiate the price and take a loan out for have gotten cheaper and things you haggle over and take loans out have gotten more expensive. Computers/refrigerators(etc.) vs houses and cars.

Interesting examples, given that computers are getting more expensive (thanks AI!) and the refrigerator I just bought was more expensive and more cheaply built than the one I bought 15 years ago.

AFAICT, the only things actually getting cheaper are doing so by shrinkflation or crappier build quality.

Over the decades computers have gotten wildly fast and feature laden and the price has dropped. I paid over $2k for a computer in 1985 that did not even have a color monitor.

I just want to take a moment to appreciate how, instead of doing anything to redistribute obscene concentrations of wealth in the hands of a very few, the system is being urged to drive itself deeper, with manifold and fractal tentacles to pick more pockets deeper, longer than ever before. Four years becomes eight; eight becomes sixteen. It will be harder not to be impoverished than ever before; the system is being built to steal from you, with a smile that and a lie that’s it’s a flexible new option to help you with upward mobility in your housing, your transportation, your life. Nevermind paying $200,000 for a $45,000 car. What’s important is that it was an affordable monthly payment from a child’s birth halfway through high school, through four presidencies, through a fifth of your life.

What car would you take a 180-month loan to buy?

One big enough to live in, I reckon.

Do 15-year loans exist for hypercars? That’s not an echelon of vehicle I’ll ever attain (or really desire to), but I know very wealthy people do all kinds of loan deals to avoid paying taxes on assets like that. Like they could write a check for a Koenigsegg, but instead they set up some kind of leasing deal so it shows up as a different asset class.

I’m sure a lender would happily write up a 15-year loan on a Ferrari 250 given its appreciation, for example.

There are companies that specialize in this. I used to see one advertise in Hemmings all the time, Woodside Credit.

https://woodsidecredit.com/product/

They offer up to $1 million and 180-month terms on exotics and classics. So this isn’t really a new concept.

Yeah, I didn’t think it was a new idea. It’s just not a realm I’m familiar with, thus the question.

I think they just write them off as depreciating business expenses. My buddy who sells insurance somehow can completely write off the $100K F-350 he tows his camper with as a business expense.

Not legally. He just hasn’t been caught yet.

Pretty sure there’s a loophole there. Slap a wrap onto it and claim it as advertising expenses. Or mobile office if it’s fancy enough.

I always assume this is what is happening when I see a truck pull into a campground with a company name on the side.

Nope. Just not many IRS agents.

If a vehicle is over 6,000 GVWR you can write of 100% of cost in the first year. However, the vehicle must be used at least 50% for business. You can also only write off the percentage of the value that matches business use. So if it is 55% business you an only write off 55%. You also must have a legit business reason for the truck. You also must keep logs of every trip and whether it is business or personal and purpose and be ready to prove to the IRS that your business use percentage is correct.

Commuting does not count as a business use nor does towing a camper for vacation. I HIGHLY doubt your neighbor is only driving his truck to meet clients or evaluate properties for insurance claims.

CPA, this is correct. Plenty of people commit tax fraud, doesn’t make it legal.

Excellent information, thank you for writing it up!

Yes, and for exactly that reason.

I think the concept of ownership of anything has faded away from mainstream. We subscribe and rent apps and features. Most people buy homes and cars based off the monthly note. Some people (including my own mother) think that as soon as a car is paid off, you should trade it in on a newer one.

Besides a car depreciating, they have the chance of becoming almost worthless in an instant, even if it is not your fault. Longer terms will require additional gap insurance which you’ll never recoup. The fact that anyone could spin this as being good for consumers is slimy.

Well said. Also car repair and home repair and maintenance is also wildly expensive so some people are just thinking it is not worth it. Just rent or lease.

I’m still using a 2009 version of Photoshop because I will not subscribe to a monthly plan for something I use occasionally. (Or can you buy it outright now?)

Also on a serious note on the 15 year loan topic. In the Midwest you will be lucky to have a car for that long before rust kills it so to me that is just ridiculous for this area of the country.

Well that sounds suboptimal, subprime even.

15 Year loan for a car? NA1 NSX. I don’t thin a loan of that length makes sense for anything other than an already-classic car that you intend to keep for life, which I would with an NSX, but prices are far beyond what I could fathom right now. Anything on the front half of it’s depreciation curve, 15 years is insane.

“What car would you take a 180-month loan to buy?”

Lotus Esprit, because it’s been a lifetime obsession, and resale value would not matter. Wouldn’t really make any sense for anything else.

Stupid fake “memo.” Why would Cabinet secretaries be involved with creating a loan length? The market will figure this out without government intervention.

Big issue for lenders: is there, or will there be, a securities market to bundle 15-year loans?

Have you seen what these cabinet secretaries have been doing? That’s the least implausible part about this whole story.

Look, if you’re going to offer manufacturer-affiliated warranties, you should also be required to give a warranty for the entire length of the loan and the average vehicle miles per year (rounded up to the nearest thousand) times that length. And for 15 years at 14,000 (rounded up from 13,596 per FHA) that comes to 210,000 mile warranty. So sure, if you want to warranty the car for 15 years and 210,000 miles I might consider a 15 year loan.

The buyer would pay for that warranty. ALL business costs are passed on to the customer.

Now we might decide as a society that people will long loans should be required to carry a warranty as we have decided that all people must carry insurance. One could make the argument that people should be protected from their bad decisions.