Chances are that if you’re reading this, you’re a car dork. You browse sites like this one, argue about cars online, and scroll classifieds for fun, judging both the car and the seller. On weekends, you either wrench on a never-ending project or stand around a parking lot with coffee, looking at other people’s projects. Passion or addiction, you’re not entirely sure.

It’s easy to forget that most people are not like us. To them, cars are appliances. Tools. Transportation. They don’t know their oil weight, and they definitely don’t know the torque spec for their lug nuts. They may not even be able to tell the difference between a Chevy HHR and a Chrysler PT Cruiser. And yet, those people buy cars. In fact, automakers care far more about them than they do about us.

The New York Auto Forum is a daylong conference held just before the New York International Auto Show press days. It’s backed by companies like JD Power, S&P, NADA, and Cox Automotive, and it brings together everyone from dealer principals and analysts to OEM executives and media.

The presentations focus on retail strategy, dealer relations, and how to sell more cars more efficiently. But what stood out most to me wasn’t the strategy. It was the data, the trends, and the outlook. This data comes from JD Power, with some figures updated since the forum. Similar trends are being reported by Edmunds.

While enthusiasts like us might go to the ends of the earth to get a $3,000 shitbox Volkswagen, regular buyers, let’s call them “normies,” want deals too. There’s an entire multi-billion-dollar industry built around convincing them they’re getting one. But the data presented at the New York Auto Forum told a somewhat different story. And if you care about finances, it’s not a particularly comforting one.

Market Ups and Downs

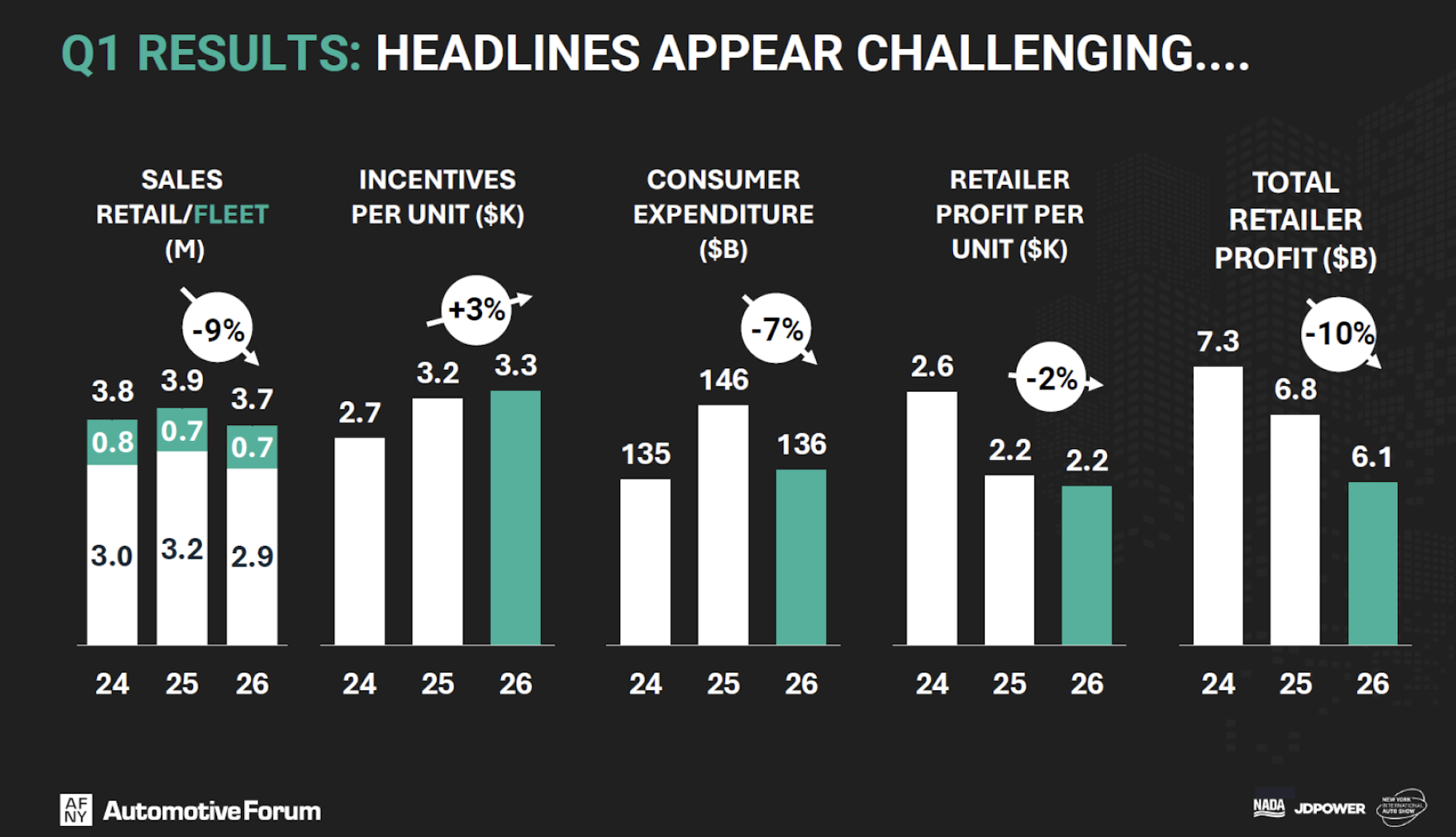

Let’s start with the market itself. In the first quarter of 2026, the average transaction price for a brand new car was $45,800 according to JD Power. The annualized vehicle sales ran at 3.7 million units, split between 2.9 million retail and 0.7 million fleet, down 9 percent from the first quarter of 2025. The industry will argue that some of that decline reflects demand being pulled forward by EV incentive changes and tariff-related buying behavior, but even with that context, the trend is clearly heading south.

Lower sales result in more vehicles sitting on dealer lots. That inventory is currently holding steady at around 2.2 million vehicles. To help things move along, manufacturer incentives rose slightly from roughly $3,200 to over $3,400 per vehicle, yet total consumer spending on new cars fell seven percent to $136 billion.

Dealers directly felt this impact. Total retailer profit dropped ten percent to $6.1 billion, though profit per vehicle remained surprisingly resilient at roughly $2,200 per unit, down just two percent. Those numbers matter to the auto sales industry. But what mattered more to me was what they revealed about the customers behind them.

Normie Affordability

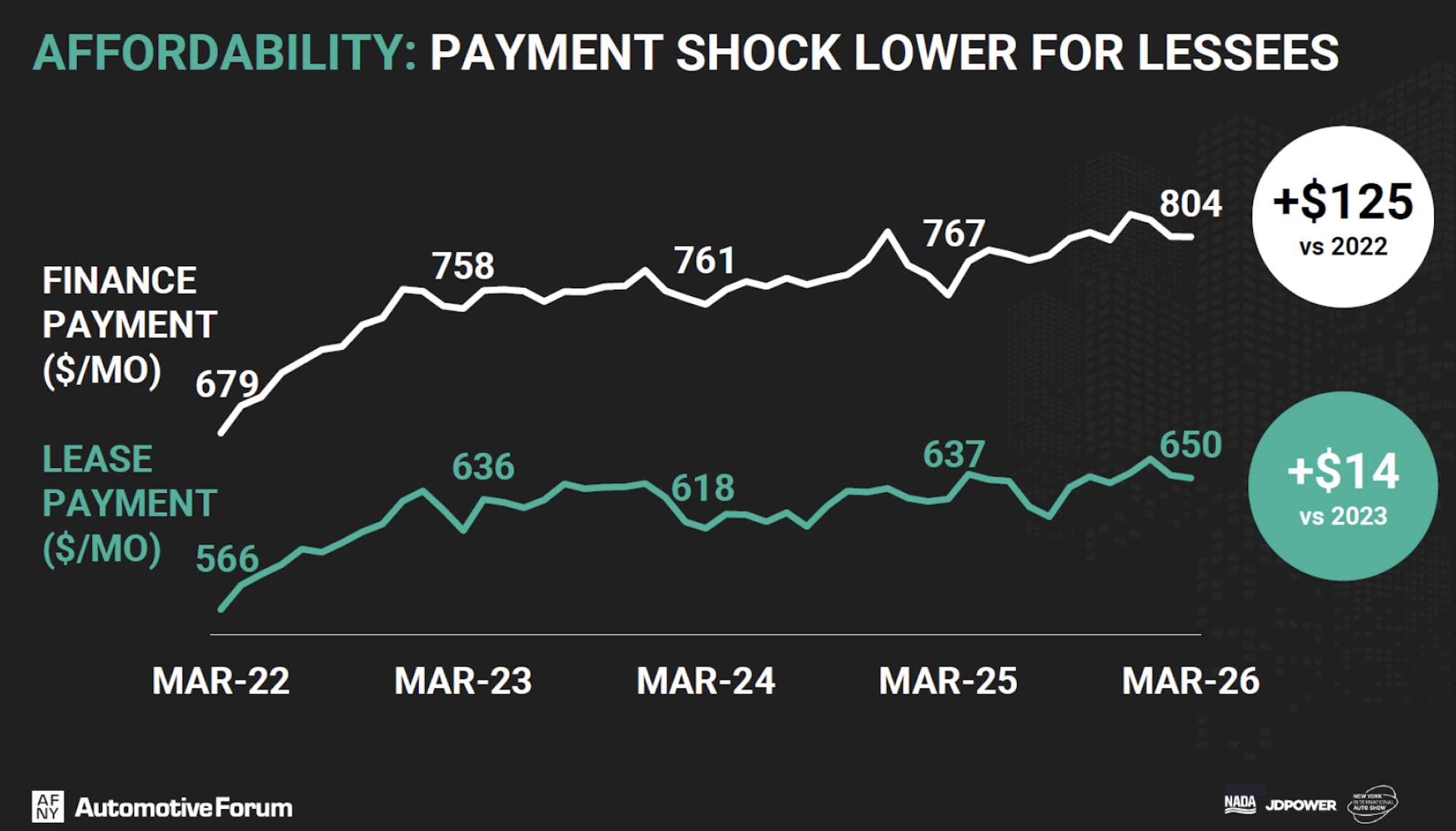

The industry term is “affordability,” which represents how manageable a new vehicle purchase appears to the average buyer after enough financing gymnastics have been applied to the spreadsheet. The average monthly lease payment for a new car is now $650, up a relatively modest $14 over the past few years. More shocking is the average monthly finance payment, which has climbed to $806, up $125 since 2022. Adding to the insanity is the fact that almost 20% of buyers now have monthly payments over $1000. That’s not luxury territory anymore, that’s the market.

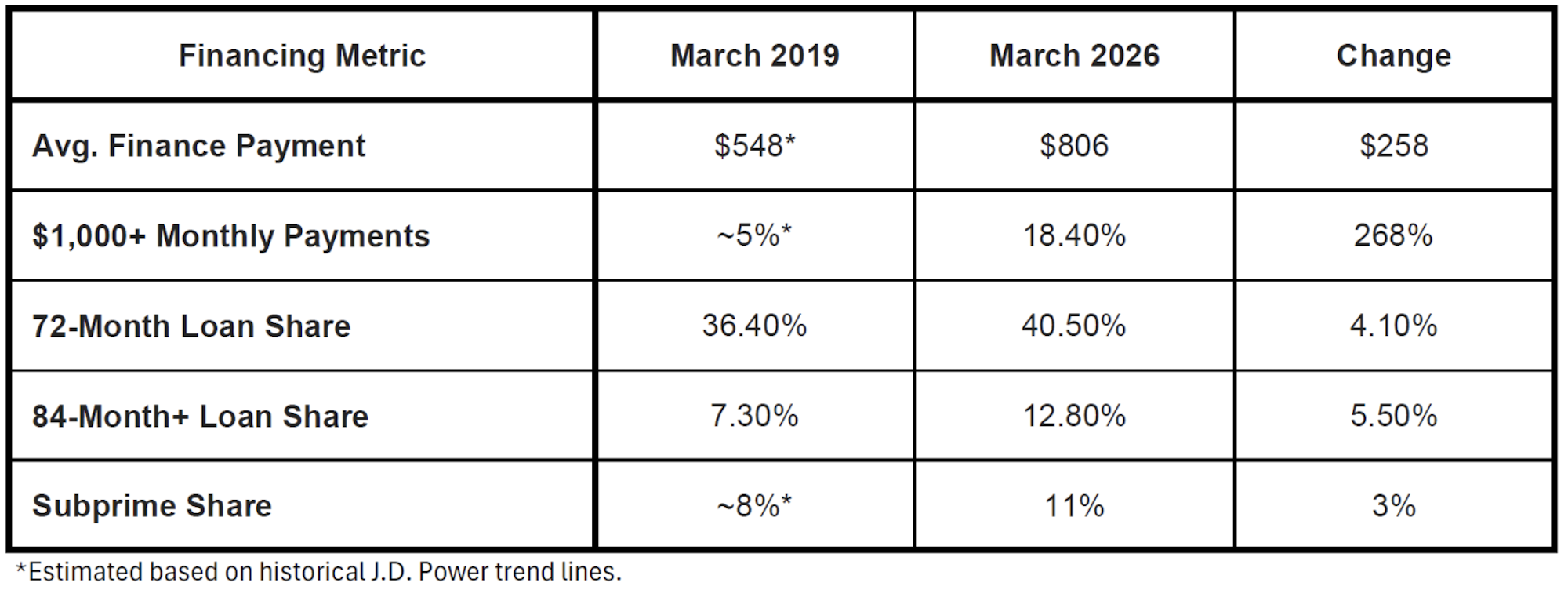

The numbers get worse when you look at how that payment is being achieved. The average new-car loan now stretches to 70 months. 72-month loans account for 40.5% of all sales, up 4.1 percentage points since March 2019. Worse still, 13% of buyers are signing for loans of 84 months or longer, up from 7.3% in March 2019. Subprime borrowers now account for about 11% of all loans and leases, the highest level in roughly a decade.

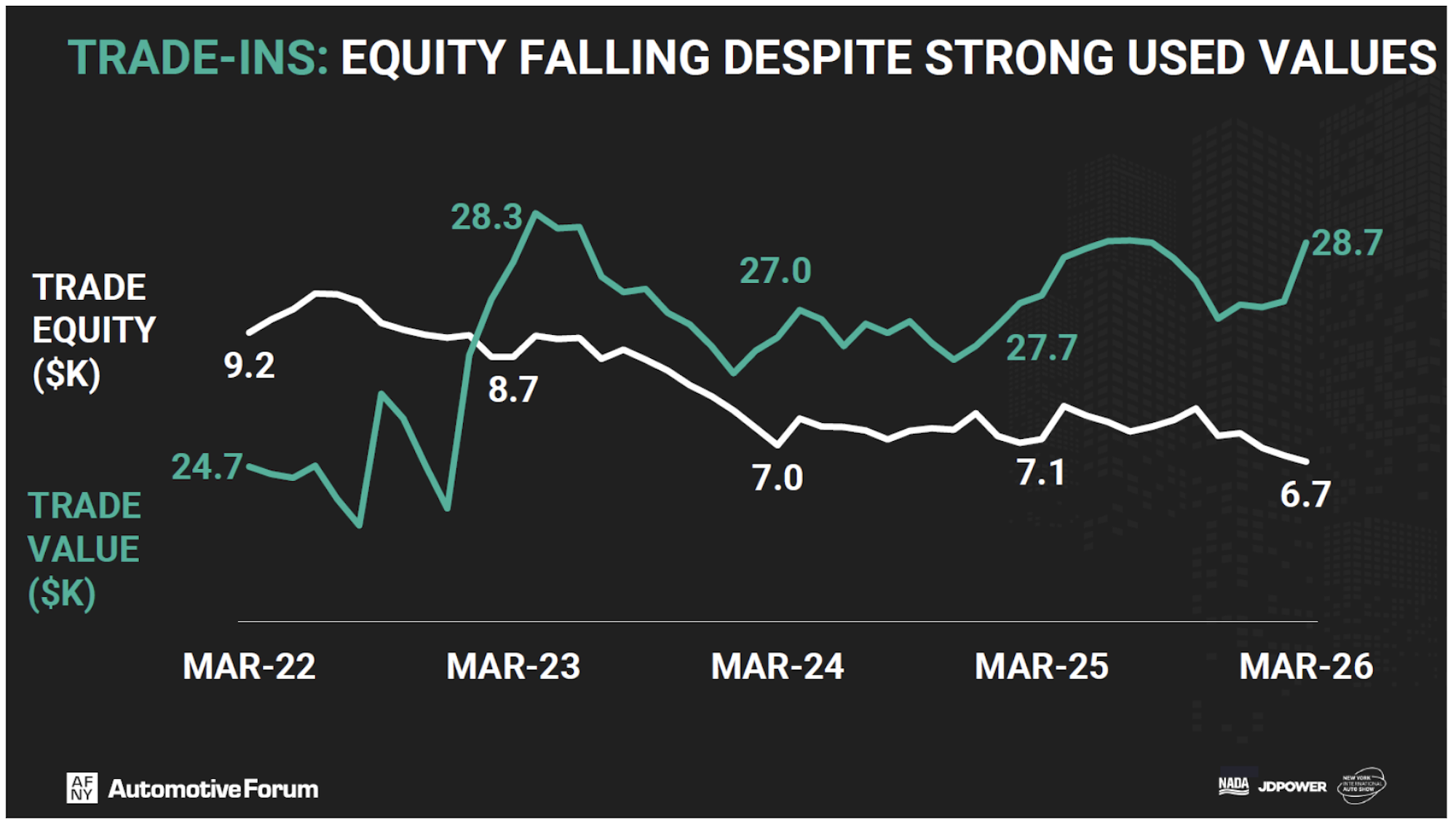

This brings us to how long the normies actually keep their cars. The average trade-in is now just 4.3 years (52 months) old and worth $28,700, meaning buyers are cycling through relatively new vehicles. But the average owner has just $6,700 of equity in said car. That means the typical trade-in customer still owes roughly $22,000 on the car they’re unloading. I physically choked on air when that slide went up.

Affordability Isn’t Equal

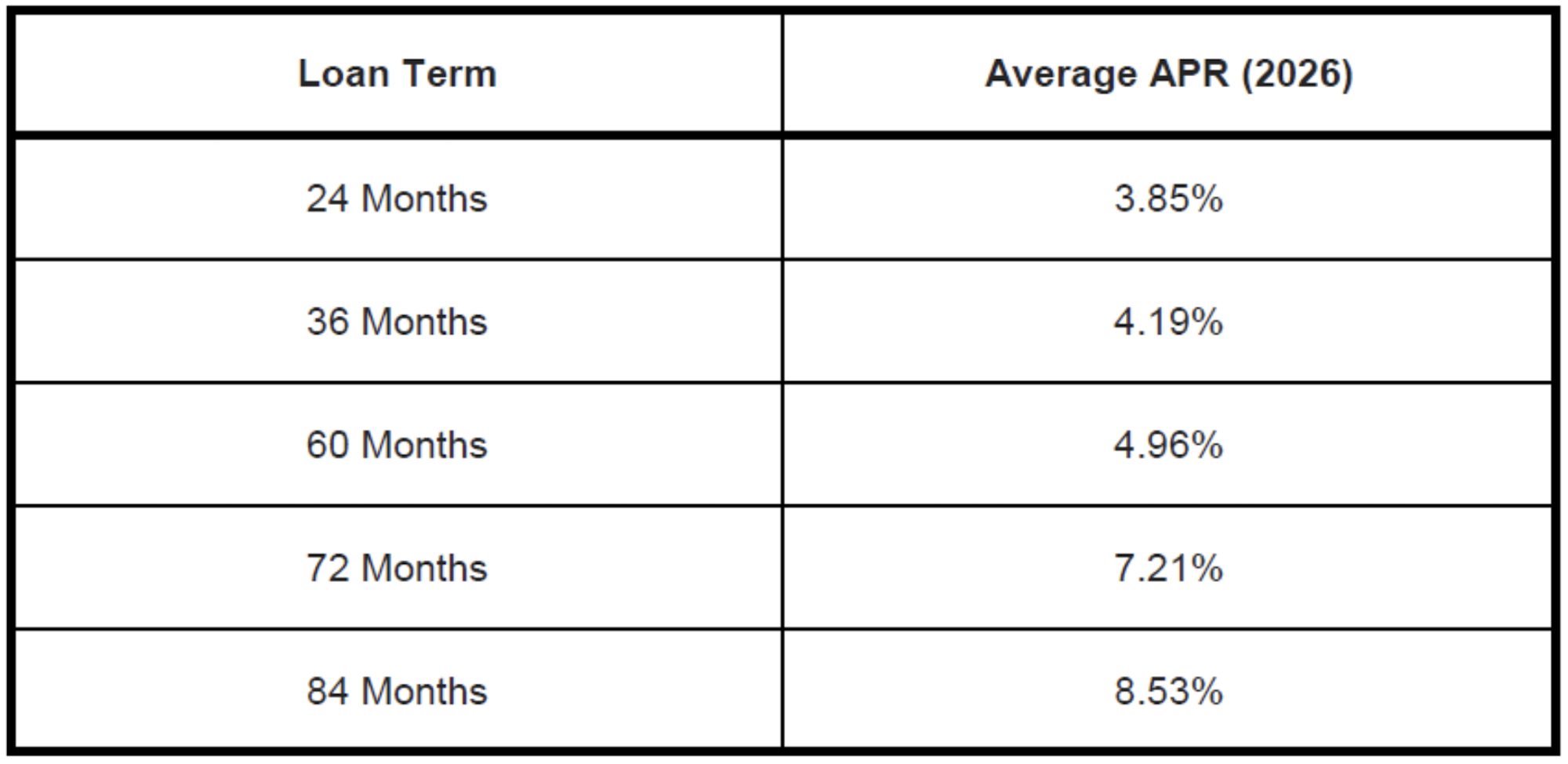

The longer loans have another hidden cost in them: interest. A 60-month loan carries an average interest rate of 4.96%. But since the market has aggressively shifted toward longer loans, the 72-month loan comes with a rate of 7.21%. If you pull the emergency lever for an 84-month term, a segment that has nearly doubled since 2019, the rate spikes to 8.53%. You’re essentially paying a 3.5% interest penalty just for the privilege of lower monthly overhead.

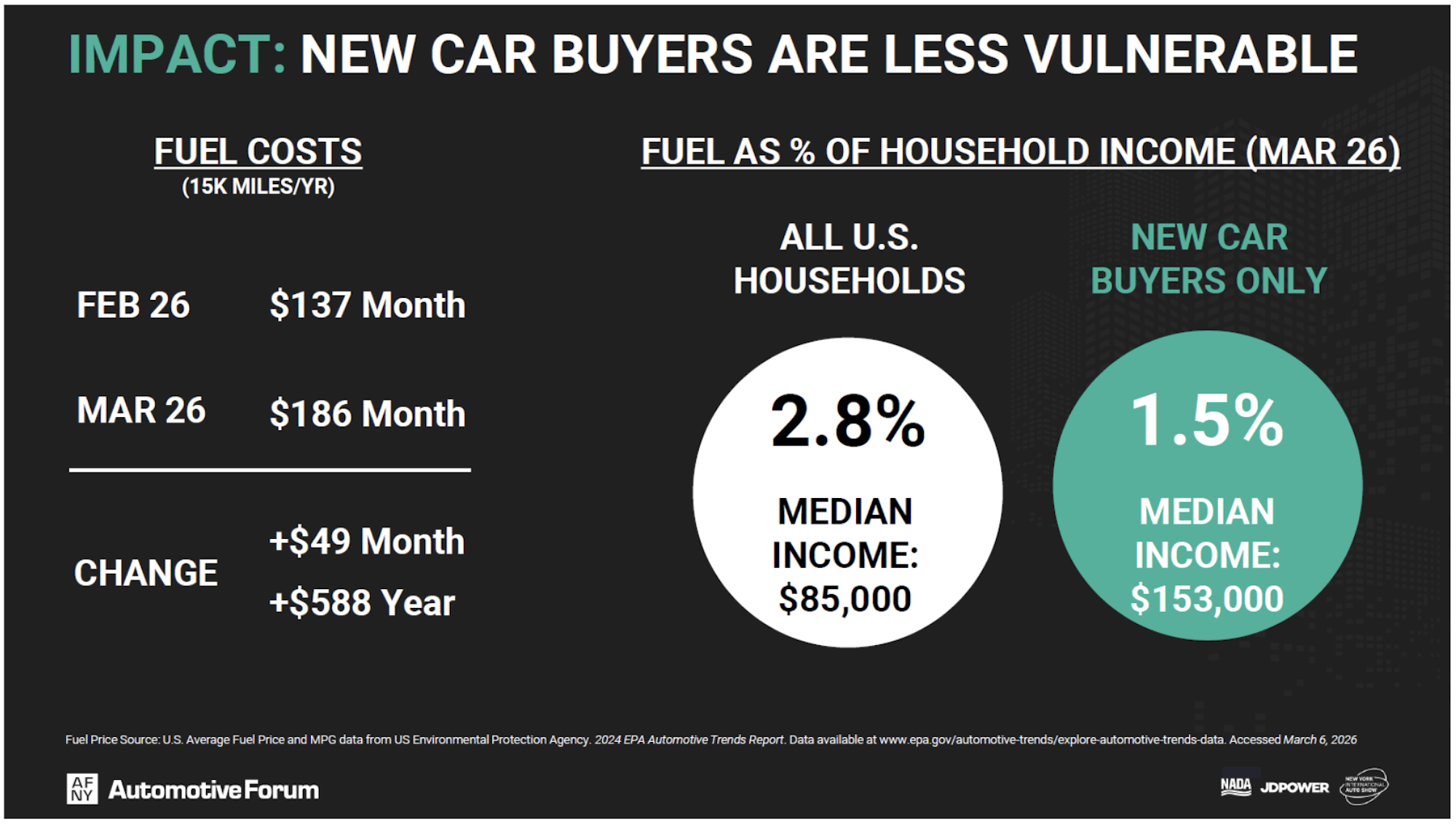

Adding to the affordability factor are fuel costs. Until March of this year, monthly consumer fuel costs, assuming 15,000 miles per year driven, were trending down from the height of $207 per month in 2022 to about $137 per month in 2026. However, that changed with the start of the Iran conflict, which drove fuel costs back up to about $186 per month and climbing. That’s an increase of almost $600 per year.

That number makes more sense as a percentage of income. The median U.S. household earns about $85,000 annually, putting fuel costs at roughly 2.8 percent of income. The median new-car buyer, however, earns approximately $153,000 per year, reducing that burden to about 1.5 percent. In other words, fuel costs matter less to the people buying new cars, which helps explain all the huge SUVs surrounding your rusted Miata at a light.

That stands in contrast to lower-income buyers, and this was a consistent theme throughout the presentations. Job growth and wage growth were described as weak, unemployment among younger workers and minority groups is rising, and disposable income is under pressure. Meanwhile, loan delinquencies continue to climb. For that segment of the market, affordability is starting to look a bit optimistic.

The Silver Lining for Dorks

So, is there any hope for us dorks in this sea of $800 monthly payments?

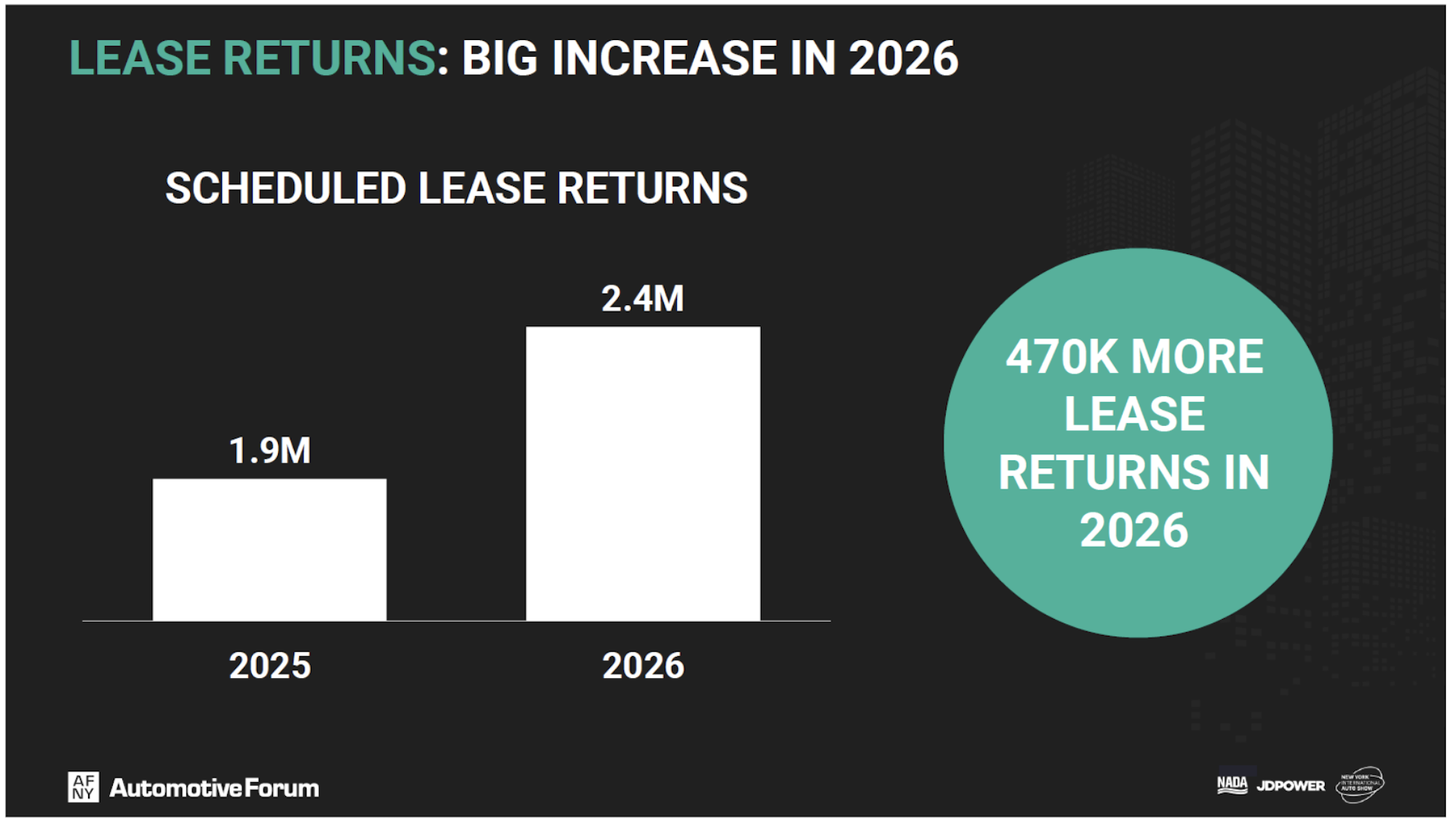

Maybe. Retail inventory has finally stabilized at around 2.2 million units, more than double the lows of 2022. More importantly, roughly 2.4 million vehicles are scheduled to come off lease this year, nearly half a million more than in 2025.

That means a wave of relatively new cars hitting the market. While the normies are busy stretching to make a $46,600 appliance work, that influx of lease returns might finally start putting some downward pressure on used prices.

What “Affordability” Really Means

So, what does all of this mean? For car dorks, the idea of “affordability” has always meant finding something interesting at a price that makes sense. That’s the game. But for most normal buyers, affordability means something else entirely. It means figuring out how to make a $46,000 car fit into a monthly payment, even if it takes seven years and leaves little margin for error.

The reality is that most buyers aren’t really shopping for cars. They’re shopping for monthly payments. The price of the car almost doesn’t matter as long as the number at the bottom works. The algebra is simple. A $50,000 car financed over 36 months at 4.25% is a $1,481 payment. Stretch that to 84 months at 8.53%, and it drops to $793. The buyer “saves” $688 per month today, but in reality, they pay $16,612 in total interest over the life of the loan, compared to just $3,316 for the shorter term.

The system, for better or worse, still works. Cars are still selling, and the numbers still add up on paper. But they only add up because the definition of affordability has been stretched to make them work. The industry will sell this as normal. For the normies making the payments, it should not feel that way.

Top graphic images: DepositPhotos.com; New York Automotive Forum

If you cut off the credit, the prices will come down.

The rising tide of wealthy drivers buying land-yacht mall cruisers is lifting all ships. You can’t stop them but you can stop the other 90% of the population.

No loans past 60 months, stricter approval standards. Suddenly Toyota can’t charge $10k more than their cars are worth ($35k for a Corolla Cross with AWD, seriously?!). Easy, problem solved.

Side note: I wish enthusiasts would stop gloating about riding out a field of old hoopties until they evaporate into rust dust.

Normal people don’t/can’t do this much longer. Safety standards, vehicle weights and driving conditions have changed so much in the past two decades.

I won’t put a newborn in a 1999 WRX when the average car in my neighborhood weighs 6000lbs and is driven by a distracted sociopath.

Maybe you won’t put a newborn in a 1999 WRX but others don’t have a choice what they drive. A 99′ should be way safer than a pre 90’s car, Abs standard and real crumple zones.

Yeah obviously. They don’t have a choice but they should. That’s my point.

I’d like to see a chart comparing over time the overall amount of payments going towards interest/fees vs. equity. I’m guessing the former is increasing and the latter is decreasing as time goes on.

Not the most encouraging data for our conomy/society, but:

I think the “paying for maintenance and repairs” factor is also huge for non-enthusiasts (i.e, the normies in question). Someone in my family is not quite at that median income level, but still leases a new base model Corolla Cross because keeping up with a used car is still a time/money suck, and for their small business a major factor was not having down time for the vehicle.

It does seem like lots of folks are getting in over their heads or buying too much car, though.

And because used car prices are still elevated, it means that buyers of these cars are also getting a terrible deal. They’re buying a vehicle that’s not far off from it’s most maintenance intensive years and they’re often the consumers for which maintenance costs are most likely to be a burden.

This is a valid point. I see many people saying go buy a 10+yr used car for 5k, but they don’t seem to consider maintenance cost and downtimes associated with this.

However also seeing people opting to “lease” $60K~80K cars while not being able to purchase one due to high monthly payment, gives me mixed feeling on current economy

When I looked up the inflation adjusted price of my truck for a Curbside Classics article I had a moment of illumination. My 2002 F150 would cost over $50,000 today, which means prices doubled in just under 25 years. Even our much newer Mazda CX-5 is noticeably more expensive. As a result I now have a fleet of older cars bought with cash and no intention of taking on a car loan comparable to a mortgage payment

As a result I now have a fleet of older cars bought with cash

This loan thing, what’s that?

Oh, “new” cars.

“ It means figuring out how to make a $46,000 car fit into a monthly payment, even if it takes seven years and leaves little margin for error.”

Alternaively, it can also mean picking a cheaper car where the payments are done before the factory warranty runs out and a car with a lower TCO… So insead of getting that Grand Highlander, get a Prius or Corolla hybrid instead.

In my view, anyone looking at financing for longer than the factory warranty needs to scale their expectations DOWN to get things in-line with their financial situation.

But, if I buy a lesser car, how will I impress people I don’t even know?

They’re the only ones you can impress.

You weren’t gonna impress them anyway!!! LOL

You don’t know how much of a poseur I am!

This would involve convincing Americans that their 2 kids and occasional vacations with a few duffel bags could theoretically fit in a Corolla. Impossible. You have to have the 3-row seating! (Sarcasm)

It’s basically impossible to fit rear facing car seats in a Corolla though. Unless you want to be dangerously against the front dash board.

It’s true, we were so happy with our little hatchback until car seats came into our lives. Now we have a midsize car just so the four of us can all fit (without anyone’s face in the windshield).

Once both kids are in boosters, though? Back to the cheapest thing I can run!

I was thinking more along the lines of preschool and elementary-aged kids, but I do get your point there. It’s why I went from a Mazda3 to a Mazda6 when my son was on the way in 2015/2016.

“It’s basically impossible to fit rear facing car seats in a Corolla though.”

That’s not true. I have 2 kids and when they were small, I fit rear facing seats into similarly sized vehicles such as a Honda Civic and Ford Escort.

Of course I also made a point of NOT getting the massive SUV-sized car seats or the SUV-sized strollers.

As long as you’re careful with what you buy, something the size of a Corolla absolutely can work if you have two kids.

The Diono car seats are the best for that. We had a CX-5 that we downsized to once we got tired of the payment on the 2019 Toyota Highlander we had, and I swapped to the Diono Radiant car seat for my daughter. Way narrower and fit much better while still having good safety ratings.

We had Diono seats as well. Great when installed, but a royal PITA to swap between cars.

I know it’s sarcasm, but we actually lived this for a long time: 2nd gen Nissan Leaf, BMW M3 coupe, and a Jeep YJ.

Our family of four did kayak trips in the M3 with 2 kayaks on the roof rack (Jeep couldn’t do it with the soft top). We did a few weekend family trips with the Leaf with two carseats (front facing at least), stroller, sleeping bags, and a carryon bag or two.

Last year, I finally broke down and got my wife the 7-seat SUV she wanted (Mazda CX-90), and I get it. It’s not just “2 kids and occasional vacations with a few duffel bags”, it’s “sportsball practices and games 3-4 days a week where we can finally contribute to the carpool”. We’re using that 7 seat capacity at least 3 days a week now where it wasn’t even a possibility before.

I still think a minivan is the most efficient 7-seater, but I just can’t bring bring myself to get one, nor can my wife. We both know it’s the “smart” decision, but neither of us can overcome the minivan stigma, and we’re willing to sacrifice some efficiency for that. Still, the CX-90 PHEV gets 50mpg combined and feels like Range Rover inside, so there’s that.

I fully agree you CAN use a Corolla as a family hauler, but there are legitimate reasons for more seating capacity (though the SUV format isn’t necessarily the answer).

I get it, because we have a minivan as well. It’s just a 2018 and is also a Kia (which I will dump as soon as its CarMax warranty expires). The space is nice. What I mean is if you cannot afford a bigger vehicle, or if you can only afford an older one, get what works financially. Too many folks refuse to buy within their means and make things work that aren’t ideal and end up overextending themselves money-wise. Did we *want* to do vacations in my Mazda6 with the two kids and our stuff filling the trunk to the brim? No. Did we anyway until we could manage buying the minivan? Yep.

This is really the crux of it. Our materialistic society has sold the American dream as having a 4-ton Suburban in the driveway, and it’s ok to borrow like there’s no tomorrow.

How’s the CX90 PHEV been treating you, reliability-wise?

I went to test drive a 2026 this weekend, and it had a check engine light and the A/C didn’t work until we restarted the car. I’d say that soured the test drive quite a bit, but I’m open to trying again with one that isn’t broken.

Well, ours is a lease, since Mazda offered a fire sale $15k off MSRP right as the EV credit lease loophole was closing. Even if we buy out the lease, it will be cheaper for us overall than if we’d bought the CPO one we were looking at.

That said, we haven’t had a single drivetrain issue. We did have issues with wired CarPlay, but we traced that to a bad USB cable, which isn’t Mazda’s fault. Wireless can be a little sluggish to connect, but is fine once connected. No issues with any other vehicle functions like the auto-steer cruise control, etc. It really get the full 24miles of EV range it’s rated for, and it charges in just a few hours on the 220V home charger we have.

The PHEV system is a bit more jarring in transitions between ICE and EV than I think it should be, but I’m comparing it against my full EV daily, and that’s just in the tuning. It’s not uncomfortable, but I think it could be improved. Note also that it requires Premium fuel, which is weird for a non-turbo four cylinder, but I assume it’s because Mazda has such high compression engines. Gas is expensive AF right now, but we can go over a month between fuel ups just remembering to charge it each night.

It is cool to feel the gears shifting in full EV mode, though. It uses at least 2-3 gears out of the 8-speed box, which is an odd sensation in an electric car.

The shifting does sound pretty interesting! It wouldn’t let me try EV mode, so couldn’t experience that. Currently have 2 EVs (Tesla 3 & X), looking to swap the X for a PHEV 3-row that’s actually practical and doesn’t embarrass the kids with stupid gimmicky doors.

Good to hear you’re having good luck mechanically, it’s so hard to find the positive stories online. Still not a great first impression with our tester.

Cross shopping the Volvo XC90 T8, and it’s very smooth when the ICE kicks in. Helps that their setup is kind of unique, in that the electric drive unit only powers the rear wheels, and the ICE only does the front. Overall that car is very refined and comfy. The base suspension is super smooth, so I don’t think the air shocks are even worth it. Pricing wise, though, need to get one a few years old.

I actually thought the 2026 CX-90 we test drove did a pretty good job with the transition between EV & ICE. Shifting seemed smooth as well. Overall felt pretty good to drive, just had a stiffer ride with the sportier suspension than the Volvo. I also quite like the optional center console between the 2nd row captain chairs. Very classy overall. Looks incredible in the Artisan Red, but my wife would never go for a red SUV.

I’m used to Premium from Mazdas, being a 2001 Miata caretaker. 91 octane to make 140hp (25 years ago)? Volvo is the same way, though they’re squeezing 300+hp out of a little 2.0T.

I also had an NB Miata (10AE), and it was pretty nice inside and well equipped for what it was.

We cross shopped the XC90 T8, but the price premium was the major factor. Plus, our extended family has had Volvos and they were in the shop often enough for them never to keep them out of warranty. Not “unreliable” per se, but out of warranty maintenance/repairs would have added up quickly (same experience as BMW).

Yep, this is sort of my rule of thumb. If you can’t pay the car off by the time the powertrain warranty is over (excluding H/K) then you need to move down-market.

This is even more important for used cars. People (especially here) seem to believe that “you can get a better used car for the same amount of money as a new cheap car” but this logic is how I find doofus after doofus financing 5 year old Grand Cherokees for 5+ years.

Hard Agree! And financing this vehicle as it enters it’s least care-free years.

Yeah, a lot of people seem to think that just because a car should last 15-20 years, that the final 10 years involve minimal maintenance. Making payments while also being on the hook for brake jobs, suspension parts, etc. doesn’t really work for me. Hell, tires are expensive.

A lot of people seem to pretend like those first 3-5 years have no real value. And I’m like, lol, those first 3 years you shouldn’t have to do ANYTHING.

Well, sure I can’t afford it now. But 84 months is a long time! I bet by the end I’ll finally get that promotion I’ve been wanting, and surely nothing else will get more expensive in the meantime!!

Crap like this is why A.) I’m still rolling the 2016 Mazda that I bought new in October 2015 and B.) My wife and I are cancelling our Vegas vacation we had planned for this September and selling the concert tickets we had (the reason for going). 🙁 I just feel like things are financially going to hit the fan (worse than they already have).

“ Vegas vacation” I was envisioning a vexation of Vegas, or whatever, maybe a curse of Chevys? Anyway, whatever the equivalent of the Porsche Parade is. But with Vegas.

Unfortunately, just Las Vegas. Not Chevy. I could likely afford a Chevy one.

I was thinking National Lampoon’s Vegas Vacation with Chevy Chase.

At least there’s another global conflict so you can pay way more for gas. Taste the freedom

Yes, so much shit, and so many fans too.

I’m going to disagree with a broad swath of this. The salient data, followed by my points below:

To start with, my old refrain: Nobody needs a new car. The average age of vehicles on the road is 12 years. Of the two cars in my fleet, one is 11 years old and one is 27.

Second, we can generally assume that if the average age of vehicles is 12 years, then there’s about 10% churn annually in the market as vehicles are added to the overall population and old vehicles are traded out. A top 10% income household is right around 210k-250k, so not all that far off from the median income of 153k for a new car purchaser.

It’s not “normies” buying new cars. It’s not “normies” trading them in at 52 months. It’s top-quintile income earners. Which is fine; I’m not going to get too worked up about a guy pulling down a quarter-mil a year having to spend (checks math) 5% of his gross income on a 1-kilobuck car payment.

Re:10% churn, I think the number is closer to 5-6% if the average age is 12 years so this means we have a lot 20+ year old vehicles on the road.

I think the problem is people making $250k still balk at $1k/month payments. I make about that much and even a $500/month payment seems insane to me. We keep our cars a long time (8+ years), so I don’t feel bad about buying new when depreciation will have flatlined by the time we eventually sell it, and I put a substantial amount down to keep the loans short and cheap. Others I know who earn in the same ballpark do the same thing or buy used.

We also don’t have more than one car payment at a time. Even though my wife’s car had a 6-year 0% interest loan, we paid that off early before I got my new car (which got $10k back in fed+state EV credits back when that was a thing). Not the savviest financial move given my wife’s loan was free, but we didn’t want the liability of two loans if poop hit the fan.

“Retail inventory has finally stabilized at around 2.2 million units”. 90% of that would be Dodge Hornets one assumes.

Meanwhile… I found a new (Ok… 2025 but still new) Ioniq 5 awd for a bit over 30K. 48 month loan with payments under $400. Yes… I paid for a good chunk in cash.

It doesn’t have ventilated seats or rear heated seats… but it has wireless CarPlay. It also has 800v charging and is averaging 4.0 miles per kWh over the 1500 miles I’ve put on it. It’s comfortable, roomy and fun to drive. It holds about as much as our Outback… and accelerates faster than most supercars from not too many years ago.

Not sure what I’m missing for not spending nearly $20K more to get an “average” car. Other than bigger payments.

If I had a regular place to charge, this is exactly what I would’ve done. EV depreciation is amazing. Instead, settled for a Prius.

Yes a finance article. Of course since the normies are trading in their new vehicle at 4 years with $6k in equity that is 3 years of interest and car payment they are not paying.

This fact – trading in for a new vehicle at 4 years with $6k equity – interested me too. Compare that to turning in a 3 year lease with no equity but much smaller payments over the similar time period. If you are going to be constantly paying for a new or new-ish vehicle, why not pay less each month?

My dad once told me that in 1965, his payments on our second car—a ’65 Malibu convertible—and the mortgage were both $83, with no other debt. He worked at the National Bank of Detroit, bringing home $150 a week, while my mom was a full-time teacher, so I guess we were doing alright. We even had a “maid,” Rilla, who came over a few times a week. Even though we lived in a typical middle-income, Leave It to Beaver-style neighborhood, more than a couple of neighbors also employed “help.” Decades later, my mom said it was more of a fad or status symbol, and it always made her feel uncomfortable. I remember them being dropped off and picked up in mostly ’50s cars that looked so different from the “modern” cars of the time.

Other than the fuel graph, none of those are adjusted for inflation making it harder to see if affordability or just inflation or a mix is at play here.

This.

“The industry will sell this as normal.”

Because it’s the *new* normal. Oceania was at war with Eurasia; therefore Oceania had always been at war with Eurasia.

“regular buyers, let’s call them “normies,” want deals too. There’s an entire multi-billion-dollar industry built around convincing them they’re getting one.”

Too bad they can’t just cut out all those middlemen and pass the savings on to those normies.

Great article but it really bugs me that some of the graphs aren’t scaled properly :/

Agreed. And the most annoying – the finance payment is vs 2022, while the lease payment is vs 2023. Big difference between 2022 and 2023 in those numbers.