Chances are that if you’re reading this, you’re a car dork. You browse sites like this one, argue about cars online, and scroll classifieds for fun, judging both the car and the seller. On weekends, you either wrench on a never-ending project or stand around a parking lot with coffee, looking at other people’s projects. Passion or addiction, you’re not entirely sure.

It’s easy to forget that most people are not like us. To them, cars are appliances. Tools. Transportation. They don’t know their oil weight, and they definitely don’t know the torque spec for their lug nuts. They may not even be able to tell the difference between a Chevy HHR and a Chrysler PT Cruiser. And yet, those people buy cars. In fact, automakers care far more about them than they do about us.

The New York Auto Forum is a daylong conference held just before the New York International Auto Show press days. It’s backed by companies like JD Power, S&P, NADA, and Cox Automotive, and it brings together everyone from dealer principals and analysts to OEM executives and media.

The presentations focus on retail strategy, dealer relations, and how to sell more cars more efficiently. But what stood out most to me wasn’t the strategy. It was the data, the trends, and the outlook. This data comes from JD Power, with some figures updated since the forum. Similar trends are being reported by Edmunds.

While enthusiasts like us might go to the ends of the earth to get a $3,000 shitbox Volkswagen, regular buyers, let’s call them “normies,” want deals too. There’s an entire multi-billion-dollar industry built around convincing them they’re getting one. But the data presented at the New York Auto Forum told a somewhat different story. And if you care about finances, it’s not a particularly comforting one.

Market Ups and Downs

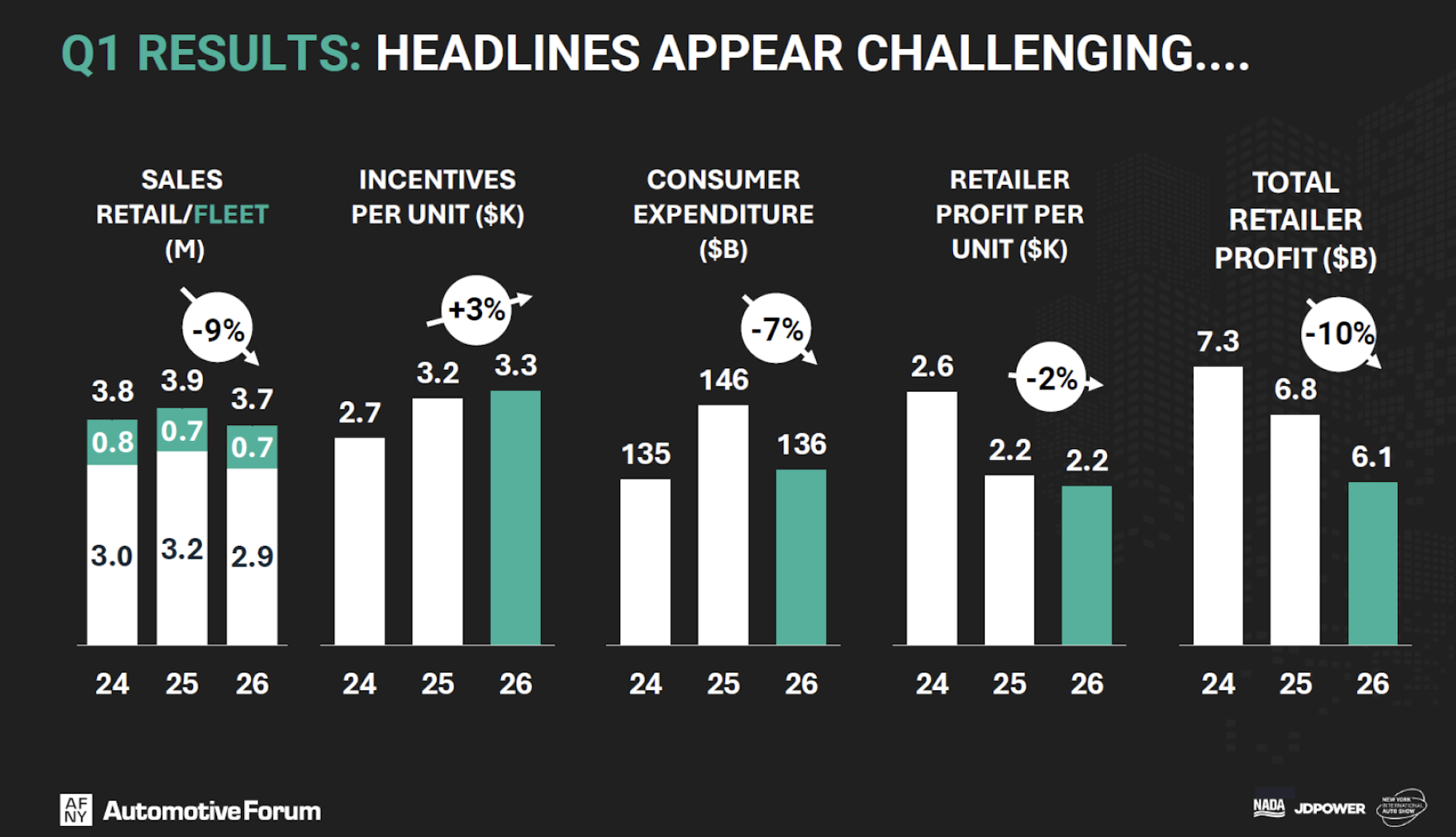

Let’s start with the market itself. In the first quarter of 2026, the average transaction price for a brand new car was $45,800 according to JD Power. The annualized vehicle sales ran at 3.7 million units, split between 2.9 million retail and 0.7 million fleet, down 9 percent from the first quarter of 2025. The industry will argue that some of that decline reflects demand being pulled forward by EV incentive changes and tariff-related buying behavior, but even with that context, the trend is clearly heading south.

Lower sales result in more vehicles sitting on dealer lots. That inventory is currently holding steady at around 2.2 million vehicles. To help things move along, manufacturer incentives rose slightly from roughly $3,200 to over $3,400 per vehicle, yet total consumer spending on new cars fell seven percent to $136 billion.

Dealers directly felt this impact. Total retailer profit dropped ten percent to $6.1 billion, though profit per vehicle remained surprisingly resilient at roughly $2,200 per unit, down just two percent. Those numbers matter to the auto sales industry. But what mattered more to me was what they revealed about the customers behind them.

Normie Affordability

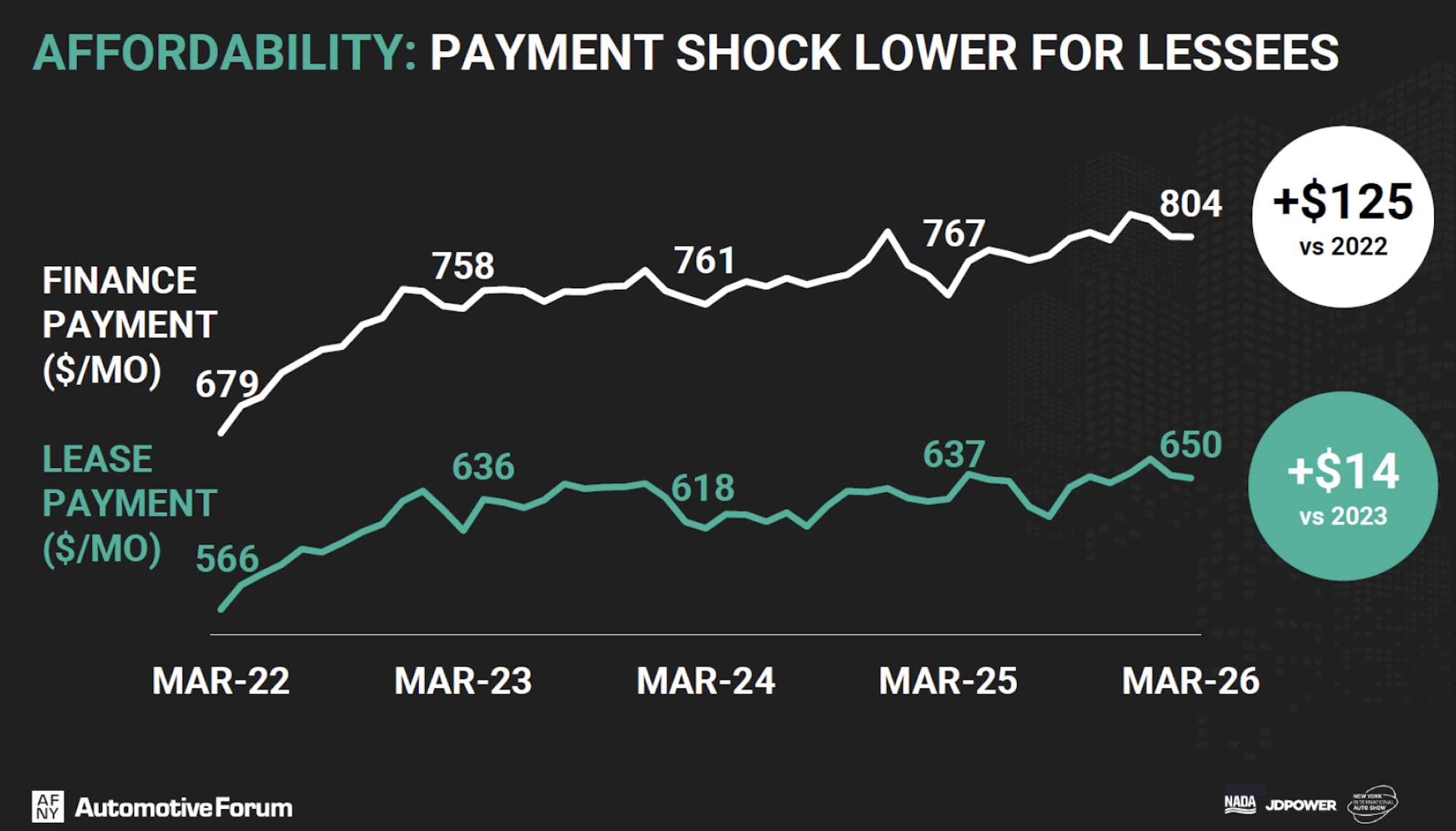

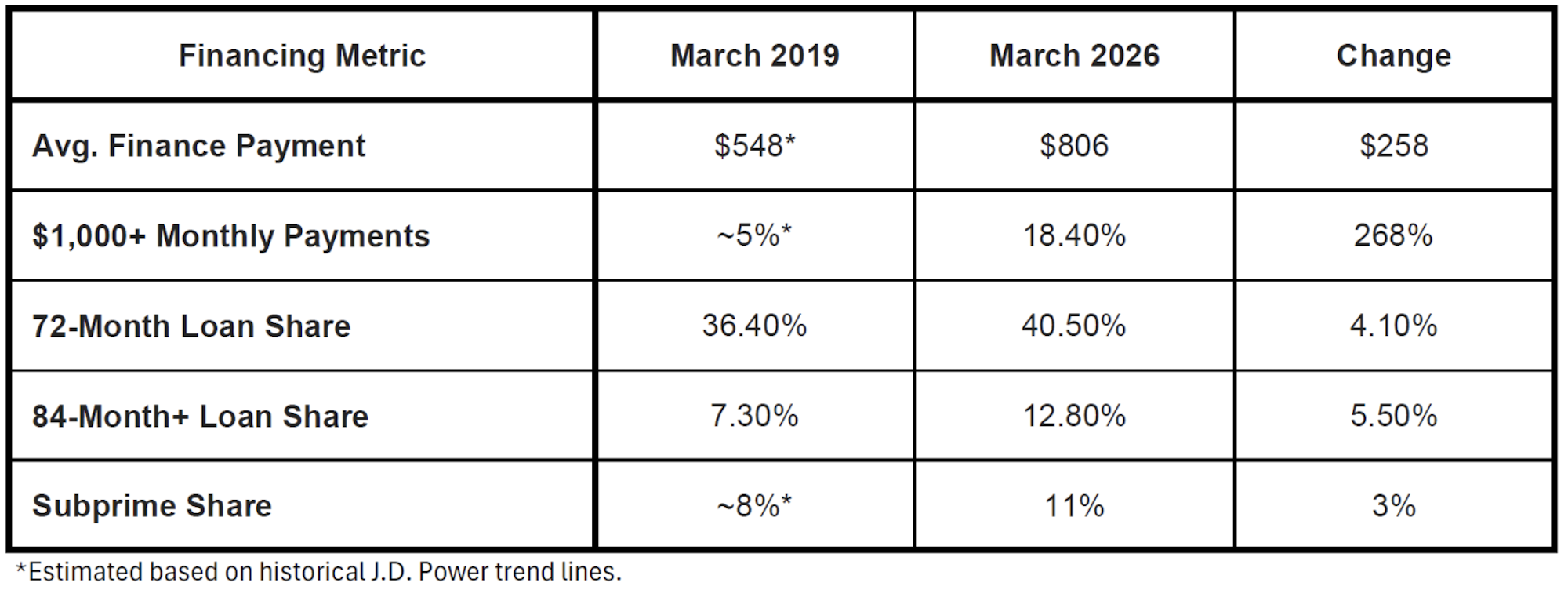

The industry term is “affordability,” which represents how manageable a new vehicle purchase appears to the average buyer after enough financing gymnastics have been applied to the spreadsheet. The average monthly lease payment for a new car is now $650, up a relatively modest $14 over the past few years. More shocking is the average monthly finance payment, which has climbed to $806, up $125 since 2022. Adding to the insanity is the fact that almost 20% of buyers now have monthly payments over $1000. That’s not luxury territory anymore, that’s the market.

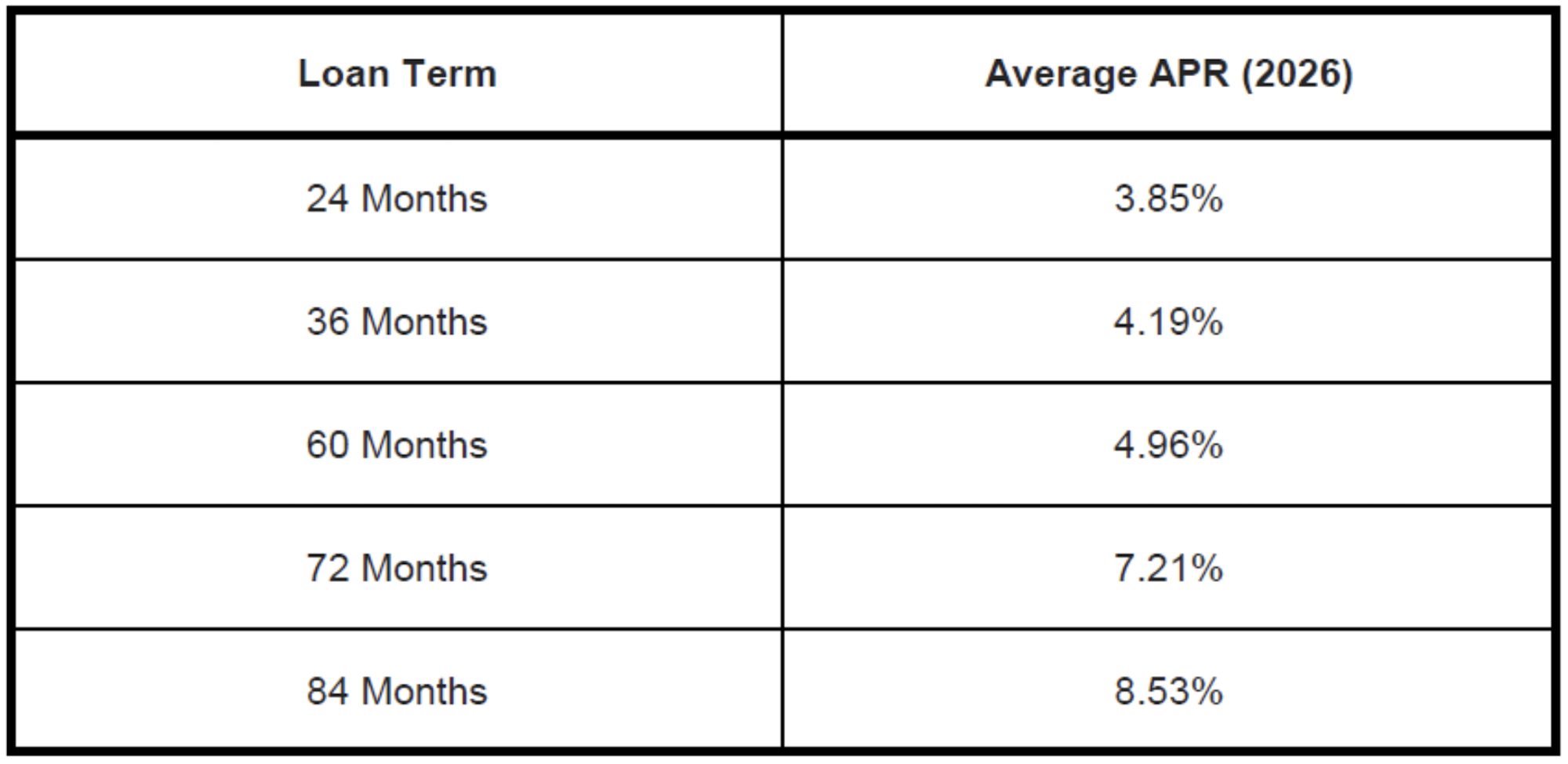

The numbers get worse when you look at how that payment is being achieved. The average new-car loan now stretches to 70 months. 72-month loans account for 40.5% of all sales, up 4.1 percentage points since March 2019. Worse still, 13% of buyers are signing for loans of 84 months or longer, up from 7.3% in March 2019. Subprime borrowers now account for about 11% of all loans and leases, the highest level in roughly a decade.

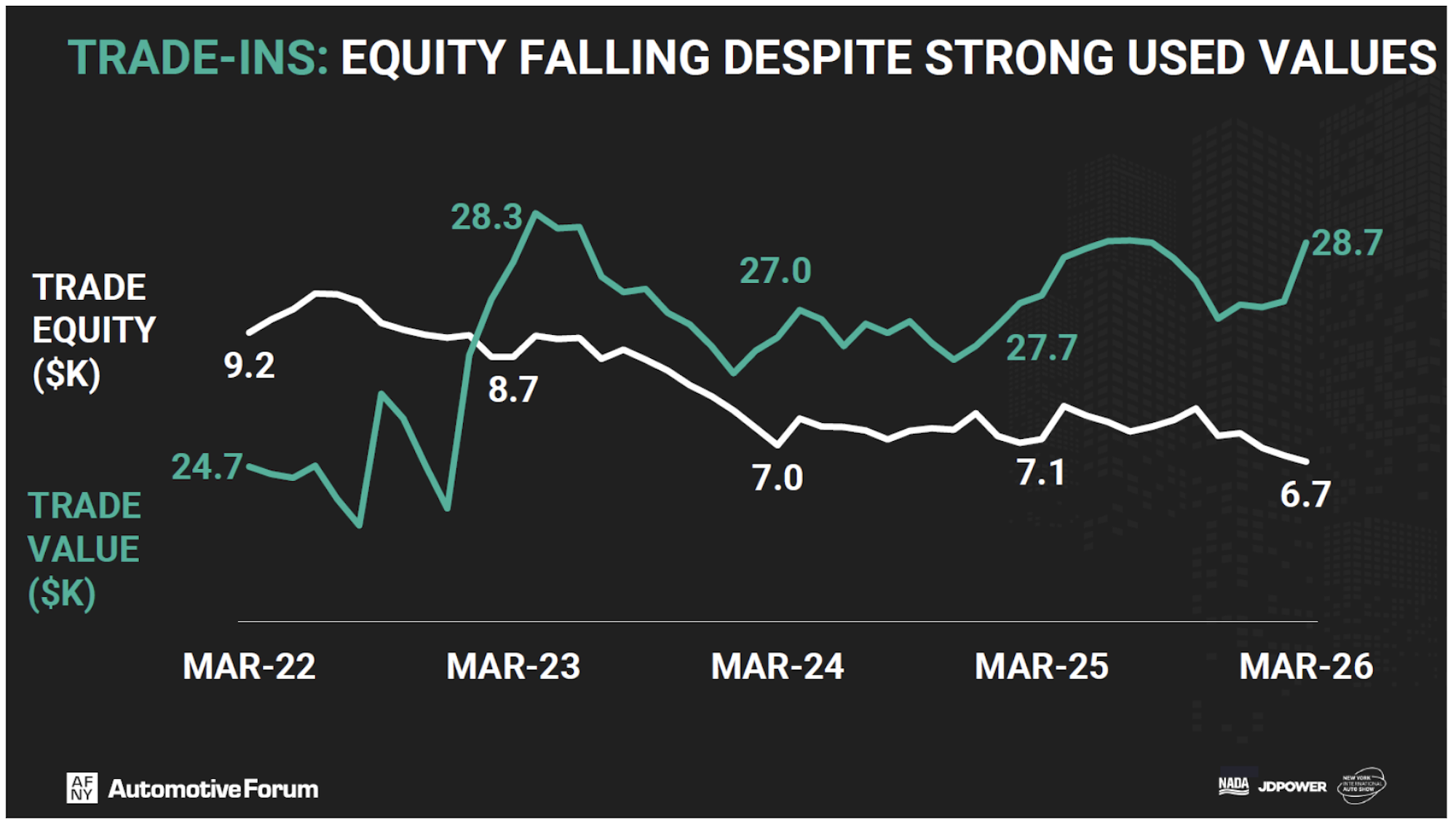

This brings us to how long the normies actually keep their cars. The average trade-in is now just 4.3 years (52 months) old and worth $28,700, meaning buyers are cycling through relatively new vehicles. But the average owner has just $6,700 of equity in said car. That means the typical trade-in customer still owes roughly $22,000 on the car they’re unloading. I physically choked on air when that slide went up.

Affordability Isn’t Equal

The longer loans have another hidden cost in them: interest. A 60-month loan carries an average interest rate of 4.96%. But since the market has aggressively shifted toward longer loans, the 72-month loan comes with a rate of 7.21%. If you pull the emergency lever for an 84-month term, a segment that has nearly doubled since 2019, the rate spikes to 8.53%. You’re essentially paying a 3.5% interest penalty just for the privilege of lower monthly overhead.

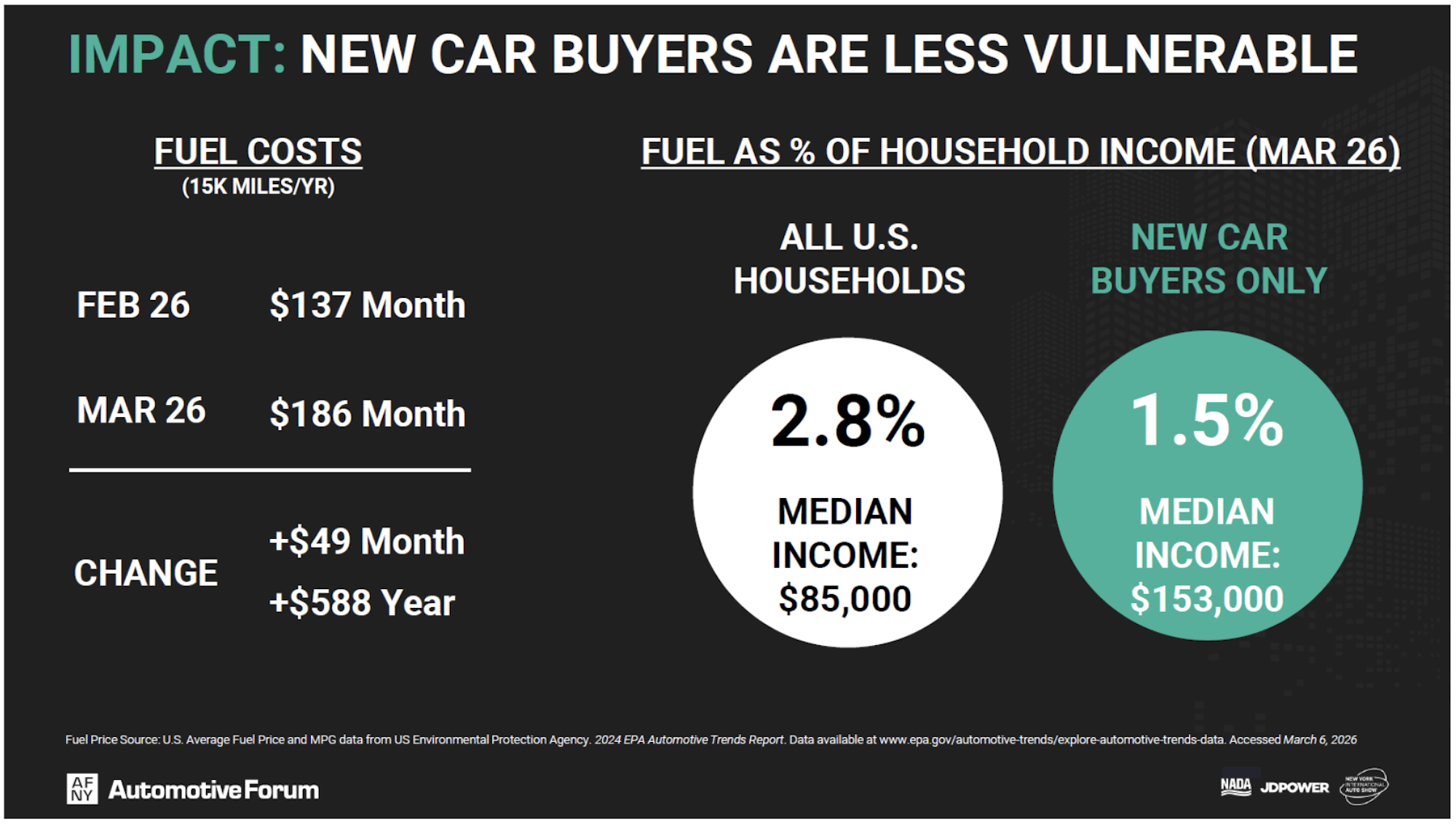

Adding to the affordability factor are fuel costs. Until March of this year, monthly consumer fuel costs, assuming 15,000 miles per year driven, were trending down from the height of $207 per month in 2022 to about $137 per month in 2026. However, that changed with the start of the Iran conflict, which drove fuel costs back up to about $186 per month and climbing. That’s an increase of almost $600 per year.

That number makes more sense as a percentage of income. The median U.S. household earns about $85,000 annually, putting fuel costs at roughly 2.8 percent of income. The median new-car buyer, however, earns approximately $153,000 per year, reducing that burden to about 1.5 percent. In other words, fuel costs matter less to the people buying new cars, which helps explain all the huge SUVs surrounding your rusted Miata at a light.

That stands in contrast to lower-income buyers, and this was a consistent theme throughout the presentations. Job growth and wage growth were described as weak, unemployment among younger workers and minority groups is rising, and disposable income is under pressure. Meanwhile, loan delinquencies continue to climb. For that segment of the market, affordability is starting to look a bit optimistic.

The Silver Lining for Dorks

So, is there any hope for us dorks in this sea of $800 monthly payments?

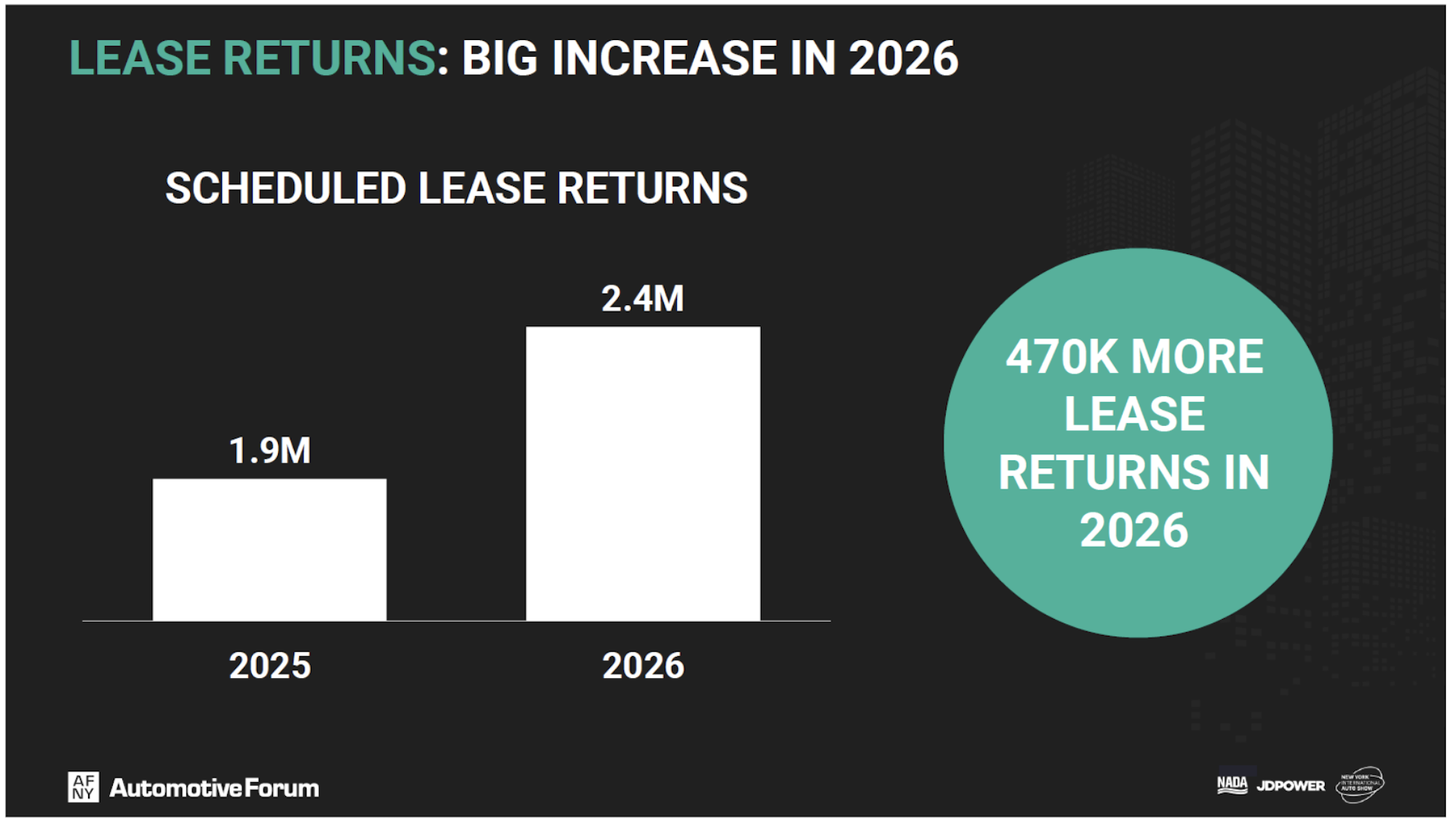

Maybe. Retail inventory has finally stabilized at around 2.2 million units, more than double the lows of 2022. More importantly, roughly 2.4 million vehicles are scheduled to come off lease this year, nearly half a million more than in 2025.

That means a wave of relatively new cars hitting the market. While the normies are busy stretching to make a $46,600 appliance work, that influx of lease returns might finally start putting some downward pressure on used prices.

What “Affordability” Really Means

So, what does all of this mean? For car dorks, the idea of “affordability” has always meant finding something interesting at a price that makes sense. That’s the game. But for most normal buyers, affordability means something else entirely. It means figuring out how to make a $46,000 car fit into a monthly payment, even if it takes seven years and leaves little margin for error.

The reality is that most buyers aren’t really shopping for cars. They’re shopping for monthly payments. The price of the car almost doesn’t matter as long as the number at the bottom works. The algebra is simple. A $50,000 car financed over 36 months at 4.25% is a $1,481 payment. Stretch that to 84 months at 8.53%, and it drops to $793. The buyer “saves” $688 per month today, but in reality, they pay $16,612 in total interest over the life of the loan, compared to just $3,316 for the shorter term.

The system, for better or worse, still works. Cars are still selling, and the numbers still add up on paper. But they only add up because the definition of affordability has been stretched to make them work. The industry will sell this as normal. For the normies making the payments, it should not feel that way.

Top graphic images: DepositPhotos.com; New York Automotive Forum

“The average trade-in is now just 4.3 years (52 months) old and […] the typical trade-in customer still owes roughly $22,000 on the car they’re unloading.”

I’d love more insight into this. I though average car age was going up. This doesn’t directly conflict with that of course, as this is just recent new car buyers. But I find it fucking insane.

Just bought one myself for $5k. I’m letting a friend use it. I don’t have space to keep it, but wanted to get one before the values rise to the point that they become unobtanium. They are very rare. Mine has a manual transmission.

https://i.imgur.com/s01Mgdk.jpg

https://i.imgur.com/tZAdOQI.jpg

https://i.imgur.com/0jlsbZl.jpg

https://i.imgur.com/A8VYJyF.jpg

https://i.imgur.com/Bc667RV.jpg

I might convert it into a diesel or an EV in the long term, yet the short term plan is to purchase a kit to make it it a plug-in hybrid using the stock motor.

My daily will always be my “bicycle”. I hit 70 mph so far and still didn’t top it out yet.

https://i.imgur.com/rwaXmz5.jpg

That’s a lot of work for a pun, and dammit I respect it.

I hope the comment was insightful. If you want something that is legally a car, but possibly the cheapest car to live with on a daily basis, the Insight is the one. 70 mpg driven carefully.

It pays to have a mentality totally opposed to the resource-wasting zeitgeist being imposed. Screw car payments. Screw gas-guzzling, unrepairable, oversized, modern CUVs/SUVs and the massive car payments they come with.

When you pay cash for a car, you’re not paying interest to banks. It’s wonderful.

My Tacoma has been paid off for like 9 years now and I plan to keep it til it dies, and even then I’ll be there with the defib trying to keep it alive.

Big fan of those early Insights in a way I never was for the Prius. Probably the rear wheel skirts, and the fact that it’s so much lesser known than the Toyota.

Also doing 70 on that “bike” sounds… challenging. I ride on two wheels more often than four but even that thing scares me.

The bike is surprisingly stable and controllable. I have gas shocks on each front wheel and another gas shock for the rear end, and the rear end acts as a positrac differential. Silky smooth at speed. Hydraulic disc brake calipers using a mix of motorcycle, ATV, and ebike parts up front, rear wheels being cable pull disc brakes suitable for ebikes, 16×1.5″ DOT rims with solar car tires. It’s enough to panic stop from speed in a shorter distance than most 1990s cars. How safe it feels is very deceptive. If I wreck at 70 mph, I go splat.

I’ve driven cars that were objectively safer, but felt a lot more sketchy at 70 mph.

Just keep after the chassis. All the mechanical stuff is solid on those, but the chassis rotting away is always the achilles heel.

My buddy’s 05 4Runner runs great but is likely going to the boneyard because the chassis is Swiss cheese.

It lived the first 18 years in Florida and it’s what I’d call rust free. Though now that I’m in Denver I have more concern. I bought some salt neutralizer to spray it occasionally.

My car payments are about $50/mo, payable to RockAuto!

For some reason wages have kept up with avacado prices. Seriously in the early 2000’s under a dollar an avacado here was considered a deal, now 33¢ an avacado is a deal.

Yea let’s bring back feudalism! Those peasants have too many rights and cars and food.

There are any number of other political economic arrangements that have, and, importantly, can exist. The fallacy that all historical roads lead inevitably to capitalism is a bell being forever rung by those who benefit from the current system. The fact that capitalism has been uniquely productive, at the cost of workers and the natural environment, does not make it the end of history.

You had me at “The fallacy that all historical roads lead inevitably to capitalism is a bell being forever rung by those who benefit from the current system”. Why give up your place at the top when you can subjugate those below you?

Feudalism can also be somewhat productive at the cost of workers and the natural environment.

Historical roads go in and out of systems constantly nobody said we can’t head back to feudalism or into a free market system.

Items related to this forum – wages have far exceeded the cost of a new car.

As to things needed for life – how about food:

In 1960 17% of a household budget was food. Today it is 10%. The mix has massively changed as well. In 1960 80% of the food budget was spent at the grocery story buying ingredients. Today only 47% of food spending in in a grocery store and the majority is from restaurants.

In the USA we have steadily been increasing what we spend on convenience. We have also been steadily eating more. Today the average adult eats 3,600 calories per day. In 1960 that was 2,900. Today the average child gets 2/3rd of their daily calories from ultraprocessed foods.

I’m often curious what would happen if a developer built houses just like the 1950s subdivisions. Small lots, small square footage, one bathroom, etc. How much cheaper would those be? Would they be discounted enough (if one maintained equal percentage of profit to other subdivisions) to notice? And if so, if they were 25% cheaper than “average” homes, would anyone buy them?

I do not know. I don’t know if the same people crying about how housing is unobtainable would then cry about the “necessary” parts of housing that would cause them to sacrifice, and then refuse to buy them. Or if they would appreciate decontenting the homes until they were affordable to purchase.

People did where I lived in Alabama. Not 3 bed 1 bath but a lot of small 2/2 and 3/2 homes and small lots. Hundreds of houses ranging from 1100 sq ft to about 1600 sq ft.

One example here valued at $220K

9118 Brookline Ln, Helena, AL 35080 | Zillow

I wonder often the same, but I think the town or state would have to be involved somehow. I think the cost of land makes this prohibitive these days. I don’t remember the details, but I recall reading the federal govt actually did something like this at the end of WWII because all the returning GI’s were going to need places to live and start families.

Where I live, every time a small house like that is sold, it is promptly razed with a McMansion popping up in it’s place. Which is sad, becasue a 2 or 3 bed Cape or Ranch style house is pretty much my ideal. I grew up in a 3 bed ranch built circa 1965, though my parent’s added on a 2nd floor in the mid 90’s.

Interestingly enough, that was their 3rd house they owned by the time they a were 35 or so. The first house they bought in 1977 or so when they had just gotten married at 24 years old.

I am significantly older than they were and can’t even come close to even THINKING about buying a home in the same area.

Financial illiteracy is expensive. The focus on monthly payment rather than interest rate and loan duration. The rolling over of negative equity into the next loan. Buying a $46,500 vehicle if you can’t afford. Even at $153,000 per year, a fifty thousand dollar car is often a questionable idea.

Financing for 7 years at 9% interest so you are always underwater on a depreciating asset makes my heart jump. What a stupid way to risk destroying your personal finances.

It’s almost like they purposely don’t teach financial literacy in school.

IMO, people learning what APR is will probably be the biggest solution (among many) to the current tomfoolery that is the car buying market. Although I think most would benefit from more appropriately sized vehicles, simply buying a smaller car (or a lower trim) is basically putting a bandaid on a sucking chest wound when it’s financed at hilarious APR and you end up paying double what the car is worth at the end of the loan.

Don’t fall for the 4 square, look for the total cost at the end of the loan. That or keep acquiring shitboxes 🙂

What’s an aper?

Something that’s embedded into the TruCoat 😛

I looked at Tahoes today for fun. They start at $60K or so, and you can trim and option them up to well over $100K. Not quite double, but an easy 75% increase is possible.

I do all the things this article says car people do.

But I’m most excited to share that I just snagged a running 1989 F150 at auction for $700. And that’s what I look for so I can do what I need to do and not pay $1k a month for a car, which is stupid

Congratulations! I hope it serves your “truck stuff” needs for years to come.

I am going to do all I can to ensure it outlasts me. Good bones to start with.

I imagine the fuel economy will eventually become an issue unless its truly a weekend/occasional hauler.

I have a 2026 Corolla as a daily, so the truck will truly be an occasional joy

but i am not a car dork, i originally came to this site by other means and for other reasons.

it started with the onion newsprint paper in the 90s, following to the website and eventually to AV club in the 00s, then gawker, then jalopnik, and finally here. while i did some minor wrenching when i had ’75 nova in the late 80s. i basically gave up on cars, because i decided my priority was using that money to travel. 40+ countries, 4 continents, and 3+ years total of backpacking. until i finally landed in europe and settled down, got married, and had a kid.

i read this site for several reasons. 1) the writers. 2) the writing. 3) because a lot of the information gathered here is an important facet of what is going on in the world, from a dedicate group of highly specialised people, that gives me a perspective that i would not normally consider.

this article is exactly why i highly value what i get here on this site. thank you for all of your hard work and dedication! 🙂

Funnny, that’s exactly how I wound up here and exactly why I stay as well.

haha, same route here as well.

that….is my path as well

Then please become a paying member so you can continue to read these great articles by great reporters

BUY. A. SMALLER. CAR.

Instructions unclear, now I own a matchbox car on 96 mo loan @15% interest.

Lol, I have a 2016 Mazda6 and most people I know are regularly fascinated at how I “fit my kids in it.” I’m sorry, I didn’t realize I need a damn Suburban for two elementary-aged kids. Sigh, Americans.

Yup, we got funny looks when we unloaded two kids and a bike trailer from a Ford Escort. We did eventually get a Mazda5 but as empty nesters we have downsized to a Fiat 500, paid for with literal cash.

I also have a Mazda5 and I amaze people by telling them I can fit a week’s worth of groceries in the cargo zone, including eggs and veggies with all the seats up.

Oh and it also does light truck stuff.

With my little trailer and my Mazda5 I’ve hauled loose mulch and soil, furniture, stuff for a dump run, new appliances, facebook marketplace finds of all kinds (vanities, a trampoline, etc), and regularly haul all the camping gear plus bikes, kayaks, and canoe while comfortably seating my two kids and 70lb lab.

I love it dearly. In sad recent news, we’ve been lending it to a friend for a while and have decided to let her buy it from us to avoid getting a car payment, and we found an incredible deal (more than 10k off book!) on a hybrid highlander with some cosmetic damage that will be easily fixed. I purchased it over the weekend and got 37mpg on the 4.5 hour drive home through the mountains.

Nice!

Bluntly, whatever. These articles act like inflation isn’t a thing. Dollars are smaller now, it takes more of them to buy stuff. Dollars were smaller in 2019 than they were in 1989 too. Wages ARE up – and nobody holds a gun to your head to buy the median priced car, which is well skewed by the millions of ludicrously priced pickup trucks idiots feel they “need”. I bought my mother a $20k base + Tech Pkg KIA Soul a few years ago that other than having cloth manual seats is notably more luxurious than the $20K Olds 98 Pregnancy my grandfather bought in 1984. Faster too, and a hell of a lot both safer and more reliable and efficient. If people want to spend a bunch on interest to have champagne taste on beer budgets, more power to them. There are still a BUNCH of cars under $30K that are way more than adequate transportation. And $25K for a used car gets you things that are actually nice.

$1000/mo is what it takes to pay off a $50K car in a reasonable amount of time with a decent down payment. BTDT would do it again if there was anything I actually wanted to buy in the sea of dreck that is the 2026 new car market. I really should thank the automakers for saving me from myself, I guess.

Finally. Dollars are smaller. We the (common) People, don’t have the same leverage we used to. You know the reasons.

Dollars are always getting smaller. Have since the dollar was invented. What did it take to buy a loaf of bread in 1776? $.01? We had a LOOONG period of very low inflation, and then a period of VERY high inflation for various reasons, and are back to a moderate rate of inflation (that is being artificially increased by the idiocy of a single man in power currently). On the bright side, wages have outpaced inflation for the past 5+ years finally with some real gains there – especially at the bottom of the labor market that really needs it.

Ultimately, some inflation can be a good thing. It allows leveraging debt. You pay the debt back with smaller dollars vs. paying for something completely up front.

I think you missed the intent and point of the mention of the ‘smaller dollars’. It’s not an issue of inflation or anything else but the fact that an increasingly smaller percentage of the population is amassing most of the wealth, leaving the rest of us with ‘small dollars’.

Thank you. This is the real issue.

Yet 95% of the population has seen their inflation adjusted income increase. The bottom 1/3 have seen gains almost as high as the top 3rd.

In real terms almost everyone in the USA is doing better than in the past. No, the gains are not evenly distributed but since when is personally doing better not enough anymore?

The poor have always vastly outnumbered the wealthy, and the wealthy have always had the majority of the wealth. The US went through a *short* period post WWII where the middle class did far better than before or since. Those days are long gone and probably not coming back – at least not absent a second American Revolution (which I would support, to be honest). Elon Musk being the richest man in the world doesn’t actually affect you much (other than his political influence, which is not relevant here).

And let’s face it, in America often being “poor” means you can only afford a 55″ TV. Or a, perish the thought, *used* car.

The next administration must let in cheap Chinese EV’s. I perceive this will be an economic mandate as things have gotten really out of control and zero progress has been made on mass transit in America. This will be a painful period for American manufacturers who are stuck in legacy approaches, as well as American workers. However, it was predictable. May our leaders of tomorrow possess great wisdom in lessening the pain.

I’ll continue to buy used, branded-title vehicles and have enriching adventures bringing them back to life and reliability. I realize it’s an unusual privilege to have cash (even a small amount), physical function, time, and garage space to do so. I mourn for the disadvantaged and oppressed in these times – give and help your neighbors and kin generously.

“May our leaders of tomorrow possess great wisdom”

Um, yeah… I wish us all good luck with that.

Not to get too political about it, but we should probably hope for voters of the future to possess said wisdom. So many of us vote against our own self interests because we buy into the marking hype put out by “our” party and don’t evaluate the people we put into office by their actual performance.

What they promise is far removed from what they deliver, and yet all we pay attention to is the messaging and keep putting them back into office over and over again, and wonder why it never gets better.

I’m convinced the Founders made a mistake. Competency tests for the right to vote should be enacted. Too many stupid people flatly believing what they were told and how to vote without looking at the facts.

Technically they kind of did this (although the true intent can be debated). Originally, only land owners could vote. There are exceptions but land owners were generally more educated and thus able to make better decisions on politicians.

The Founders dealt with the “competency” issue by restricting the vote to those who were male, white, and landowners. That encouraged a certain uniformity of opinion.

If the Chinese automakers committed to donating just $50 per unit sold to the next presidential “library”, they could be setting up showrooms here next week.

I shutter to imagine a Trump library. Shelf upon shelf of gold leaf comic books probably.

Don’t forget the NFT gallery.

Pretty sure the building will be a gold pyramid too.

And you don’t see the similarities between that and the Chinese? Someone is going all off.

Nah, looking at the resistance to releasing the Epstein files, it’s gotta be kiddy porn.

What do you think is in those comic books?

I don’t feel bad about any of this.

There is absolutely NO reason to ruin yourself financially for transportation. Zero. The media loves to keep on talking about “the average price of a new car” blah, blah, blah. No one is forcing you to spend that much. There are great options for as low as mid-20s for new and if you buy used you can still get a great car with low miles for $10k.

I’ve helped a few people shop at the $10k price point over the last few years and found the selection reduced to very high mileage and/or rebuilt crashed cars. Sometimes with a rebuilt title, sometimes without and you just have to do some detective work.

I do agree that it is possible to own cheap, reliable transportation, but for a normie who lives in fear of a mechanical failure, it’s a lot harder. Turbochargers have SERIOUSLY proliferated in the 10ish year old selection and they all seem to be leaking oil (into the intercooler) at catastrophic rates.

You can fix a LOT of problems with the difference between a $10- $20K used car and that near $50K average new car price. I see no reason for the normies to not just get the best Corolla or Camry $20K will get them and drive off into the sunset. Other than they all want to sit up high in stupid CUVs on the same platforms that cost more.

Sure you can, but I’m not talking about people who have $20k to blow on a car, I’m talking about people for whom $10k took a long time to save, and don’t have $4k more for a turbo replacement. Ask anyone unlucky enough not to have bought a home and locked in a mortgage by 2023 how easy $20k is to come by.

Then take the time to find a minty example of an even older and simpler car. They are out there. I bought my mother a 40K mile V6 ’01 Camry in 2019 for $3500. Sadly drowned by a hurricane or I have no doubt it would have been her last car ever. Even at double or triple that price that is a heck of a deal. But you have to search for them.

I have my standard advice for people whining about house prices – move somewhere you can afford.

I actually almost did that, but it invariably meant pushing mileage up into the 200k range. That was a good find in 2019, but I think it would not have gone that way if you tried to do it in 2024, and taking 4 days off work to fly across the country and drive a car that you just bought sight unseen home is something you do for a unicorn, not a commuter.

This was a couple of years back the last time I did it, and based on the avalanche of replies implying I’m a moron, it’s probably not as bad now.

“You can fix a LOT of problems with the difference between a $10- $20K used car”

Or push them in the direction of a more basic $10K car… like a used Corolla, Prius, Civic, etc.

Hell… for someone who is single and just needs a cheap, reliable commuter car, the Mitsu Mirage won’t be fancy, but they’re cheap to buy and cheap to operate and for $10K, you definitely can get a low mileage example.

In my observation though, many people want vehicle with “the right image”… and then make the mistake of doing something like buying “a cheap BMW/Mercedes/Audi”.

I’ve known people who did that and didn’t listen to me when I tried talking them out of a bad decision like that… and I watched how it bit them in the ass later.

Yup – as I just replied to another poster. If you have no time, not much money, and just need reliable transportation, lease the cheapest thing you can find over and over. Play your cards right and you won’t even ever have to buy a set of tires. But it has to be CHEAP. “Car as utility payment”.

I personally think the Mirage is not enough cheaper than much, much better cars. They really are complete and utter crapcans. I’ll take a used Corolla or Camry for the same money any day. Also the issue that Mitsubishi dealerships are thin on the ground these days – Toyota service is available everywhere if you should need it.

Cheap Euro cars are only good value if you can mostly wrench on them yourself. BTDT for decades. You can have a great experience on the cheap. But I would never recommend that to anyone who has to depend on a shop, especially at today’s labor rates. You also have to know what to buy and what to avoid.

Plenty of Chevy Malibus with less than 100K miles for less than 10K.

Just one example: one owner, no accidents, 92K miles, NA engine with a 6 speed conventional auto in a mid trim level for $7500. Not even black, white or grey.

https://www.cargurus.com/details/440438216?resultSetId=c30d18f2-0929-4616-b43a-7c178e0eee52&searchUuid=ca3ed338-dcba-4ea3-9419-5ae82709d517&sourceContext=carGurusHomePageModel&sponsoredType=NONE&srpVariation=DEFAULT_SEARCH&listingIndex=14&inclusionType=DEFAULT&searchZip=97124&searchDistance=50000&ourls=SRP&srpc=N4IghgZgxiBcoC8CWAHOICcB2AjAJgBYQAaEAWzAGsBTAWQHsATagGwBUAnJMgBTABcAFgGc4AbXI4A9IwBsePCUky8AZjw4lZaXLUgAuqSTCAIqyQA3ahwCeAUQB2YAEYtqjOBDAth1Uii4oahMOehRhAHkHFhtPb19SQSRmADkBJHoHAHdk6gBlJJQUJAcAczh+DgBXPxBGY34wByC4AFYABk720gdMgtQUFzcAITBfFhLqOAAOAlJheg5+EyQOaih+DId0AEE8gGElBaW2GxQp2BBhuzy2AH1aHbZ9gAktMAAPWiQ3MFKLnBdTqkCgfHiBAFA0hWJJQNwvBqLGwRFCbTKiWASFIRFJ3PI7AAyADUdgBxOxKAl2Wg4u4AMQASnYKaRsXc2C87HT7i8AJK3CIMgCaSgAqikTDtHuSTPSGVKWSB9lSdri2Ly2FSDPMOCgiWAuOlMugTFydqKCfc8nYdgzXiAAL6kDYfOCgCYeWAEAjtAiqaYaWT+cqwHDzKpVZLoKBgVTuVT+gC0jCgzjAiYI1FjiYwBBwGETrTA1ADWHaGEYrRwWCOHCgLujBtJVWqwhe9DI1D4-wYzBYShQpTA6GoNgAUhQABpjhCMOnDQQALTwoqQEQAVnYCAT9mOskKAOqMdhIXmyWjrscYR0OoA

Speaking of Malibus – there is actually a mint condition Malibu Maxx of all things sitting with a for sale sign on it near me right now. No idea what they want for it, but I can’t even remember the last time I saw one of those rare Malibu hatchbacks. Looked super nice driving by, certainly a Grampy’s last ride as are so common down here. I have to go that way later, I should stop and check it out.

I had lots of that generation of Malibu you posted as rentals. Not a bad car at all.

Tell those people to stop paying the Toyota tax, the SUV tax, and the Luxury car tax, and they’ll get a lot more hits in their searches.

I just went to auto tempest to see what’s around. 10 to 12k. Limited it to sedans, not SUVs or crossovers and scrolled past any luxury makes. And people need to get over their hang up of that “magical” 100,000 mile number. Things don’t automatically fall apart when a car passes that milestone. It is just another service interval (which might include a timing belt).

There are indeed lots of options.

2015 Mazda 6i sport $12k 86k miles

2015 Ford Taurus SEL $11k 85k miles

2016 Chevy Cruze LT $11k 80k miles

2016 Chevy Malibu 1LT $10k 82k miles

And the list goes on and on.

We don’t have a shortage of decent cars to buy in that price range.

We have drivers who think they are too good to be driving around a “regular” car. They think they are entitled to crossovers because they are trendy. Or they think they “need” a Toyota because our shitty automotive press has brainwashed people into thinking only Toyotas are reliable. Or worse of all, they think they are ballers who should be behind some shitty German brand. All those criteria add thousands to the price of a car, which means you would indeed be over that $10k threshold. Take those things away and you can indeed find cars for around $10k.

You’re assuming a lot, but these are better options then were available when I last went though this song and dance 2ish years ago – perhaps a sign of the changing economic landscape. Best I found for this family member then was a 2017 Cruze hatch with about that mileage and repaired front end crash damage for $10k. Only constraint from her was it had to have a hatch, and I excluded CVTs.

Now I’m getting ready to put a turbo in it.

There is a night and day difference in the used car market between today and 2-3 years ago. New car shortages in 2020-2021 did crazy things to the used car market. That is returning to normal as shown in the lease return data in this article.

“I’ve helped a few people shop at the $10k price point over the last few years and found the selection reduced to very high mileage and/or rebuilt crashed cars”

For $10K, you absolutely can find good used cars that have low mileage… such as used Corollas, used Priuses, used Civics, etc

But I’m gonna guess that at least in some cases, the people in question insist that they “need” a larger 7 seat SUV from a luxury brand and/or loaded with luxury features they “need” so they can “safely” ferry around their 1 or 2 kids, right? Or they “can’t live without” heated seats or carplay… even though they survived just fine with vehicles in the past that didn’t have that, right?

So the real issue is many people have trouble separating their needs from their wants.

I’ve personally encountered this more than a few times when helping people buy vehicles. In one case, the wife wanted a “full size SUV” because “they needed more space”. I told them that if it’s space they need, then it’s a minivan that they should get.

And I showed the actual interior space data that showed the minivans from Honda, Kia, Toyota and Chrysler cost less and had way more space than the SUV the wife wanted.

And since the husband was a practical person, they ended up with the minivan rather than an overpriced status-mobile SUV to satisfy the wife’s false “needs”.

“Turbochargers have SERIOUSLY proliferated in the 10ish year old selection and they all seem to be leaking oil (into the intercooler) at catastrophic rates.”

Yeah and at the same time, it’s easy to steer people away from these turbocharged vehicles that don’t hold up well (not to mention regular CVT transmissions) by simply steering them in the direction of a hybrid or a BEV.

I generally buy new cars, because I keep them for a very long time and like to know I’m not buying someone else’s problems. But I honestly don’t think I’ll ever be able to afford a new car again. My pay hasn’t even tried to keep up with inflation.

And what are you doing about that other than complaining or resigning yourself to accepting the situation? Looking for a higher paying job? Taking some classes? Doing anything at all to improve your employability/value to your employer? Heck, I effectively gave myself a $12K a year raise by moving to a state with no state income tax a decade ago.

Wow, that’s a lot of assumptions. Maybe try to not victim blame or act like you know someone else’s situation or that your experience translates universally to everyone else? You can do better than that.

Victim? I think not. Or being a “victim” is a big part of the problem. You are only a victim if you let yourself be one.

You can call it victim blaming if you want but only you can change your future. We can talk all day about how things could be changed to make the economy more equitable but the reality is that every one of us has to live in the world as it is today.

If you don’t like your current economic reality make a plan to change it and then work that plan. It might sound harsh but the world is harsh.

The place where I can see the payment “making sense” if bought responsibly, is if you seriously — and I mean seriously — are buying something for the truly long haul.

”That’s it. This is the family car for the next 15-20 years. For real.”

If you buy correctly… modern cars will absolutely do that. No problem. You take care of it, and it takes care of you. Even 20-30 year old vehicles did that extremely well so long as they were taken care of, and they’ll go longer without major surprises if you didn’t can-kick. I live in New England where rust is real, but meticulous folks kept their un-garaged NPC-mobiles in good shape for 200K+ miles by putting in the effort.

Outside of that? I drive actual crazy, and I’d never consider $1000+/mo on anything. Ever. Heck, before the recent crazy my highest ever payment was still under $400 a month and that was a new, custom ordered 2016 Porsche Boxster Spyder!

Unless that was a really good lease deal, the math isn’t mathing on that Porsche unless you had a really, really long loan or put a WHOLE bunch of money down. I mean, I only had a $400 payment on my Mercedes for four years, but that’s because I put more than half the price of it down. Would have paid cash but I needed to put a roof on my house thanks to a hurricane, and hadn’t gotten the insurance money yet.

> of put a WHOLE bunch of money down.

Ding ding ding! I borrowed $21,600. $80Kish down at the time.

Financed what someone might for a stripped 4-cylinder Toyota Camry.

Did the same last year with my Spyder RS. I basically financed the equivalent of a nice Toyota Highlander, and still paid it off in 14.5 months.

EDIT: FYI, there is also no such thing as a “really good deal” on any Motorsport division Porsche. You PAY. There are no incentives, and usually hefty ADMs.

It’s bit disingenuous to be comparing payments when one is putting half down without mentioning that fact. Being able to do that is the definition of privilege after all, especially for what is basically a toy car. I paid cash for my BMW convertible… I could have used that money to put half down on a new one, but I don’t like the new ones. And mine has not depreciated a penny in the six years I have owned it.

There are no deals on Porsches period, and IMHO their prices have gone even more plaid than most. I had the purchase of a new, quite lightly optioned, Cayman for European Delivery negotiated for my 50th birthday present to myself. My Inner Yankee Cheapskate scuttled the deal. I just couldn’t come to grips with nearly $80K once the government was paid for that car. But hey, at least by then Porsche wasn’t charging *extra* to pick it up at the factory as they used to. Bought a leftover Fiata instead for 1/3rd the price that was 1/3rd off MSRP. Much better, even if I ended up getting rid of it in a couple years because it was a bit to painful to wear. I missed my mark by a couple of years with buying a new Cayman, should have sucked it up and ordered one of the last base cars with a six.

And now, thanks to Trumple Thinskin, you can’t realistically buy 25yo used cars from Europe either. I have a friend in The Netherlands who owns a shop who would cheerfully help me find something fun, but the tariffs make it just plain stupid at this point.

It’s not disingenuous. It’s a reminder that there’s another way make such a large purchase. Cars are generally the 2nd most expensive purchase a given household makes outside of a home, and the issue is too many normalize being flippant and impulsive about it, where people go up to their neck in debt obligations.

I didn’t have a $398/mo payment for 60 mo on a desirable Porsche because I was clever, or only knew some trick told to me by one of the four most recent dead archdukes of the Holy Roman Empire.

I did it because I planned ahead, had no intent on ever having a monthly payment inline with my Boston rent, and saved while still being responsible on every other front. I realized that so long as I kept building the pile, I’d get there in time to order one exactly as I wanted mine to be, to the last detail.. So I did.

I didn’t decide to YOLO buy a Spyder RS. I realized years in advance that it was going to exist, and that I wanted one. I made a plan, and immediately cut every other non-essential expense (save retirement) to shovel money into savings as hard as I could. I even took on an additional after-hours role so I could have a bigger shovel. And I bought it with a payment around what most people would have for a loaded Toyota Highlander, securing my own financing for the lowest rate for 60mo in the country, instead of having a car payment substantially higher than a Boston mortgage. Then I paid it down in 1/4 the term length so it would. Be. MINE.

Sorry for trying to remind the world there’s another way to do things.

That’s all fine and good. But just “reminding that there is another way to do it” is not actually what you did. You spit out with a major flex that you “only had a $400 payment on a Porsche”. Had you explained how you got there, then GREAT. But you didn’t do that. So good for you that you were able to do these things and buy your dream car, but it’s pretty irrelevant to most people’s experience of life. I mean I could have spent the $200K or so in cash I have put towards my new house on a Ferrari or something instead too. I like cars, but I try not to be stupid about them to that extent. But as the kids say – “you do you”.

I don’t think anyone here doesn’t know that you can just save up money and pay cash in whole or in part for a car. And as I have said here many times – debt in and of itself, is neither good nor bad. It’s just a tool in the financial toolbox that can be used or abused.

Wow, this is all so absurd to me. I know this is nothing new, but these “normal” people are not normal, they are idiots. It’s kinda like common sense doesn’t exist anymore, since sense is not common anymore. My cheapest shitbox was $100 TOTAL.

“$16,612 in total interest over the life of the loan”

Wow, I think that’s about what I’ve spent to buy all the cars I’ve owned in 25 years!

“stretching to make a $46,600 appliance work”

Wow, I can only daydream about all the rusty shitboxes I could buy for that! Since I especially don’t want a new appliance car, ha ha

Most people really have no interest (or ability) in owning rusty shitboxes. I have the ability, BTDT, but not even remotely the interest. Or any reason to at this stage in life when I can afford mint examples of interesting cars.

Exactly. What’s the single mom with 2-3 kids and an apartment going to do when her shitbox needs repairs every weekend but the kids have to be at school on Monday and she has to be at work? And public transport inevitably sucks? It does not compute.

Exactly!

If all you need is basic transportation and no drama, I am a big fan of “car as utility payment”. Lease the absolute cheapest thing that can get you by. As I have said here before, a succession of cheap VW Jetta leases got my bestie through nursing school while also working a full time job. She had NO time for car drama, and none of the Jettas gave her any for about $200/mo. Didn’t even have to buy a set of tires for them, other than the set of mounted snows she bought for the first one and kept through two more. $200/mo isn’t THAT cheap compared to just buying a used one and keeping it for a decade, but no surprises has real value when your time is very expensive.

And this is also why this last time around I bought my mother a new base KIA Soul rather than finding her another low miles used Camry for cheap. Because when anything at all goes wrong, it’s *KIA’s* problem for the five years of the B2B warranty, not MY problem. I still get the call, but I tell her to just go to the dealership. Priceless.

This is leaving out that the typical household does not buy a new car. In 2025 when a person needed a car 70% of the time they bought a used one.

Yeah, that is the very terrifying reality.

People aren’t just signing up for their terms on a new F-150.

They’re also signing up for these terms on a few year old Dodge Durango.

If that is the case they are overextending themselves and need to stop shopping expensive and gas guzzling SUVs. Maybe a few year old Chevy Spark or Mitsubishi Mirage in more in the budget.

>… need to stop shipping expensive and…

And they’d tell you to get your logic and reason the eff out.

Which is fine but they shouldn’t expect any sympathy from me when they complain about being broke and living paycheck to paycheck.

Similar to how my coworkers get no sympathy when they complain that they will never be able to afford a house but refuse to do an internal transfer within our company to a location where they could easily afford to buy a house.

We all make choices in life.

Moving to a state with no state income tax and a rather lower overall cost of living was the best financial decision I ever made in my adult life. I bought a lovely house for $90K less than ten years ago, and paid it off in three years even though I basically did it on a whim with zero preparation. It’s worth $200Kish today, which is still VERY affordable. And with two lodgers in my place in Maine year round, that place has nice cash flow and allows deducting a lot of the expense of it.

Ultimately, infinitely more people are house poor than car poor. Though the real fools are BOTH.

We are all the ones picking up the tab for their bad decisions in one way or another. That’s the part I’m not happy with.

When the head of the household runs up as much debt as they can against an overstated or temporary income, the family still needs to be housed and fed. If they can’t pay the bills, eventually they’re on public assistance to fill in the gaps.

Not a great situation for anyone, and I’d be happier if there were less misery and public expense even if it means that SuperSubprimeLenders.offshore doesn’t get to run a Superbowl ad.

Yes, we collectively pay a sliver of that excessive spending through public assistance but all public assistance is a small slice of public spending.

SNAP, TANF, housing assistance… all the public support programs that people love to complain about are less than 8% of the federal budget.

People over extending themself are mostly just screwing themselves by sending an ever increasing percentage of their income to creditors. Most loans do not default – even subprime ones.

Not all loans need to default to cause a crash.

Over-extended people are only screwing themselves until, of course, there are enough over-extended people to screw us all.

Didn’t we end up paying almost a trillion dollars in corporate welfare the last time this happened the exact same way less than a drinking age ago?

No, we didn’t pay almost a trillion to bail out banks back in 2008 – 2010. Congress authorized up to $700 billion in loans through TARP. That money was loaned not given to banks and was paid back with interest. The maximum borrowed amount was $430 billion. Between the interest earned and money lost by loan defaults TARP ended up costing US taxpayers $32 billion. Like the auto bailout the cost of bank bailouts was wildly exaggerated and the cost of doing nothing would have been huge.

That said, what is your alternative? We ban subprime loans? Ban car loans over X number of months? 1/3rd of US adults have a subprime credit score.

“It’s basically impossible to fit rear facing car seats in a Corolla though.”

My response to that would be “Sure… no prob. But mark my words… The Dildo of Financial Consequences WILL be paying you a visit if you buy that high-TCO SUV.”

A lot of the cars coming off-lease will be EVs.

I am making assumptions here, but I would say that the lower end of the income spectrum is less likely to have provisions for home charging.

How can we ever again expect lenders to act responsibly when we have established that they will never bear the consequences?

The next time we see this report, it will be 12% 96+ month loans.

It’s intentional, at the school district I worked at our state removed all financial literacy standards from math classes. And they ruined the science standards too.

And this was over 10 years ago, after the pandemic I heard they were taking teachers out of the curriculum and using generic curriculum for everyone at a cost of $130 million. It’s only going to get worse.

Dorks!?! Abby Normal is preferred. A good percentage of the readership enjoys having the interest, knowledge, tools, and skill to do their own maintenance and repair. There are many rational reasons to buy a new car, or lease if you can write it off as a biz expense. I have never had the need, nor desire to buy new, knowing how much more that amount could purchase used.

It is understandable that many need reliable, presentable transport for work, and may not have the housing arrangement to allow working on a car. I don’t understand purchasing something with predatory terms. Your average Joe sees my 16yo MB with shiny paint, near mint condition, and thinks it is much newer, and certainly not purchased for less than half of the cheapest econobox.

Meh. I loved buying new cars once I could afford what I liked new. Especially my pair of special-ordered European Delivery BMWs. Fabulous having it YOUR way, and not somebody else’s sloppy seconds. But I had reached a point in life where I could afford it, especially for the second one, a completely unneeded other than I wanted it M235i that was the 4th car in the garage. Took my mother to Europe for a month to get it, trip of a lifetime for her. I freely admit the first one was a stretch at the time, but I still have it and it’s been paid for 12+ years now.

Used cars are better value in SOME ways, but not ALL ways. Certainly the best money I ever spent on a car was my first new BMW in 2011, which I still have and love. And at the time, it was not realistically possible to buy one used, I tried for years. RWD, 6spd, wagons were rather thin on the ground, and not enough cheaper than a new one once the discounts were factored in. And I travel effectively for free.

I also have an aging used Mercedes these days, but that is mostly simply because I liked the S212 better than what they were flogging new at the time – the idiotic All Terrain. If they hadn’t stopped making not-Outbacked new ones, I probably would have ordered a new one and done another Euro Delivery. Similarly, I bought my minty 128i convertible six years ago because I couldn’t get a stick in a new 2-series (and BMW killed Euro Delivery, as has Mercedes now I believe). If I can’t get exactly what I want new, why pay the premium? But if I could, I would.

That’s all great, a rare in U.S. stick shift sporty wagon in your choice of trim is a great example. Your career path used to be more normal, where if you’re doing a competent job, you could more or less count on it continuing, and came with pension, health care, and 401k matching. That is rare currently. I have worked my way up to comfortable conditions three times, only to have it disappear with arbitrary ownership, or corporate structure change. Lean times between have taught me to never over extend, and only purchase cash. I told a wealthy friend that always had a new Aston Martin, that he should look into getting a Ford GT back in 2003, as I was sure they would appreciate, but it was out of my reach.

I have found the trick is don’t work for a publicly traded corporation. I work for a private partnership (second time actually, first prof job was for big corp and I learned that lesson fast) that actually cares about their employees as more than just a headcount to be rationalized. No pension, but generous compensation makes up for it. Other than the ludicrousness that is health insurance, I could retire any time I want at this point. So even losing this job wouldn’t be the end of the world. But that is the perspective of a guy in his mid 50s who’s single, no kids and actually lives pretty frugally. Other than my current madness of building a new house. In 20:20 hindsight, probably a huge mistake – I really should have just built a garage/workshop., But it just means I need to sell one or the other of my current houses when it’s done. Just need to decide whether I am really done with going to Maine summers, or if I’d rather keep my current Florida house as a rental or sell it. Or sell both, be debt free again with a nice chunk of change leftover. It sucks that I am pissing away $2500/mo in interest currently, but ultimately it doesn’t really matter, and if I lost my job the rental income from my other properties covers it and my basic living expenses anyway. I just wouldn’t be able to pay it off until I got a new job or sold them.

I certainly agree about not overextending yourself. I won’t owe money on a car out of warranty (as a general rule), and I have long used the “pay yourself first” method – I put a big chunk of my salary into savings and live off the remainder, including buying cars. And houses for that matter. And other than the couple I didn’t keep long enough, I have paid off every new car I have bought new in less than three years anyway. But unless the industry takes a big step back, those days are deader than Elvis.

Not knowing where your new house is being built, I don’t know what your property tax situation is. That is what put me off of newer construction in my area. Sounds like you have done well, and should be able to retire well whenever you want. I gave up the rat race more than ten years ago to be a caregiver for my parents after my dad could no longer drive to chemo/radiation treatments. He passed in 2018, Mom just six months ago. I’m the youngest sibling at 62 and lived a pretty free wheeling good time life other than people dying on me. My eldest brother 74, still thinks I’m in my 20’s and talked me into taking down three dead trees on his property two days ago. 3&1/2′ to 4&1/2 ‘ diameter trunks, 30′ to 45′ tall. I still have all the equipment from my 20’s after my first career sidetrack, and had done a 75’ tree for him a dozen years ago. After they were all down, and started to be cleaned up, 5hrs. had passed, and I was shot. Still feeling it slightly from rarely used muscles. Live Large while you’re healthy!

SW FL. Taxes here are reasonable, with little difference between new or used houses. It’s all market-based and everything is revalued annually. Taxes have fallen right along with values. And if you are homesteaded, they can only go up a small amount annually anyway, and you get $50K off the top of the valuation. But the time and hassle and aggravation of building a new custom home SUCKS, nevermind that I will be underwater on the value of this house for a LONG time vs. what it is costing with all the cost overrruns. If I knew then what I know now, I would not have done it in hindsight.

My mother did what you are doing for my grandparents. She was their live-in caregiver for 16 years, which let them age and die in their own home. The last few years as her full-time job, and it was a job as my grandmother had dementia. Not fun, and a huge amount of respect for anyone who takes on that role for elderly folks, relatives or not. My grandfather was sharp as a tack until the last month of his life – he died of stomach cancer, and was pretty health for being in his 90s until that. Mercifully, my grandmother passed just a couple months later, as she was about to the point where my mother couldn’t handle her anymore and was looking at nursing homes. She was the mean sort of dementia patient, not the happy la-la kind like HER mother was. My great-grandmother was like a happy 5yo the last few years of her life, my grandmother not at all, especially towards my mother…

Definitely feeling you on the getting old and using unused muscles – I’m 57. I spent today putting in blocking for the kitchen cabinets in the new house, and I am definitely going to feel this tomorrow. And I have a bunch more to do tomorrow, and even worse, the rest of it means getting on and off an 18″ step-platform to do it. I quit for today so I can get a helper for tomorrow to minimize how often I have to get up and down off that platform. I am installing the kitchen myself – my third IKEA kitchen. Also doing the bathroom vanities and whatnot. Saved a small fortune vs. what the contractor wanted, and a much better end product. Sweat equity, LOL.

Their chart “Payment shock: Lower for lessees” (under your subtitle, “Normie Affordability”) is a BS move by them because they used misleading conclusion bubbles at the right of the chart to iimproperly emphasize their point.

What they present is:

Finance payments: +$125 vs. 2022

Lease payments: +$14 vs. 2023

which appears to be a $111 difference in increase if you don’t read the smaller print.

That is an invalid comparison of different time periods, which one can assume is meant to exaggerate.

The valid statement pairs would be either

Finance payments: +$125 vs. 2022

Lease payments: +$84 vs. 2022

which is a $41 difference in increase,

or

Finance payments: +$46 vs. 2023

Lease payments: +$14 vs. 2023

which is a $32 difference in increase.

Wouldn’t percentage differences be the real point of comparison?

Financing went up about 18.5%, leasing went up 14.8% or so. Not a huge difference but a noticeable one.

Time period makes a difference too. By comparing sales to 2022 and leases to 2023, they present a year less inflation for leases compared to financing. But, if the time periods were equal, yes, percentage would be a better comparison.

Not just a year less inflation, but they excluded THE year for inflation, especially in autos. For this reason alone, I’d dismiss everything this outfit puts out.

This is not analysis, this is influence.

I didn’t look at the particular years, but, yeah, that would seem to suggest intent.

It’s that bad. In 2022, new cars inflated 10.4%. More than the cumulative inflation for all years since.

Weird how the author did not mention that, you would think that was their job.

Quite true. They left out THE main year of increase.

I think one of the difficult things for me to wrap my head around is how car prices are one of the few things that cost the same everywhere in the country. It make the discussion on what people think “affordability” means really complicated.

The new-car buyers earning a mean of $153k hits different here… in my county that’s the cut line for “low income” for a household of 4.

And most of these people agreeing to these outrageous payments are not car people and are buying boring shit they don’t enjoy. It’s mind boggling.

If they were aiming for boring shit most of them would find something for less than $45k.

Keeping up with the Joneses is a thing. Not a good thing but a thing.

Keeping up with the Joneses doesn’t have anything to do with the car being interesting, it merely requires a badge that people equate to being expensive. A Mercedes SUV is just as boring as a RAV4 and that’s the kind of stuff most people are paying all this money for. Even Lamborghini’s biggest seller is a marked up Audi SUV in RAV4-ish clothing. People who are overpaying to keep up with the Joneses might be sort of enjoying imagining the neighbors are impressed (they’re not), but other than that, they’re not enjoying the vehicle for its qualities. I’d say most of them aren’t even getting that kind of dubious joy, they’re just following what they’re expected to do and if they live where the neighbors spend that much on a premium brand vehicle, they feel they need to do the same to fit in. Why not just get a CRV? What would the neighbors think? How would we look picking up the kids from dance classes? Personally, I couldn’t fathom caring about such a thing, but I live in this kind of area and know some of these people. They’ve all done what they were told to do from day one and now in middle age, very few of them are happy for it.

I hate CUVs in general – but if you don’t see that a Mercedes GLE is a *significantly* nicer driving experience than a RAV-4 or CRV, then you definitely need to just drive RAV-4s or CRVs. It’s not AS vast a gulf as between a Corolla wagon and my W124 Mercedes wagon was in 1988, but it’s still pretty damned vast. And on the flip side – the price difference isn’t nearly as much today either. $10K vs $45K in 1988 vs. $42K for a loaded RAV4 vs. $65K for a comparably equipped GLE. And realistically, a GLB is about the same price as a loaded RAV-4 and are comparably equipped too. The base RAV-4 is better value at $32K, but definitely lacking in amenities compared to the Mercedes.

I’ve been in both cars and neither are impressive. Yeah, the MB is nicer, but I don’t see what’s better, I see far shittier value for the money. Sitting in it was, like, eh, this is all the extra money? I can’t imagine spending so much more for so little if cars were just appliances to me and especially for someone who can’t shrug off the extra cost. These are used to transport filthy dogs and kids that spill literal and figurative shit inside of it, carry home improvement stuff, will sit in parking lots to get damaged by idiots, etc. If people can afford it, whatever, they’re not the subject here, it’s the idiots paying the rates and terms in the article who obviously can’t afford it that make no sense. I don’t care if the MB (or whatever it is, I didn’t specifically intend to pick on MB here) gave them a blow job every time they got in, if they’re doing 84 months at 8+%, they can’t afford it and that’s stupid as there’s nothing of necessity about something that much more expensive that does the same job as a cheaper one that also has lower running costs. Few of the people doing this are doing it for the petty luxury, it’s something deeper: a sad compulsion to think they’re impressing people or—worse—merely trying to keep up with some perceived comparative standard. They’re not their own people living for themselves, they’re living a life of comparison that revolves around the perceived judgement by others. Therapy is cheaper and offers a resolution to lack of identity and insecurity rather than unhappiness and a hamster wheel of debt (though a competent therapist that isn’t a drug dealer or who just tells you what you want to hear is a lot harder to find). It’s even dumber if it’s a premium car that is more likely to start having issues before it’s paid for. Then what?—oh the friendly salesman showed me how I can just trade it in and roll the difference into the the payments for the new one for only another $200/month! Maybe I’m wrong about the tone and purpose of the article, but as an alien anthropologist abandoned on this planet, my studies have led me to think that I’m supposed to feel sympathy when I read about how many people are underwater and defaulting on car loans and, disappointingly, I do . . . until I see the numbers and feel like a sucker for letting these creatures affect me.

As I have long said – if you don’t get what makes a Mercedes or BMW better, just buy a Camry and spend the difference on whatever does floats your boat. They aren’t for everyone.

I used to get MB when they still engineering-led instead of whatever inspires the crap they peddle now, but regardless, if you’re putting yourself into that much risky debt for one, that’s unequivocally stupid and, again, I merely used Eurotrash brands as an example—there are plenty of overpriced trucks, POS Jeeps, and even bland Japanese SUVs people are locking themselves into. In the future, I’ll try to remember to use them as an example because there’s something about referencing German cars that works like a hard stop to prevent a point from getting through.

I wouldn’t buy what they are selling *today* either – but neither of us are their current target market. Doesn’t change the fact that there is a lot of EXCELLENT engineering in them, even when combined with a fair amount of stupid at this point too. An E-class is still a better car than a Camry, if not as dramatically better as my ’88 was. But TANSTAAFL always applies too.

You could have summed it up with ‘image over content’. Some people believe they need to be seen a certain way to be considered successful by those around them.

As some people are willing to pay more to get more, even if that last bit of more is disproportionately expensive.

They do get to talk about their new car for a few months.

I think a great number of the people hand-wringing about “affordability” in the comments don’t quite grasp this number. A $1000 payment is not budget busting to a typical new car buyer, and with improved durability and resale, a 7 year term is not the end of the world either.

I yearn for the day when the site publishes an article about how more people having the income and desire to buy more and nicer cars is Good Actually instead of the 1000th iteration of the reverse.

“People having the income and desire to buy more and nicer cars is Good” reframe is maybe the wildest part of this. Record loan lengths and record monthly payments aren’t signs of a population gleefully trading up. They’re signs of people stretching further and further just to access basic transportation. The average new car in 2026 isn’t a luxury purchase for most buyers, it’s just a car. If people were genuinely more prosperous and freely choosing nicer things, you’d see shorter loan terms and lower default rates, not the opposite. Calling that a success story is a bit like seeing someone take out a second mortgage to cover groceries and saying “wow, people really love food these days.”

Are new cars more or less affordable compared to median household income than in the past?

The answer is more, but you won’t see that stat here very often.

100% love this article (post, story, IDK)…and a GREAT question. An interesting follow-up idea: How does this compare to the late 50’s to 60’s. Or even 70’s to early 90’s? Was keeping up with the Joneses trending at the same pace then as now? Lot’s to potentially be unpackaged here!

During the 50’s and 60’s? Definitely! 70’s? Not as much given stagflation and the oil crisis.

I see your point Gene… however I am curious to know the effects of stagflation and oil crisis… it would likely be an an anomaly … and that crisis led to the Pontiac T1000… a win!

The biggest effect besides focusing on efficiency, was the change of focus from speed and horsepower to handling. ) to 60 and quarter mile time sucked in the mid seventies and eighties, but lateral Gs stepped into the spotlight. (Mainly by the 84 Corvette with its touted 1G cornering.)

Also you had the rise of pickup trucks and SUVs as the sporty alternative. When the speed limit is 55mph and the speedo limited to 85, why not have a truck?

Is keeping up with the Joneses still a thing?

I thought that was an 80s thing that tv and movie producers caught onto in the 90s.

Still a thing. There’s some pretty shallow people out there.

I’m sure it’s fine if you don’t feel the need to put money towards a 401K or housing….

New car buyers are largely homeowners with plenty of money in their 401Ks. <shrug> Always have been. If you live in a wildly expensive coastal area, you can always move somewhere cheaper. Job pay doesn’t vary nearly as much as house prices do.

Pay doesn’t vary nearly as much as home prices Looking and median home price / median household income:

West Virginia is cheapest at 2.7

Hawaii is the most expensive at 9.9

I know. I have colleagues in 28 states. We all make about the same money, but the dude who moved to LA sure didn’t buy a house for $90K like I did when I moved to Florida a decade ago. He’s a network engineer so he makes a little more than I do, but nothing compared to the difference in cost of living. Same with the folks in NY/NJ. Those in the Midwest are a lot more comfortable. The one in Hawaii married really, really, really well so she’s doing fine, LOL. All the folks still near HQ in suburban Boston are pretty much screwed. But once the company made WFH an option for everybody, there was a diaspora away from that overpriced cesspit. I was hired as WFH 19 years ago and blazed a trail for non-sales folk to do so which Covid massively accelerated. My company is never going back to in-office for more than a handful of people, they massively downsized the space and are saving a fortune.

If you want to live in the cool places, you get to pay to play. God’s Waiting Room, FL is the opposite of cool, but it’s cheap and quiet and I will take FL summers over ME winters. Plus I was able to afford to keep my place in ME for summers anyway up to now.

I earned almost $200,000 a year in LA.

My cousin earned more than I at about $250k

I earned significantly money there than I did in SF, and she earned a great deal more money there than in Chicago.

Neither of us could afford to buy a 2br condo. Neither of us could WFH – pre or post-Covid. (she’s been called back to her office post-covid despite buying a place in Palm Desert)

Both of us had CPO cars there too – not $1000/month/7 year depreciation pits. We could have easily qualified for new cars at that cost range – but what a waste of money it would have been.

You listed 3 of the most expensive cities in the USA.

Nobody is forcing anyone to buy a $45,000 Highlander instead of a $30,000 Camry

Having both the income and desire are fine.

Long loans at high interest indicate the desire, but not the income.

I can understand taking a long loan by choice if the interest is very low, but that hasn’t been the case for a few years now. If you’re taking an 84 month loan in 2026, it’s because that’s the only way you can afford the monthly payment.

The average (mean) transaction price is up because buyers are choosing to purchase a more expensive class of vehicle. The buyer that can afford a Camry is buying a Grand Highlander.

Like for like cars are cheaper today than 30 years ago.

In 1995 a base Camry cost the median household 24.6 weeks of income

In 2024 a Camry costs 16.4 weeks of income

1996 RAV4 – 26 weeks

2024 RAV4 – 17.8 weeks

1995 Explorer – 29.7 weeks

2024 Explorer – 23.9 weeks

1995 Wrangler – 18.8 weeks

2024 Wrangler – 13.3 weeks

1997 CRV – 30.1 weeks

2024 CRV – 23.9 weeks

We can go on and on and on – It isn’t even close.

The gap is even more extreme for luxury cars. They are MASSIVELY cheaper today than they were back in the day. My ’88 300TE had an MSRP of over $45K. That’s pushing $100K in today’s money. For a car with plastic seats, a cassette deck, zero driver assists other than ABS, a manual driver’s side mirror, and a whopping 160hp and 4spds in the transmission. And only the rear wheels driven. The current one might as well be a starship for $70K.

When you adjust for content, modern cars are astounding value. Also, I owned that car when it was about the same age and miles as the ’14 E350 wagon I have now – the ’88 was rusting (despite also being a Florida car it` had some top down coastal rust) and had lots of fun mechanical issues to sort out. Cars really do last a LOT longer and are more reliable along the way, even German ones.

Of course, given the choice, I would choose a brand-new ’88 wagon, but my Luddite tendencies are well known here. That they don’t make them like they used to is both good and bad. 🙂

I understand that, but I would say that the 84 month loan on a Grand Highlander is more likely to default than a 60 month loan on a Camry.

If this happened in a way that only caused inconvenience to the lender and borrower I wouldn’t mind.

Recent history has taught us that when these perpetually negative equity loans eventually default, it’s society as a whole paying the gambling debts.

Anyone defaulting on a 84 month loan on a Grand Highlander has nobody but themselves to blame. Nobody needs a new Grand Highlander. That is a want not a need.

The return to normal interest rates over the last few years should be a wake up call to a lot of people but the data isn’t showing that. They are just doubling down to continue a lifestyle they can’t afford instead of dialing back.

Yes, large debt bubbles can cause trouble for the general economy. The only thing we as individuals can do about that is to get our own personal finances in order.

If I was still massively overextended in 2009 like I was in 2001 the “great recession” would have been devastating. Instead my time unemployed was time spent doing projects around the house and I saved a lot of money vs paying a contractor to do that work. Digging out from early stupid financial mistakes wasn’t fun, took years to accomplish but paid off in the end.

I would like to blame it all on personal responsibility, but there’s blame on both sides of the transaction.

I expect consumers to act irrationally. I used to expect banks to act responsibly.

Banks are acting rationally. They package auto loans and sell them off to investors as an ABS (Asset Backed Securities) The bank is a middle man in the sale of financing just as the dealer is the middle man in the sale of the vehicle.

It is also rational for a bank to offer longer loans as they make a lot more per loan. Look at the example in this article where the 84 month loan brings is 5x more in interest payments. Yes, more people will default but the higher profit per loan covers that and the loan is backed by a physical asset that can be repossessed and sold at auction.

Is pushing buyers into long high interest loans moral? I would say no but it is very much rational.

For my part, I was referring to the entire lending side of the deal as the ‘bank.’

IMHO, the bank should first be concerned with lending money to people who will pay it back. The fact that the borrower’s ability to repay is a distant second (at best) to the lender’s ability to bundle and sell the debt is troubling and obviously has lead and will continue to lead to trouble.

Even by your definition – “banks” are still being rational. The name of the game is making money and if profits increase along with defaults then banks will do that.

At the extreme end are payday loans. Those are extended with full knowledge that many will never be paid back in full but the high rates still make it an extremely profitable business.

That’s the problem. Bank and Investment Bank are now the same thing.

As long as that remains the case, we’ll keep running in the same circle (or jumping off the same cliff).

The idea of investment banks is relatively new thing and didn’t prevent banking failures in the past like the S&L crisis in the 80’s.

The cycle of increasing debt and then loan failures is as old as the idea of loans and banks. Read up on the bank crisis of 371 BCE where Greek banks failed after overextending loans for merchant shipping.

Banks act extremely rationally and responsibly in terms of making money for their shareholders. They don’t give low interest loans to deadbeats. The high interest and/pr long term loans are highly profitable even if they have to repossess and resell the car. Far more so than the pittance it takes to deal with defaults.

Unlike houses, cars are *easily* repossessed and resold. That and realistic loan pricing in the first place is a HUGE difference between the mortgage loan crisis of getting on 20 years ago and car loans today.

Or it still makes sense from a cashflow perspective. Even at 8%, a loan would be cheaper than my cashing in investments today. But I would never have to pay that much interest on a car, even today. The best time to borrow money is when you don’t actually need to, in a lot of ways.

The people with those considerations aren’t processing a conventional secured auto loan for purchase and therefore aren’t showing up in these numbers.

In the world of a 60 month Camry buyer who instead stretches to become an 84 month Grand Highlander buyer, he probably does not have established lines of credit.

Sure they are. Like I said, I didn’t HAVE to borrow money for my last bunch of cars, but it made more sense to do it than not do it. They were all normal car loans. Mix of from my bank or the dealer, whomever was cheaper each time. Or in the case of my GTI, initially through the dealer to get a spiff, then refinanced at my bank the next day.

And I suspect that Grand Highlander buyers aren’t the ones getting 84mo loans. I would be looking at Stellantis, KIA/Hyundai, and Nissan dealerships more than Toyota dealerships. But even so, people do seem to be willing to pay longer to get what they want, even if it’s not what they necessarily need. Most can swing it, some can’t. But ultimately, it doesn’t matter at all. Car loan defaults are not the same as mortgage defaults in their ability to affect the economy, so the pearl-clutching and hand-wringing is rather silly. Heck, all the used car only buying types should rejoice in the added inventory that might result.

I had the same notion about lower-end manufacturers, but the percentage of 84 month loans is more than Kia / Hyndai’s entire market share.

I don’t know if those loans are financing Highlanders or domestic pickups, but they’re not all going towards Kias.

It wasn’t the loan defaults that caused the crash last time. The derivatives market based on those loans was many times larger than the mortgages. I assume all those same investment products are in-place for auto loans.

The auto loan market is a fraction of the mortgage market. And as I keep saying, cars are easy to repossess and resell. Rightly so given the stakes, houses are expensive and time-consuming to repossess and resell, and of course the amounts of money involved are hugely bigger. Cars are chump change compared to houses.