I had a bit of a whiplash moment this morning. Two well-respected analysts came out with reports about vehicle pricing and affordability, and neither report quite agreed with the other exactly as to the culprit. It’s a fun exercise to read both back-to-back as the problems are clearly identified and yet, while there’s some overlap, I don’t see fingers pointing quite in the same direction.

The Morning Dump will take a bit of a different approach this morning as I’m going to take the news of the day and analyze these two reports in the context of what they wrote, with the hope of coming to some sort of answer as to why no one has a clear answer. Obviously, I’ve written about this a lot this year, so I’ll try not to repeat myself too much.

This morning’s first analysis comes from Jessica Caldwell and her team at Edmunds. The other report is from Erin Keating at Cox Automotive. Edmunds, being B-to-C-focused, tends to have a consumer perspective, whereas Cox Automotive is a bit more B-to-B, but both are historically the best resources when it comes to tracking these issues.

The Manufacturer Is To Blame

This is the easy finger to point. Cars have gotten too fancy and too expensive and automakers have abandoned the lower-end of the market by getting rid of the sub-$25,000 car in almost every context. This is also the Trimflation argument, which is that automakers have prioritized higher margin vehicles and trim levels, meaning that even if a cheaper MSRP vehicle theoretically exists, few of them ever end up being built and sold.

This factor is called out by Edmunds, which reported today that a record number of people are taking out loans that are 84 months or longer.

“Unfortunately, this is the new normal for new-car buyers. Until we see a major shake-up in automaker incentives, a meaningful drop in interest rates, or a shift toward a more affordable mix of vehicles — none of which appear to be on the horizon — consumers will have to keep walking this financial tightrope.”

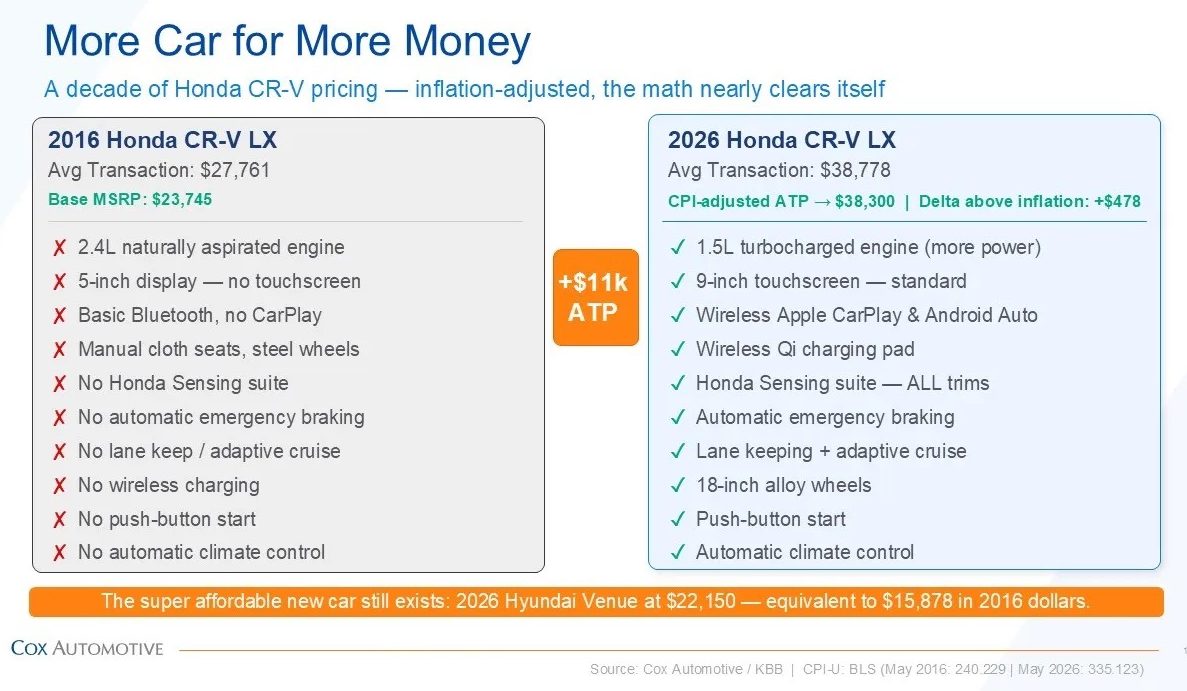

It’s the mix! This is definitely true, to some extent, although this chart from Cox is interesting:

A 2026 CR-V, when adjusted for inflation, is only about $500 more expensive, yet offers way way way more stuff, and more stuff that people want. Specifically, the report from Cox is called “The Car Is Not the Villain” because, even though ATP is up $11,000, it’s more complicated than people just buying good cars.

Today’s CR-V includes turbocharged performance, advanced infotainment, wireless smartphone integration, and driver-assistance technologies that were optional or unavailable a decade ago. It is a better, more capable vehicle by almost any measure. Once adjusted for inflation and income growth, the price has barely moved.

The increasing price of the car is real, but is that the manufacturer or the consumer driving this trend?

The Consumer Is To Blame

As the Edmunds report points out, consumers are hitting record lengths and amounts for loans, with potentially dangerous outcomes:

“Car shoppers are caught in a dangerous practice of focusing heavily on their monthly payment while ignoring the potential long-term damage to their wallets,” said Ivan Drury, Edmunds’ director of insights. “Pushing loan terms past six or seven years might make an average monthly payment more digestible today, but it’s a mathematical trap. When you pair a 7.0% APR with an 84-month loan and a smaller down payment, you’re signing up to hand over nearly $10,000 on average in interest alone. Unfortunately, stretching out the term to be able to swallow a higher-priced vehicle guarantees you’ll be building equity at a snail’s pace, leaving you highly vulnerable to falling underwater when it’s time to trade in.”

Are car shoppers being irrational here? Cox would argue that getting a slightly higher trim vehicle isn’t necessarily bad:

There is also a common-sense piece to this. When the price gap between a base vehicle and a better-equipped model is relatively small, many buyers choose the vehicle with more features, better fuel efficiency, or stronger long-term usability.

That behavior is rational. Consumers are thinking about total value, not just the lowest entry price. Over time, those choices shift the sales mix and lift the industry average. The headline number moves, but the underlying story is consumer choice.

It’s true that consumers are not as interested in cheaper vehicles. Given how long people keep cars these days, I do wonder how much of an impact option for the cold weather package or whatever matters 13 years down the road. If you sell your vehicles at a more normal rate, then the options you have can command a higher price.

Politics Are To Blame

Tariffs have added costs to new cars, as have safety regulations and environmental regulation. This is nowhere clearer than on the lower end of the market, as the United States has long relied on imports for many of its cheapest cars. Nissan, which often offers the most affordable cars on the market, does so by relying largely on Mexico for production.

With the USMCA under review, the prospect of bringing more cars from Mexico is a sketchy one, with Nissan’s CEO Ivan Espinosa pointing out to Bloomberg that the company is suddenly paying 25% more to import its cars:

The duties are “making part of the lineup that we are bringing in from Mexico difficult to sell,” Espinosa said Wednesday on Bloomberg Surveillance. “Looking at the pressure that the US market has today in terms of affordability, we see that potentially some of the buyers could be moving into this type of vehicle, so we are working very strongly on making them more competitive.”

[…]

While the company has shifted some vehicle production to reduce its tariff exposure, it’s kept entry-level models like the Nissan Sentra compact and Kicks crossover in Mexico to take advantage of lower labor costs. The manufacturer has said tariffs on the Kicks and Sentra cost around $2,500 to $3,000 per vehicle.

$3,000 on a Sentra is insane and, even if the goal is to bring more manufacturing to the United States, the medium-term impacts are extremely real. Nissan is trying to find ways to make the cars cheaper in Mexico as opposed to just bringing production here.

Politics is definitely playing a role, although it varies a lot by car, and politics aren’t making people buy $50,000+ three-row SUVs.

It’s The Economy

Consumer preference, regulation, politics, manufacturing choices, et cetera are all part of the picture. The sad reality is that many things are conspiring to impact the car market, and there’s very little consumers can do about it because of the underlying economy. This is something that all the analysts seem to agree on, and though it isn’t necessarily the main culprit, it’s the one factor that is insurmountable for a consumer and difficult for automakers to impact.

First, from Cox:

The bigger issue is the economic environment around the vehicle. Purchasing power has been stretched, household budgets are under pressure, and consumers are absorbing higher costs across nearly every part of daily life.

Vehicle insurance has risen sharply. Auto loan rates are higher, so borrowing costs more. Maintenance and repair costs are up. Gasoline is higher, too. So are housing, groceries, healthcare, and subscription services.

In that environment, it is no surprise that a new vehicle feels out of reach for many Americans. But the issue isn’t the car itself — it’s because life got more expensive.

And from Edmunds:

“The Q2 data perfectly illustrates the stark reality of today’s new-vehicle market: Affordability is such a massive hurdle that buyers are forced to stretch their budgets to the absolute limit just to get into a new vehicle,” said Jessica Caldwell, Edmunds’ head of insights. “When you see loan terms extending to record lengths, down payments shrinking, and monthly payments hitting all-time highs, you’re looking at a clear recipe for long-term financial strain.”

Some consumers are too stretched by all the various negative economic factors, whereas other consumers are driving the K-shaped market by shrugging off those concerns and demanding bigger, better, nicer. Automakers are also facing these concerns as money is more expensive to borrow and they, too, will reach a limit of what they can offer affordably to consumers.

In the end, the fingers are pointing in various directions because there are legit that many directions to point in these days.

What I’m Listening To While Writing TMD

It’s “Cats” by Mitski, because my cat was up this morning yelling at me to feed him even though I’m wiped after the track day.

The Big Question

What would you bring to an Autopian track day?

Top graphic images: stock.adobe.com; DepositPhotos.com

My .02 is that everything has gone up other than wages.

A 1996 Corolla had a base price of about 13K. Today that would be 27,700.

The base price of a 2026 Corolla is $23,125. A 2026 Corolla is pretty much an S-Class compared to a ’96, so in fact you get more for less, relatively speaking.

It’s the cost of everything else that is (pardon my French), fucking people.

(Funny story, I once said that in a group of actual French people, and they looked puzzled, and asked why Americans say that).

Just look at the cost of housing alone- it’s skyrocketed since 2020. Even for the people that had the good fortune of buying pre-2020, they’re still paying more via property taxes. That home that was purchased for 200K is now worth 450k and taxed accordingly. And for those who weren’t able to buy then, good luck saving now that the rent has likely doubled.

Theres a segment of people experiencing unprecedented wealth growth, while the rest of us stagnate and fall further behind. The current wealth gap is larger than during the Guided Age, it’s time to start sharpening the pitchforks.

Your comment on the housing is correct. I bought well, but my town is increasingly gentrified. Families don’t stay so the turnover is high, and transaction prices are escalating. Seen many houses here double in just a couple years.

It’s wild in my area. Not too long ago, a local realtor posted a slide show of homes purchased 10-15 years ago with the selling prices of then vs now. It was supposed to show what a great investment local real estate is, but it just pissed people off. It was mostly average looking 400-500K-ish family homes selling in the millions now. .

This would imply everyone’s assessments have gone up, which would mean no one’s taxes have actually gone up. The way your taxes would increase is if the budget dramatically increases, or if your assessment in relation to everyone else’s assessment in the tax levy, has gone up.

My taxes went up based on assessments. Costs for my town went up, so there is that

Housing is a whole other thing. 100 years ago we would use some land and materials to build a two-flat of (2) 1200 square foot homes. Now we use twice the land and more materials to build (1) 4000 square foot home.

Yeah, it doesn’t matter if the cost of something has only risen because of inflation if people’s wages haven’t also risen because of inflation.

In California Prop 13 locks in the taxable value of your home at whatever you paid for it (or your parents paid if you bought it from them or inherited it). There are large numbers of million dollar+ properties in CA that pay taxes as if they are still worth <$100K.

Prop 13 doesn’t lock taxable value, it limits annual increases in assessed property value to 2%.

I learnt that expression relatively recently from British person. I thought it was very funny.

I’d bring my TR6 to a track day!

Shareholders looking for higher returns. The people with money want to make more. Consumers-“Look, I bought a new car! Look at how nice it is! I got all the options so when I sell/trade I’ll do better!” Which as was noted above means you’ve negated that with interest. Never mind that some of those features broke a lot.

I would drive a base model with a great drivetrain.

Oh yeah, and while the cars are better adjusted for inflation, my income has not

Up until my last car, I did. Spent everything on engine / mechanical upgrades. Nothing on extras.

Unfortunately, not a lot of that with US offerings. Can’t get a wagon never mind an inexpensive new one

Just checked out of curiosity. The cheapest estate car here is the Seat Leon Sportstourer. You can have it with a 115bhp 1.5 litre turbo engine a six speed manual for €23,200 (around $26,400).

I blame capitalism and corporate money mining. Landlords, C-suites and shareholders. They want to make us into a society of subscribers, endlessly paying for everything.

I get that profit is the goal. They’re in the business of making money, which they do by selling cars. That’s fine; if you aren’t paying the bills you’re going broke. But to what degree is anything owed to the shareholders? Are executives actually worth millions of dollars when line staff are making one-twentieth as much?

Please note I say this with only a single 100-level Economics class and a bit of Business Ethics, and the argument of what shareholders are owed was vigorous, beginning in no small part with whether anything was owed at all. One thing we all agreed on was that shareholders’ engagement of business-related gambling was voluntary, which absolves business of a modest portion of liability.

Modest.

Obviously the whole point is to make money. How much money they get to make, well, there’s no promise there. And if they’re going to price the damned things like they’ve got a megayacht payment to make, we’re not going to buy. We don’t owe anyone that yacht, we don’t even owe anyone the opportunity to shop for a yacht.

I make decent money – not great by any means, up until last year we very nearly came close to breaking the six-figures mark but that has since changed. But the house is paid off and we live modestly. We could afford some stuff. But with the average new car price at $49,000, I don’t think we could afford a new car. And with the price of new cars going up so quickly, now there are previously-inconceivable 84-month car loans. Because people still need cars, and the banks don’t lend the money for free because they have shareholders too, all of them trying to get rich. How long before we see a ten-year car loan?

I say all this knowing that, as a holder of a shares in several mutual funds, I am among those people. But I’m not trying to get rich per se, I just don’t want to starve after I retire.

Still. Automaker executives. Shareholders.

They keep telling us that AI will make a lot of labor obsolete, and I agree. I’m fairly certain the CEOs and top-tier executives are a first choice for replacement with AI, provided the existing layer of middle managers protecting the rest of the company from the executives is retained, for obvious reasons.

But the cost of housing has rocketed up at a pace that far outstrips that of either inflation or wage growth. A house that cost just $100k in 2000 can, depending on the market, now cost 4x as much. I know that my house’s price has gone up by a factor of three; I couldn’t afford to buy my own house if I were shopping right now. Corporate landlords snapping up all the available housing and treating it as a money mill is poisoning the housing market, forcing hundreds of thousands of people into difficult decisions where they have to ask, which one can they cut back on: someplace to live, or something to drive? Some make the decision one way and become Van Lifers, and others become tenants, shopping deep into the classifieds for the reliable wrecks, driving up the prices on ten-year old Corollas.

What would I bring: I can’t afford anything special to bring, so I will bring my 1987 Toyota Truck. It isn’t fast, but I can help carry your wreckage home for you.

Are you under the impression that in some previous decade where cars were more affordable, that capitalism wasn’t in place? Or that cars were affordable in the USSR?

Excellent response.

So much hate on these boards for capitalism…

Lots of hate for capitalism. Cars were more affordable as people had more buying power. Enjoy your dividends

I don’t have dividends.

And I’m not that smart, but have enough neurons to see capitalism may suck, but it sucks less than any other system that has been tried

The outcome of chasing the dragon of infinite growth. Gotta keep the stock price going up to keep the shareholders happy, but once the market matures, no choice but to start squeezing customers.

The car market has been “mature” in the United States longer than the vast majority of Americans have been alive.

The bottom line is that wages have gotten so far behind the rest of economy in terms of increasing along with it, that we are all a lot poorer, even while working more and more.

What would you bring to an Autopian track day?

I’d bring my 2021 F250 diesel. Of the five vehicles in my fleet, it is somehow the fastest and best handling. I need to buy the Mustang from today’s shitbox showdown just so I have something semi appropriate to take to a track in case the opportunity ever arises.

As for the cost of cars, trying to argue any single factor is the primary driver is kind of silly. Realistically, it is a combination of consumer expectations, cheap/easy credit (even with interest rates that have gone up the last few years), the cost of labor (which paradoxically can increase as efficiency/worker productivity increases), geopolitical issues (tariffs, etc.), the cost of raw materials required to build complex modern vehicles, and probably twenty other factors I could name if I cared enough to think about this for 10 minutes.

What about the banks? They’re the ones approving those ridiculous loan terms.

They are setting the loan terms, not just approving

Yeah, that too! The math to make an 84 month loan on a depreciating asset as collateral worthwhile is interesting to say the least.

I am afraid I won’t be able to afford used soon as there will be less cars and they won’t be as easy to repair

84 month loans are only the fault of people buying the cars. In the end, the buyer is the one making the payment. If you need a 84 month loan you need to lower your car standards.

Or, you have the money to afford it and the interest rate is low. Then you’re just smart.

But but but I deserve a better car! And I haven’t learned any personal responsibility.

And maybe ‘the government’ will pardon my stupid car loan, the way they keep talking about pardoning borderline mentally challenged college loans

I don’t think people expect the government to bail out their car loan, they just aren’t thinking long term.

(Also, forgiving predatory college loans was a good thing.)

Great analysis. You’re forgetting also how capital wants higher and higher returns, so I’d add your 401k as a villain.

Now, can we clarify some misleading crap in that 2016-2026 comparison:

– a push button should be cheaper to make so that should be a downgrade for numbers sake (ironic that consumers think it’s an upgrade but see cause #2)

– same goes for the 1.4 engine. Should be cheaper to make, where’s our credit? (Please don’t mix R&D here since we have to assume 2016 Rav also had that going compared to 1996 models)

– Apple car play and other tech add-ons put money in the pockets of tech monopolies and away from shoppers. That’s a usability upgrade but can’t compare it to “we didn’t use to have CarPlay in 1996”. No one is comparing 2010 Sirius service to CarPlay and they should because maybe we don’t want it. Oh, you mean to tell me that it’s fully integrated into the car’s telematics and we don’t have a choice? I see I see.

Having nearly 100% of the population on a 401k retirement plan has resulted in pressure on companies to show short term growth over everything else.

How is a turbo and intercooled engine cheaper?

Not sure if I understood you correctly, but smaller engines are not necessarily cheaper to make, especially if there is a technological difference (turbos, direct injection, etc).

Seriously? Its literally the automakers, they chose to discontinue cars, especially smaller cars, in favor of SUVs and pickups. They chose to discontinue base trim levels and sell everything well equipped, they chose to repeatedly raise prices on the same old models that have been in production for ages, when amortization of tooling and R&D should be making them cheaper to build per unit

While that’s absolutely true when talking about Ford and Stellantis, but what about the other 15ish companies? GM, Honda, Hyundai, Mazda, and several others all have ~30K cars that I would actually want to own.

Right, but they used to sell even smaller, cheaper cars. Those are gone.

🙂

yeah that’s true, but the only one of those I’d personally want to own was a Honda Fit…

edit – My mom’s Kia Rio of the last year they made it really surprised me by how much I liked driving it, even with the CVT. I much preferred it over the 2010 Camry she had even though you might be able to argue the Camry was a “better” car.

That is simply not true, and I have a close example. A cousin of mine had a Fiat 500 which she replaced with a Toyota Yaris Cross. Nobody forced her into the crossover as Toyota still sells the regular Yaris hatchback. She chose the crossover on her own.

TBQ: My 03 Honda Civic LX and my 13 Honda Civic Si of course.

I could finally get lap time comparisons, and while I know the Si is faster, how much faster is it really?

Also, which is really more fun to drive full out? I don’t know that my skills will keep up with the Si at full tilt, while the Lx is so slow as to be frustrating on big straights. My instructor at my last Open Track Day commended me on the Lx “Get good divining this and you’ll be a monster in something capable” sadly that was two summers ago, and I haven’t been able to go back.

Inflationary adjustments are not an accurate comparison of “cost”. The best measure is hours worked. Take your pool of buyers of given product, find their average wage, then find how many hours it takes them to purchase that product. Do that for both time periods. If hours went up, cost is up. If hours went down, then cost is down.

Great. So for the CR-V above. Median wage (according to bureau of labor statistics) unadjusted was 37,040 which works out to 17.80 per hour. The 2016 costs 1600 hours of work. 2025 (26 data not yet available) is 62,088, or 29.85 per hour. The 2026 car costs 1300 hours of work.

Happy to accept other sources of data if you prefer them.

So 300 hours less. Now whats the hours difference for median healthcare, education, and housing expenses?

That’s not really about the car anymore, is it?

If all your labor hours “saved” buying a new car spent somewhere else and then some, that car isn’t exactly more “affordable”. You can’t talk about affordability in a vacuum.

But then you’re no longer measuring the affordability of just the car, you’re measuring how attainable everything in the amorphous bucket called “lifestyle” is. I’m not saying what you’re pointing out isn’t a problem, just that the evidence isn’t there that cars are a significant part of the problem.

How exactly does affordability of a car works, if you don’t take into account available money to spend on a car?

Because words have meaning. Cars are more affordable by the similar car/hours worked metric. Housing is less affordable by the same metric. So claiming that cars are less affordable because housing is more expensive, even when cheap cars are still cheap but fewer people are buying them, doesn’t make sense. Certainly GM isn’t responsible for housing being more expensive!

A car of the same size and level of luxury costs the same as it did a couple of decades ago.

Cars are more expensive because small, cheap cars went away. That happened because customers stopped buying them. That happened because CAFE stopped the subsidy towards Focuses and Cruzes and the upper-middle-class Democrats who had bought those cars went electric instead.

MSRP has certainly increased for many models but they aren’t always getting it. Ram and GM trucks might be be the best example. 10 years ago you might have been able to get a base work truck for $23k to $25k now you can for $25k to $28k. BEV MSRP over all have gone down while getting more. MSRP is the problem because they thought they could get often did and don’t want to reduce it now the things are regular and free money is gone.

I’m not sure how we calculate inflation works anymore half the time some greedy greasy little man corners the market on something making consumer costs going up. Stamped lumber for instance. Everyone was getting payed the same except the tree owners were getting less. Retail lowered their profits and yet prices were at least 500% over what they had been just months to a year before. Now they are more or less back to what they were. The egg supply issue caused a lot of consumer goods to increase now eggs are back to where they were. We had chicken issues a few years ago that is now back to about normal. Now we have beef issues that won’t stabilize for a few years. Gas prices are rapidly falling after over doubling in many places. We are also in a massive housing market correction. Florida and Texas appear to be leading the charge.

“The Big Question What would you bring to an Autopian track day?”

I’d gather all of the readers who owned a Chevrolet Trax so you could call it the Autopian Trax Day. 🙂

Personally I think the affordability issue, at least in the US, is the decades long societal prioritization of personal wealth and corporate profits. Seem to me as time goes on, I see more and more emphasis on the stock market = the entire economy, and numbers where it looks like the top 10% of people is now 50% of spending and rising. The automakers and dealers cater to the top end, as that is most profitable, and they are probably buying the majority of new vehicles. Many (not all) consumers seek to stretch themselves to the limit to make payments on the biggest, fanciest thing they can make the monthly payment on. Everything is driven towards big, fancy, and expensive from all directions.

“Look how nice my new vehicle is”

wow.

”I worked with the dealer to get the payment down”

I had this conversation three times. None of them kept the vehicle more than 3 years. Have a scuba tank

Maybe my own French car if I can find a small enough grandfather clock:

https://live.staticflickr.com/65535/52763070823_2cfb092975_c.jpg

https://live.staticflickr.com/5302/5600648065_1cce953440_c.jpg

The average American has been proven to be a financial idiot unfortunately. People seem to not be able to see beyond a week to make decisions.

I’ve always been fortunate enough to pay outright for used cars within my budget, the idea of a loan on a car makes my stomach turn

What about a loan at 0%?

Loan at 0% or 1% makes sense if the cash flow is there. Pay in future dollars that are inflated compared to today’s dollars. Plus keeping other investments available to make more money makes sense to me. If you want a new car, there are much worse ways to go about purchasing one than the manufacturer eating the interest.

I bought my first BMW motorcycle at 0% interest!

This would be the exception if you need a new car. But again, if I can keep one more recurring bill out of the budget, more peace of mind

Considering how finances are not taught in public school (or at least while I was there), that doesn’t seem like a coincidence.

The average American has been proven to be a financial idiot unfortunately.

I suspect it would be equally accurate to say “The average person has been proven to be a financial idiot.”

The biggest difference is that, in America, we don’t have nearly as many consumer protections to save us from ourselves. I’m not going to argue whether this is a good or bad thing (the lack of protections is probably good for some and bad for others), but I wouldn’t assume consumers in other countries would make better decisions if given the same opportunities.

Never mind the current admin is trying to sabotage the agency trying to help

All this points to complex factors. As evidenced by our comment section where intelligent people are citing quality sources about inflation, cost of living, purchasing power, or whatever other measure of consumer costs/income seems to model one’s personal beliefs and intuition.

I think two things are clear though:

Perception is that costs are wildly out of control and most people can’t afford what they want. Everyone expects a catastrophic recession soon. The CA LAO has been calling for it every year, and every year CA ends up with billions more revenue than projected. There’s a huge perception gap even among experts. And of course, applied economics is a lot about vibes.

Two+ decades of zero rates at the fed has conditioned folks to think that amortization of large purchases are free. People are looking at the sticker… but as we all know that’s not how a majority of people shop. The increased costs might not be about cars at all…

TBQ: my custom porteur bike with all the fancy luggage.

TBQ: if motorcycles are allowed, I’d bring one of mine! Otherwise my Bronco.

Politics are broadly to blame, period.

Politics impact every aspect of the vehicle purchase price. Politics impact what can and cannot go into a car (expensive EU compliant emissions equipment, GPF, etc). Politics impacts how much it costs to bring a car into the country (wildly inflated due to ridiculously stupid tariffs). Politics impact the state of the economy (not so great right now due to the *everything* going on).

Politics impacts the economy from the Fed Reserve side in that high inflation leads to higher interest rates. Politics impacts the perception of Americans when it comes to CPI, Cost of Living, etc. Politics impacts how automakers structure product portfolios, knowing that if cost of selling cars is high, trims must get inflated or prices must go up to account for this. Politics impacts the cost of repair bills and parts, of gasoline, of everything.

The argument against EVs and Hybrids I hate the most is that “the government can’t tell me what I can and can’t drive so I wont drive an EV.” Well listen pal, the government has done exactly that since before WWII. Politics have grown increasingly fast paced and short sighted in the US, and that acceleration of the full cycle from policy to impact lays bare just how definitively that politics drives this above every single other factor.

I appreciate the commentary, and to me it still points to expected shareholder profits

TBQ: My FR-S is the only car that runs. I mean I could road trip the Bug once it runs. But it doesn’t.

Let’s not forget to put some blame on dealers too. They know exactly what they are doing to affordability when every car on the lot has some combination paint coating, window tint, nitrogen filled tires, and fabric protection jacking the price up hundreds to thousands of dollars.

The “VIN Etching” that they wouldn’t remove from my bill of sale because they “already did it”. I still don’t know that they etched. I’ve never seen it.

I’m pretty surprised there was no finger-pointing at greedy gouging dealers and their bullshit fees, not to mention their scummy high pressure sales tactics. A glaring omission, if you ask me.

Re: consumers – I vehemently disagree with this take. Consumers are forced to look at the monthly payment because the overall cost has risen so much, so quickly. If the damn things were actually affordable for most people, we’d be able to look at that instead of the monthly payment.

Also, let’s not forget that dealers are ordering vehicles on spec, so they’re checking the option boxes that’ll appeal to the vast majority of buyers . They don’t want a lot full of low-spec strippers that will have limited appeal to go along with their limited margins. Nowadays, if you want that base model with no options, you’ve got to find a dealer and manufacturer who are willing to work with you to special order for your unicorn – and at that point, you’re more likely to pay as much or more than you would if you simply accepted something from their existing inventory.

TBQ: Our new Mazda CX-90. Sure it’s way too big to be a proper track car, but I’d like to learn what it’s actually capable of in a safe environment. I have no interest in driving performance cars at half of their limits because of my lack of skill. I am much more interested in pushing my everyday car to the edge to see exactly where that is.

Car pricing: most of my career has been involved in the engineering and manufacturing of complex systems for transportation and energy. The idea that physical goods somehow keep on getting cheaper every year is an anomaly of like the past 30 years of economic development, mostly due to shoving externalities off to Asian (read: Chinese) manufacturing. Modern cars are amazing chunks of engineering, vastly safer, more efficient, and capable than their predecessors, and as the Honda comparison shows, not actually that much more expensive when adjusted for inflation.

They also last a hell of a lot longer than they used to. We talk about 72 and 84 month auto loans as if it’s a terrible calamity, but I think this is misplaced. If you take a 7 year loan for a car thats going to be dead after 5, that’s stupid. But most modern cars will last 20 years plus, they are actually durable goods in the economic sense. So it might actually be a wise decision to finance long term, especially given how prevalent subvented financing is (Mazda was happy to do 0% for 72 months on our car, and while we could buy it outright that is actually a hell of a lot of free money on offer if you invest it instead).

Please stop using “adjusted for inflation” in arguments. I don’t know a single middle class person where their pay has ever kept up with inflation.

TBQ: if you ever come close enough to me, I’ll bring my MGB 🙂

This exactly. Especially in the last 6 years since covid, my wages, while up, have nowhere near kept up with even a conservative view of overall inflation.

If wages had grown with productivity since the Reagan years, the federal minimum wage would be around $24 an hour by now. You’re very right in that “adjusting for inflation” is not as helpful a statistic as it could be unless it’s coupled with something that also describes the “average” person’s actual buying power as well. Going back to the 1960s, not only was a dollar “worth” more relative to later years due to inflation, but wages relative to dollar value in the market were higher, too!

A thing that raises my hackles is when I see current economists trying to argue that “well, inflation isn’t actually that bad because wages are growing, too,” neglecting that “inflation” does not apply to all goods equally and the index prices for things such as food, rent, and other necessities have eclipsed any growth in wages for the lowest earners.

I know I’m a pinko-commie socialist cuck-lord or whatever the term is now (soy? Something with soy?), but I am starting to think an economic system where we keep funneling money to trillionaires to play astronaut in low-earth orbit while everyone else just gets poorer and hungrier isn’t a very good system!

Man, I’d love to make $24 an hour. That would address a ton of day to day anxiety.

Hmm the French figured that out sans internet in 1789. They came here to avoid the same mistakes and -wait…

I am not an economist, but I took a statistics class once and I know “average” is a terrible metric.

People don’t get pay raises for staying in a job, only when the switch jobs. And the “average” person doesn’t have the ability to change jobs.

For example, managers at a big company move up every 3-5 years and are way ahead of inflation. The engineers stay in the same job or pay band for a decade getting maybe 1-2% increases per year. But hey, the pay increases for that one manager averages with the 50 engineers, so pay is keeping up with inflation!

What do you suggest doing then? Objectively, dollars then are not the same as dollars now, so some adjustment is needed to compare. What’s your preferred model?

Uhhh…. why? It’s objectively true that a dollar in 1900 had a far greater purchasing power than a dollar today, that delta is inflation. Now if you want to debate about which inflation metric to use or how to adjust for the glaring deficiencies in certain metrics (like CPI), those are certainly discussions worth having. But inflation is a natural result of a productive economy and absolutely should be factored in.

Helping this take with some easy data: minimum federal wage went up roughly 200% since 1985, while prices hiked 300%. So at the very least we’re poorer by a third here in the US. There.

But almost nobody makes minimum wage, so that’s really not useful data.

I…don’t believe you.

The article starts with a false premise. Cars are not more expensive today so there is no reason to try to assign blame.

Price is just one half of “affordability”.

The issue is everything else is more expensive, people cannot afford homes, etc.

And if that’s the issue, then the premise of the article is false, as Jason says. Examining whether Stellantis is to blame for housing prices is, obviously, absurd.