I had a bit of a whiplash moment this morning. Two well-respected analysts came out with reports about vehicle pricing and affordability, and neither report quite agreed with the other exactly as to the culprit. It’s a fun exercise to read both back-to-back as the problems are clearly identified and yet, while there’s some overlap, I don’t see fingers pointing quite in the same direction.

The Morning Dump will take a bit of a different approach this morning as I’m going to take the news of the day and analyze these two reports in the context of what they wrote, with the hope of coming to some sort of answer as to why no one has a clear answer. Obviously, I’ve written about this a lot this year, so I’ll try not to repeat myself too much.

This morning’s first analysis comes from Jessica Caldwell and her team at Edmunds. The other report is from Erin Keating at Cox Automotive. Edmunds, being B-to-C-focused, tends to have a consumer perspective, whereas Cox Automotive is a bit more B-to-B, but both are historically the best resources when it comes to tracking these issues.

The Manufacturer Is To Blame

This is the easy finger to point. Cars have gotten too fancy and too expensive and automakers have abandoned the lower-end of the market by getting rid of the sub-$25,000 car in almost every context. This is also the Trimflation argument, which is that automakers have prioritized higher margin vehicles and trim levels, meaning that even if a cheaper MSRP vehicle theoretically exists, few of them ever end up being built and sold.

This factor is called out by Edmunds, which reported today that a record number of people are taking out loans that are 84 months or longer.

“Unfortunately, this is the new normal for new-car buyers. Until we see a major shake-up in automaker incentives, a meaningful drop in interest rates, or a shift toward a more affordable mix of vehicles — none of which appear to be on the horizon — consumers will have to keep walking this financial tightrope.”

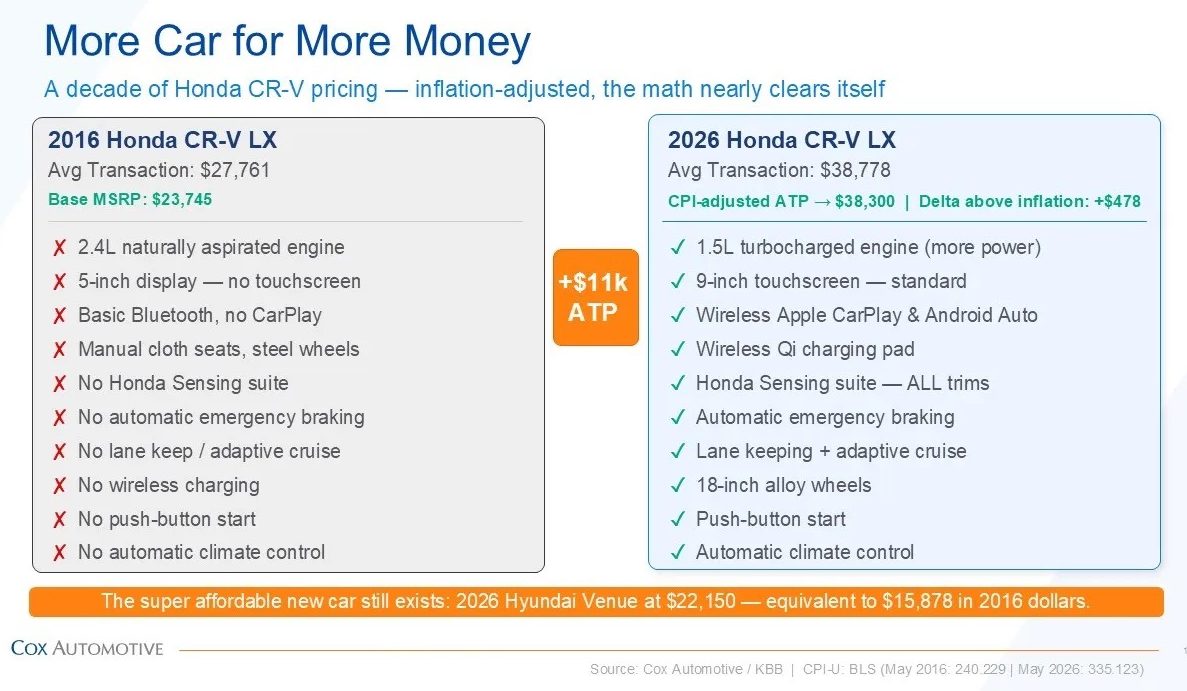

It’s the mix! This is definitely true, to some extent, although this chart from Cox is interesting:

A 2026 CR-V, when adjusted for inflation, is only about $500 more expensive, yet offers way way way more stuff, and more stuff that people want. Specifically, the report from Cox is called “The Car Is Not the Villain” because, even though ATP is up $11,000, it’s more complicated than people just buying good cars.

Today’s CR-V includes turbocharged performance, advanced infotainment, wireless smartphone integration, and driver-assistance technologies that were optional or unavailable a decade ago. It is a better, more capable vehicle by almost any measure. Once adjusted for inflation and income growth, the price has barely moved.

The increasing price of the car is real, but is that the manufacturer or the consumer driving this trend?

The Consumer Is To Blame

As the Edmunds report points out, consumers are hitting record lengths and amounts for loans, with potentially dangerous outcomes:

“Car shoppers are caught in a dangerous practice of focusing heavily on their monthly payment while ignoring the potential long-term damage to their wallets,” said Ivan Drury, Edmunds’ director of insights. “Pushing loan terms past six or seven years might make an average monthly payment more digestible today, but it’s a mathematical trap. When you pair a 7.0% APR with an 84-month loan and a smaller down payment, you’re signing up to hand over nearly $10,000 on average in interest alone. Unfortunately, stretching out the term to be able to swallow a higher-priced vehicle guarantees you’ll be building equity at a snail’s pace, leaving you highly vulnerable to falling underwater when it’s time to trade in.”

Are car shoppers being irrational here? Cox would argue that getting a slightly higher trim vehicle isn’t necessarily bad:

There is also a common-sense piece to this. When the price gap between a base vehicle and a better-equipped model is relatively small, many buyers choose the vehicle with more features, better fuel efficiency, or stronger long-term usability.

That behavior is rational. Consumers are thinking about total value, not just the lowest entry price. Over time, those choices shift the sales mix and lift the industry average. The headline number moves, but the underlying story is consumer choice.

It’s true that consumers are not as interested in cheaper vehicles. Given how long people keep cars these days, I do wonder how much of an impact option for the cold weather package or whatever matters 13 years down the road. If you sell your vehicles at a more normal rate, then the options you have can command a higher price.

Politics Are To Blame

Tariffs have added costs to new cars, as have safety regulations and environmental regulation. This is nowhere clearer than on the lower end of the market, as the United States has long relied on imports for many of its cheapest cars. Nissan, which often offers the most affordable cars on the market, does so by relying largely on Mexico for production.

With the USMCA under review, the prospect of bringing more cars from Mexico is a sketchy one, with Nissan’s CEO Ivan Espinosa pointing out to Bloomberg that the company is suddenly paying 25% more to import its cars:

The duties are “making part of the lineup that we are bringing in from Mexico difficult to sell,” Espinosa said Wednesday on Bloomberg Surveillance. “Looking at the pressure that the US market has today in terms of affordability, we see that potentially some of the buyers could be moving into this type of vehicle, so we are working very strongly on making them more competitive.”

[…]

While the company has shifted some vehicle production to reduce its tariff exposure, it’s kept entry-level models like the Nissan Sentra compact and Kicks crossover in Mexico to take advantage of lower labor costs. The manufacturer has said tariffs on the Kicks and Sentra cost around $2,500 to $3,000 per vehicle.

$3,000 on a Sentra is insane and, even if the goal is to bring more manufacturing to the United States, the medium-term impacts are extremely real. Nissan is trying to find ways to make the cars cheaper in Mexico as opposed to just bringing production here.

Politics is definitely playing a role, although it varies a lot by car, and politics aren’t making people buy $50,000+ three-row SUVs.

It’s The Economy

Consumer preference, regulation, politics, manufacturing choices, et cetera are all part of the picture. The sad reality is that many things are conspiring to impact the car market, and there’s very little consumers can do about it because of the underlying economy. This is something that all the analysts seem to agree on, and though it isn’t necessarily the main culprit, it’s the one factor that is insurmountable for a consumer and difficult for automakers to impact.

First, from Cox:

The bigger issue is the economic environment around the vehicle. Purchasing power has been stretched, household budgets are under pressure, and consumers are absorbing higher costs across nearly every part of daily life.

Vehicle insurance has risen sharply. Auto loan rates are higher, so borrowing costs more. Maintenance and repair costs are up. Gasoline is higher, too. So are housing, groceries, healthcare, and subscription services.

In that environment, it is no surprise that a new vehicle feels out of reach for many Americans. But the issue isn’t the car itself — it’s because life got more expensive.

And from Edmunds:

“The Q2 data perfectly illustrates the stark reality of today’s new-vehicle market: Affordability is such a massive hurdle that buyers are forced to stretch their budgets to the absolute limit just to get into a new vehicle,” said Jessica Caldwell, Edmunds’ head of insights. “When you see loan terms extending to record lengths, down payments shrinking, and monthly payments hitting all-time highs, you’re looking at a clear recipe for long-term financial strain.”

Some consumers are too stretched by all the various negative economic factors, whereas other consumers are driving the K-shaped market by shrugging off those concerns and demanding bigger, better, nicer. Automakers are also facing these concerns as money is more expensive to borrow and they, too, will reach a limit of what they can offer affordably to consumers.

In the end, the fingers are pointing in various directions because there are legit that many directions to point in these days.

What I’m Listening To While Writing TMD

It’s “Cats” by Mitski, because my cat was up this morning yelling at me to feed him even though I’m wiped after the track day.

The Big Question

What would you bring to an Autopian track day?

Top graphic images: stock.adobe.com; DepositPhotos.com

Bingo. According to CarGurus… there are 1,410,039 used cars for sale Nationwide right now…. 914,414 under $30,000…. 538,816 under $20,000…. 298,261 less than 10 years old. There is simply no reason to buy a new car on a 72 month loan other than “I want a car I cannot realistically afford”.

It’s a decision to rely on higher margin/lower volume that has accelerated because companies realized, during and after covid, there is much less price resistance than previously presumed. They’ll pay ADM! They’ll accept a blackjack that pays 6/5 instead of 3/2! They’ll pay $8 for a bag of chips! The benefit to companies is it combines lower expenses (material, labor, etc) because they’re making fewer items/serving fewer customers yet extracting more profit per item/customer. The downside for them is it gives rise to something called Client Concentration Risk, which is when their preferred group of customers shrinks and they’re left holding the bag because they’ve abandoned a larger, more stable base. Hello, Stellantis!

Agreeing with “all of the above” (and below in the comments). Think about how many individual decisions by how many individuals/groups/corporations go into design, manufacturing, marketing, regulation, pricing, financing, what to buy, when to buy, etc. etc. etc. And we would be remiss to ignore larger economic factors as well. Fundamentally, no one is going to agree on “the” right answer because every answer has some truth to it (short of the person saying it wearing a tinfoil hat, but maybe even then).