I had a bit of a whiplash moment this morning. Two well-respected analysts came out with reports about vehicle pricing and affordability, and neither report quite agreed with the other exactly as to the culprit. It’s a fun exercise to read both back-to-back as the problems are clearly identified and yet, while there’s some overlap, I don’t see fingers pointing quite in the same direction.

The Morning Dump will take a bit of a different approach this morning as I’m going to take the news of the day and analyze these two reports in the context of what they wrote, with the hope of coming to some sort of answer as to why no one has a clear answer. Obviously, I’ve written about this a lot this year, so I’ll try not to repeat myself too much.

This morning’s first analysis comes from Jessica Caldwell and her team at Edmunds. The other report is from Erin Keating at Cox Automotive. Edmunds, being B-to-C-focused, tends to have a consumer perspective, whereas Cox Automotive is a bit more B-to-B, but both are historically the best resources when it comes to tracking these issues.

The Manufacturer Is To Blame

This is the easy finger to point. Cars have gotten too fancy and too expensive and automakers have abandoned the lower-end of the market by getting rid of the sub-$25,000 car in almost every context. This is also the Trimflation argument, which is that automakers have prioritized higher margin vehicles and trim levels, meaning that even if a cheaper MSRP vehicle theoretically exists, few of them ever end up being built and sold.

This factor is called out by Edmunds, which reported today that a record number of people are taking out loans that are 84 months or longer.

“Unfortunately, this is the new normal for new-car buyers. Until we see a major shake-up in automaker incentives, a meaningful drop in interest rates, or a shift toward a more affordable mix of vehicles — none of which appear to be on the horizon — consumers will have to keep walking this financial tightrope.”

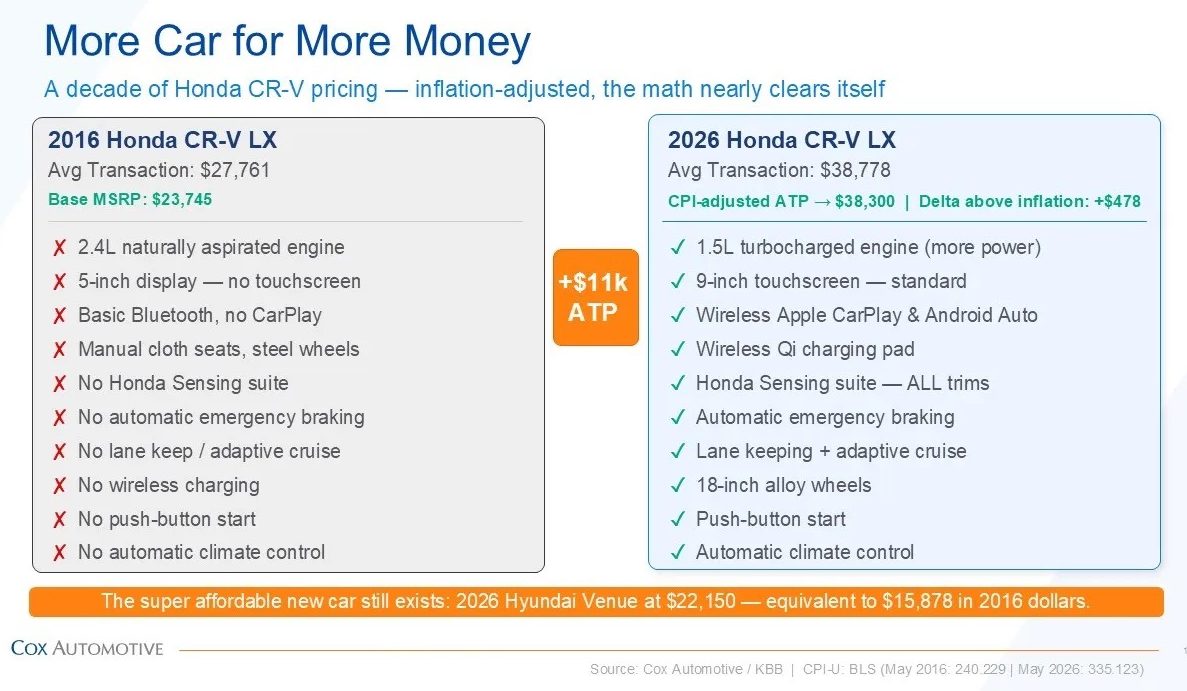

It’s the mix! This is definitely true, to some extent, although this chart from Cox is interesting:

A 2026 CR-V, when adjusted for inflation, is only about $500 more expensive, yet offers way way way more stuff, and more stuff that people want. Specifically, the report from Cox is called “The Car Is Not the Villain” because, even though ATP is up $11,000, it’s more complicated than people just buying good cars.

Today’s CR-V includes turbocharged performance, advanced infotainment, wireless smartphone integration, and driver-assistance technologies that were optional or unavailable a decade ago. It is a better, more capable vehicle by almost any measure. Once adjusted for inflation and income growth, the price has barely moved.

The increasing price of the car is real, but is that the manufacturer or the consumer driving this trend?

The Consumer Is To Blame

As the Edmunds report points out, consumers are hitting record lengths and amounts for loans, with potentially dangerous outcomes:

“Car shoppers are caught in a dangerous practice of focusing heavily on their monthly payment while ignoring the potential long-term damage to their wallets,” said Ivan Drury, Edmunds’ director of insights. “Pushing loan terms past six or seven years might make an average monthly payment more digestible today, but it’s a mathematical trap. When you pair a 7.0% APR with an 84-month loan and a smaller down payment, you’re signing up to hand over nearly $10,000 on average in interest alone. Unfortunately, stretching out the term to be able to swallow a higher-priced vehicle guarantees you’ll be building equity at a snail’s pace, leaving you highly vulnerable to falling underwater when it’s time to trade in.”

Are car shoppers being irrational here? Cox would argue that getting a slightly higher trim vehicle isn’t necessarily bad:

There is also a common-sense piece to this. When the price gap between a base vehicle and a better-equipped model is relatively small, many buyers choose the vehicle with more features, better fuel efficiency, or stronger long-term usability.

That behavior is rational. Consumers are thinking about total value, not just the lowest entry price. Over time, those choices shift the sales mix and lift the industry average. The headline number moves, but the underlying story is consumer choice.

It’s true that consumers are not as interested in cheaper vehicles. Given how long people keep cars these days, I do wonder how much of an impact option for the cold weather package or whatever matters 13 years down the road. If you sell your vehicles at a more normal rate, then the options you have can command a higher price.

Politics Are To Blame

Tariffs have added costs to new cars, as have safety regulations and environmental regulation. This is nowhere clearer than on the lower end of the market, as the United States has long relied on imports for many of its cheapest cars. Nissan, which often offers the most affordable cars on the market, does so by relying largely on Mexico for production.

With the USMCA under review, the prospect of bringing more cars from Mexico is a sketchy one, with Nissan’s CEO Ivan Espinosa pointing out to Bloomberg that the company is suddenly paying 25% more to import its cars:

The duties are “making part of the lineup that we are bringing in from Mexico difficult to sell,” Espinosa said Wednesday on Bloomberg Surveillance. “Looking at the pressure that the US market has today in terms of affordability, we see that potentially some of the buyers could be moving into this type of vehicle, so we are working very strongly on making them more competitive.”

[…]

While the company has shifted some vehicle production to reduce its tariff exposure, it’s kept entry-level models like the Nissan Sentra compact and Kicks crossover in Mexico to take advantage of lower labor costs. The manufacturer has said tariffs on the Kicks and Sentra cost around $2,500 to $3,000 per vehicle.

$3,000 on a Sentra is insane and, even if the goal is to bring more manufacturing to the United States, the medium-term impacts are extremely real. Nissan is trying to find ways to make the cars cheaper in Mexico as opposed to just bringing production here.

Politics is definitely playing a role, although it varies a lot by car, and politics aren’t making people buy $50,000+ three-row SUVs.

It’s The Economy

Consumer preference, regulation, politics, manufacturing choices, et cetera are all part of the picture. The sad reality is that many things are conspiring to impact the car market, and there’s very little consumers can do about it because of the underlying economy. This is something that all the analysts seem to agree on, and though it isn’t necessarily the main culprit, it’s the one factor that is insurmountable for a consumer and difficult for automakers to impact.

First, from Cox:

The bigger issue is the economic environment around the vehicle. Purchasing power has been stretched, household budgets are under pressure, and consumers are absorbing higher costs across nearly every part of daily life.

Vehicle insurance has risen sharply. Auto loan rates are higher, so borrowing costs more. Maintenance and repair costs are up. Gasoline is higher, too. So are housing, groceries, healthcare, and subscription services.

In that environment, it is no surprise that a new vehicle feels out of reach for many Americans. But the issue isn’t the car itself — it’s because life got more expensive.

And from Edmunds:

“The Q2 data perfectly illustrates the stark reality of today’s new-vehicle market: Affordability is such a massive hurdle that buyers are forced to stretch their budgets to the absolute limit just to get into a new vehicle,” said Jessica Caldwell, Edmunds’ head of insights. “When you see loan terms extending to record lengths, down payments shrinking, and monthly payments hitting all-time highs, you’re looking at a clear recipe for long-term financial strain.”

Some consumers are too stretched by all the various negative economic factors, whereas other consumers are driving the K-shaped market by shrugging off those concerns and demanding bigger, better, nicer. Automakers are also facing these concerns as money is more expensive to borrow and they, too, will reach a limit of what they can offer affordably to consumers.

In the end, the fingers are pointing in various directions because there are legit that many directions to point in these days.

What I’m Listening To While Writing TMD

It’s “Cats” by Mitski, because my cat was up this morning yelling at me to feed him even though I’m wiped after the track day.

The Big Question

What would you bring to an Autopian track day?

Top graphic images: stock.adobe.com; DepositPhotos.com

What would you bring to an Autopian track day?

In my circle of friends, acquaintances, and coworkers our incomes have NOT kept up with inflation. This drum beat of cars are cheaper now is fine for a lot of people but not all of us. It is wild to see people who could buy houses or new cars 10-20 years ago now driving cars they bought 10-20 years ago and not afford rent.

Cheap cars were a self fulfilling deal, like manual transmissions. The manufactures wanted higher profit, as did the dealers, neither stocked the cheap cars on the lot and then said the customers are not buying them. Even 25+ years ago I had to special order a cheap base model car with a manual.

“What would you bring to an Autopian track day?”

A lawn chair, an umbrella and a Yeti Cooler filled with cold drinks, cold fried chicken and fruit salad.

Don’t forget the sunscreen, mosquito repellent and Band-Aids.

Hero.

I can’t speak by any means to all new cars but in a specific instance of shopping for Mazda CX-5 for my wife a couple years ago it stood out that the base trim version which the dealer only had one of on the lot and Mazda was doing away with also felt dec-ontented and cheap even compared to going one trim level up. Whereas going from the mid tier trim to top of line just felt like we’d be getting a bunch of stupid gimmicks and gadgets (except adjustable lumbar-which as a tall guy I really want!).

Not sure about other car makers but I wonder if similar to Mazda in the time of top level interiors being dominated by screens when you get a basic car it feels aggressively cheap and crappy. Interior photos of the first year or two VB WRX seem to corroborate this (before they also axed the base model) in fact the base trim was even worse looking than the CX5, with two smaller screens surrounded by uhaul van matte gray trim instead of the mid and upper tier’s large screen with the admittedly still detestable piano black.

I wonder if anyone can guess what I would bring to an Autopian track day? It definitely doesn’t start with F and end with D and rhymes with tire turd.

You can’t mention your cats without sharing a picture of the beast.

If I could join a track day, and it ran, I’d bring the 6.9 and let people drive it.

TBQ . . . I’d bring something cold to drink and treats to share.

That’s awesome!

Another hero.

Very interesting discussion. A few specific comments:

Ah, but if it offers way, way more stuff, but people only want more stuff, I think you’ve found the disconnect. Honestly, a lot of what’s being sold as “features” on new cars is not something I want, and I will actively avoid it.

If you live somewhere it gets cold, it makes a big furry impact. This is something I learned when I was younger – sometimes waiting so you can afford the thing you want rather than settling for a cheaper thing that you only kinda want is the better financial decision. When I buy a car with the features I want, I’m far less likely to be shopping for a new one as soon as the loan term runs out, which is very good both from a quality of life perspective and a financial one.

Perhaps not, but politics are making expensive three-row SUVs look a lot better to manufacturers than they need to be, which encourages them to push more for consumers to buy them. Even when CAFE was a thing, the fact that many big crossovers qualified as “trucks” was a problem. With CAFE no longer a thing, they’re even more incentivized to push the big, heavy, inefficient vehicles with huge profit margins.

Agreed. I banged this drum back when Biden was in office too – no one person was responsible for inflation back then, and no one person is now either. There have been some epic own goals (fsck FIFA) on the inflation front, but it’s a complex economic thing and nobody can just arbitrarily reduce it (though it seems they can arbitrarily increase it).

TBQ: My 2001 Corvette. I originally had plans to track it at Road America, but I’m pretty sure I don’t fit in it well enough with a helmet on to pass safety inspection. The top of my helmet would be the crumple zone if I ever rolled it.

Something I’ve learned after moving out of the states is that the American market has generally become much less discerning than other global localities. It’s a broad stroke to paint, but we’ve been so conditioned to buy, buy, buy and the resulting endorphin rush, that firms don’t have to try as hard in a market with this level of purchasing power to make transactions more enticing.

We Americans cross-shop and compare prices, but very little attention is comparatively paid to overall value for the money. If everyone is selling an option for ventilated seats at $2000, many consider it a fair price without doing the introspection of if chilled butts are worth that cost, so even if the manufacturer could eventually bring the inflation-adjusted price down through better engineering or cost savings, there’s no need. It will sell fine.

Where I am now, the consumer has less of a problem walking away if an item doesn’t meet their needs or their budget. “Here today, gone tomorrow” marketing tactics also backfire as they’re insulted if a companies tries to rush their decision-making phase.

Is a 1.5L turbo likely to last as long as 2.4L NA?

Asking for a friend.

In a controlled environment I’d think the turbo would give out before the NA engine because of heat and more parts but who knows in the real world. And would that difference be significant over say, 8-10 years of ownership?

Depends on how you drive. Generally, the harder you run the engine, the faster it’d wear out

TBQ: Apparently a grandfather clock….

Will it do 150?

What’s hilarious is that my wife has a 2015 CR-V and even she’s perfectly happy w/ it because it has everything she needs/wants and not anything EXTRA. Both of our vehicles don’t have all of these extra fancy distracting/annoying features so we think they are better than new. I do understand about the concept of the new ones that if the car that’s loaded is only a little bit more, then it makes sense for that person. I’d probably still be one who would choose the not loaded car just to avoid the annoying fucking “features” and screens. I would never be buying a new car at a stealership anyway ha ha. “Ya but that TruCoat!!!” We are moving towards the minimalism lifestyle in general too, mostly as far as selling stuff around the house…but the concept is the same: if we don’t need it, we don’t want it and vice versa. We’d rather have experiences/vacations and time w/ family vs. stuff. There’s so much excessive consumerism.

“$10,000 on average in interest alone.”

That is what my current car cost and is my most expensive car! Plus it’s paid off

Yeah, I have a gas range that’s more than 20 years old that was manufactured by a brand that no longer exists but you’ll have to pry it from my cold, dead hands because it is dead simple, well built (before the cost-savings era) and just works. It doesn’t even have a freaking clock on it.

The short answer is costs are rising, much much faster than incomes

Read a depressing article about the middle-class dream of being able to buy a house is done. That’s not the most depressing part. The gut punch is the thesis of the article that the rise of the middle class from WWII through the 1980’s was a blip, an anomaly and that a world with Haves/Have Nots, Lords/Serfs etc. was the norm when you look at the whole timeline of civilization.

It’s true. The Baby Boomers enjoyed a life that no one before or after them has, but we weirdly set that as some sort of standard that we now can’t live up to.

I wouldn’t say weirdly . . . perhaps overly optimistic. What I do think is weird that a lot of Boomers/Gen X parents just casually acknowledge their kids have next to no chance to live the lives they had. i.e guy a nice house in a nice neighborhood.

TBQ: My lotus.

If I had decent tires. I need to call my tire guy tomorrow.

QOTD…. My slow-car-fast 91 Miata BRG5 speed .

TBQ: I’d bring my RC truck to track day. Tires are still affordable and its got great battery life and the batteries are swappable. No range anxiety over here, baby!

For TBQ, I wanted to bring my Bolt to Lime Rock on updated tires (though the Spark EV would have been more on theme!) but having just moved, there wasn’t time to do so.

TBQ: I only have my Clio Hybrid right now… so that?

I think it’s the consumers fault.

Cheap cars have been around for a long time, and consumers time and time again eschew them in favor of pricier options.

If no one bought 100k half ton pickups, they wouldn’t exist. Instead, they sell by the boatload.

If there were a lineup to buy Nissan Versas, or Mitsubishi Mirages, then other companies would take note and release offerings in that segment.

People are quick to blame car companies, or tariffs that have been around for a couple years, as the drivers behind cars getting more expensive. Meanwhile at work, the cleaning staff drive Explorers because God forbid they are seen in a small car!

You know why we have videocards that cost over 1000 usd? Because consumers pay for them.

Personal responsibility goes a long long way in life.

Fully agree. It is also the reason why crossovers are everywhere, manuals are dying, etc.

As a country in general, its citizens, government, and many corporations have been living beyond their / or means for decades. The good times must roll!

No, I’m going to disagree with you. I place the blame on dealers, not on consumers. Dealers are the ones who put cars on lots, dealers are ones who order them from the manufacturer. Dealers are the ones who upsell the customers.

tbq: Well, I do own a vehicle whose suspension was tuned by a guy who worked in Formula One and at Lotus. But perhaps I should bring the Miata instead.

If somebody could make money selling an easily affordable lineup, they would be doing so. Nissan was almost pulling it off, but the administration is busting their kneecaps with tariffs (and the wild swings make it impossible to plan investments).

If I don’t check all the options boxes, how will I be able to sell my Chevy Silverado as a 1 of 1 in 20 years?

Ha! Resale is the stupid reasoning to buy more expensive/optioned

1 of 1 built at that plant during that shift on that day!

Joke’s on you, I also checked all the option boxes so at best you’re 1 of 2! 😛

(I actually looked for one with fewer option boxes checked, but that doesn’t really work with the joke)

Bingo. According to CarGurus… there are 1,410,039 used cars for sale Nationwide right now…. 914,414 under $30,000…. 538,816 under $20,000…. 298,261 less than 10 years old. There is simply no reason to buy a new car on a 72 month loan other than “I want a car I cannot realistically afford”.

A lot of folks are (rightly or wrongly) afraid of used cars. My dad always buys new because he doesn’t want to “inherit someone else’s problem.” I can’t convince him that he just needs to do a little digging / research and he would be able to ferret out the problem cars. It probably doesn’t help that the last two used cars I bought gave me massive amounts of trouble (mainly because I got impatient and didn’t follow my own advice, resulting in buying a couple cars I should’ve walked away from)

I am like this. I also enjoy troublefreeness.

Not gonna lie, I’ve thoroughly enjoyed my current car, bought new and with a warranty, over those two used ones that taught me a lot about car repair (but out of necessity rather than desire lol)

I’ve thought about this a lot, as seemingly with many autopian commenters I have a higher tolerance for old/funky used cars than the average buyer. But even I sometimes get tired of the the weird little squeaks and groans of my old car, the little worn interior parts that cant easily be replaced. We got a lucky break and got a very low mileage grandma car from a family friend for my wife, and I have to admit it has been really nice having one basically new, everything works, no stress wondering if something is gonna poop out on a road trip, car.

I can see why for the average buyer it’s a total mystery box when/why their car breaks down and I think it makes the fear of something breaking often loom larger than it should…but also I don’t blame them, breaking down sucks, dealing with mechanics sucks, doubly so when you’re not knowledgeable. Which is a roundabout way of saying I can see why the average person is wary of buying-and ever since Covid lightly-used is no longer the deal it used to be. See recent article about used RAV-4s costing as much or more than new ones. I also wonder if some of this divide in opinion about this depends on where you live. I grew up in a small city in Montana if your car broke down you weren’t going to be risking your life waiting for a tow on the side of a busy 6 lane freeway, a friend or family member was probably at most a 20 minute drive away.

I’d rather have a nice used car than a stripped down new car. But I work on my own cars, so the lack of warranty isn’t as much as issue for me.

I call BS. As has been talked about here, it is very difficult to get a loan for a used car.

And since half of American households can’t even afford a $400 emergency, how the hell do you expect them to save up $10,000+ to buy a car outright?

Young coworker just replaced her failing PT Cruiser. She chose a used Mitsubishi Mirage for a reasonable price…and will be paying 19.99% interest due to lack of credit history. I could have purchased it for a lower rate on my credit card.

She needed a reliable vehicle and hasn’t been employed very long, so she did the best she could. It’s rough out there, especially for people just starting out or in precarious financial situations.

It’s a decision to rely on higher margin/lower volume that has accelerated because companies realized, during and after covid, there is much less price resistance than previously presumed. They’ll pay ADM! They’ll accept a blackjack that pays 6/5 instead of 3/2! They’ll pay $8 for a bag of chips! The benefit to companies is it combines lower expenses (material, labor, etc) because they’re making fewer items/serving fewer customers yet extracting more profit per item/customer. The downside for them is it gives rise to something called Client Concentration Risk, which is when their preferred group of customers shrinks and they’re left holding the bag because they’ve abandoned a larger, more stable base. Hello, Stellantis!

Agreeing with “all of the above” (and below in the comments). Think about how many individual decisions by how many individuals/groups/corporations go into design, manufacturing, marketing, regulation, pricing, financing, what to buy, when to buy, etc. etc. etc. And we would be remiss to ignore larger economic factors as well. Fundamentally, no one is going to agree on “the” right answer because every answer has some truth to it (short of the person saying it wearing a tinfoil hat, but maybe even then).